sapling

Personal Finance

Student Loans

Credit Cards

Debt

Taxes

Budgeting

Investing

Home Finance

Car

Personal Finance

Career Growth

Freelance

Small Business

Resume Tips

First Jobs

Switching Careers

Career Advancement

All Career Growth

The Juggle

Balancing Life + Work

Travel

Shopping + Entertainment

Home Ownership

Insurance

Retirement

All The Juggle

JOIN OUR NEWSLETTER

JOIN OUR NEWSLETTER

Grant a Wish!

By: Beverly Bird

Read

Advertisement

By

Ashley Donohoe

These Tips Can Help Save You the Big Bucks on Holiday Flights

The Juggle

By

Melissa Fanella

Can a Married Couple Get First-Time Homeowner Benefits Twice?

The Juggle

By

Beverly Bird

Options If You Can't Pay the IRS

Personal Finance

By

Ashley Donohoe

Hacks to Help You Get Out of the Debt Trap

Personal Finance

By

Stephanie Faris

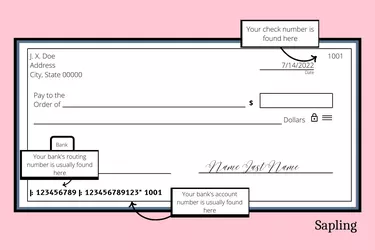

What Information Is Required on a Check?

Personal Finance

By

Melissa Fanella

Recession-Proof Side Gigs

Career Growth

By

Ashley Donohoe

Is It Time for a College Bank Account?

Personal Finance

By

Anne Johnson

Do You Pay Taxes on Personal Payment Apps?

Personal Finance

By

Stephanie Faris

Is It Time for a Second Job?

The Juggle

By

Ashley Donohoe

Your Taxes & Student Loan Forgiveness

Personal Finance

By

Anne Johnson

Are 401(k) Loans Really Worth the Risk?

Personal Finance

By

Ashley Donohoe

College for Working Adults: Full Time vs. Part Time

Personal Finance

Follow Us on Social Media

By

Melissa Fanella

Workday Wellness Hacks

The Juggle

By

Melissa Fanella

Is Now the Time to Switch Jobs?

Career Growth

By

Ashley Donohoe

Using Your Federal Work Study for Job Experience

Career Growth

By

Anne Johnson

How Do I Search for Forgotten Assets?

Personal Finance

By

Jim Woodruff

What Is Dow Jones & the DJIA?

Personal Finance

By

Beverly Bird

The Inflation Reduction Act & Going Green

The Juggle

By

Ashley Donohoe

Are Credit Card Deals for College Students a Good Deal?

Personal Finance

By

Melissa Fanella

Mutual Funds vs. Index Funds: Pros & Cons

Personal Finance

By

Ashley Donohoe

Reduce Your Cost of College With Alternate Credits

Personal Finance

By

Jim Woodruff

ETFs vs. Mutual Funds: Pros & Cons

Personal Finance

By

Ashley Donohoe

Create a Budget With Your College Student

Personal Finance

By

Beverly Bird

How Is Long COVID Affecting the US Economy?

The Juggle

Report an Issue

Contact*:

Severity*:

High

Normal

Low

Description*:

Screenshot loading...

Cancel

Submit