AI personal finance advice study: how “personal” it is

More than half of adults in the U.S. and U.K. have asked an AI tool for financial guidance, according to MIT Sloan research published in May. That is now close to the share who consult a human adviser. The problem, as a new AI personal finance advice study suggests, is that the answer depends heavily on who is asking and how they ask.

The MIT Sloan and CEPR working paper is the most detailed life-cycle look at AI financial advice so far. It finds that leading models give broadly sensible guidance on basics like saving and investing, but they also lean on a few blunt rules of thumb, and they respond differently to prompts written by different kinds of users. The advice can look tailored. Often, it is only loosely so.

That distinction matters because the projected gaps are not small. Advice generated from prompts written by women led to nearly $60,000 less wealth by age 60 than advice generated from prompts written by men, while prompts from people with low financial literacy produced nearly $50,000 less wealth. For people with no prior experience seeking financial guidance from AI, the gap was nearly $100,000 (MIT Sloan, May 2026).

What this AI personal finance advice study found

The good news is real. The MIT/CEPR research simulated financial lives from age 22 to 90 using prompts from a nationally representative sample of around 1,000 U.S. adults, then fed those prompts into ChatGPT 5.2 and Gemini 3 Flash (MIT Sloan, May 2026). On the decisions that matter most, the models mostly tracked what economists would prescribe.

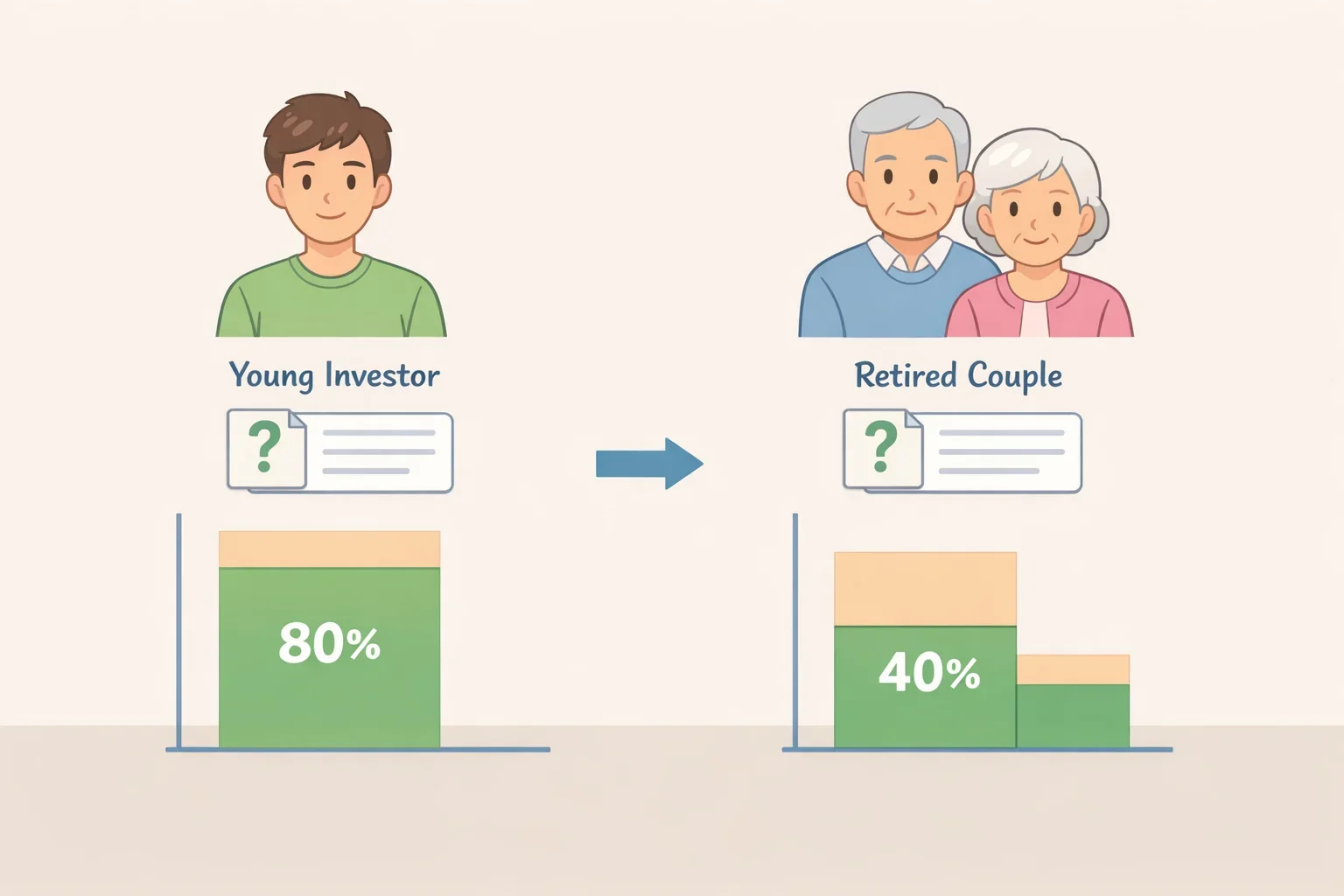

Following the models’ advice pushed more than 99% of simulated people into the stock market, raised equity allocations by as much as 40 percentage points, and built savings buffers above $10,000 for almost everyone by age 30 (CEPR, June 2026). In many cases, the simulations ended with wealth above $1 million by retirement, at least on paper.

The models also did something useful that many users probably would not have thought to ask for. Liquidity appeared in 83% of AI responses even though only 6% of people mentioned it, and saving showed up in 76% of answers even though only 20% of prompts raised it (MIT Sloan, May 2026). On the basics, the machine often nudged people toward better habits than the ones they described.

It even handled some context well. When prompts mentioned macroeconomic uncertainty, the AI recommended more saving and less risk-taking. Portfolio allocations also declined after midlife, which fits standard life-cycle theory. As MIT’s Taha Choukhmane put it, it was “actually surprising the advice aligns with life-cycle theory, since these systems aren’t designed to optimize financial decisions” (MIT Sloan, May 2026).

Where the heuristics take over

The trouble starts when the advice needs to get specific. The MIT/CEPR paper found that about a third of saving-rate recommendations were round multiples of 10%, and more than 98% of retirement withdrawal recommendations followed the 4% rule, regardless of the details in the prompt (CEPR, June 2026). That is not personalization. That is a calculator with a favorite number.

A job-loss scenario made the limitation plain. When a simulated worker lost their job and income fell by half, the model told them to cut spending, even when they had savings sitting there ready to be used (CEPR, June 2026). The buffer, which is the point of having one, went unmentioned.

A separate arXiv preprint from April found a similar pattern across frontier models. Using 1,000 synthetic client profiles, the authors reported “systematic heuristic collapse,” meaning investment allocations were driven mainly by self-reported risk tolerance, while age, income, investment horizon, and liquidity needs mattered much less than they should have (arXiv, April 2026). The failure is easy to miss in a single exchange because the output still sounds reasonable. The pattern only shows up when you look at enough cases to see how little the model changes.

Better prompts help, which is both encouraging and a little depressing. The MIT/CEPR study found that richer instructions, with life-cycle framing, portfolio theory, and fuller financial context, improved spending and saving guidance and reduced reliance on round-number shortcuts (MIT Sloan, May 2026). In plain English: users who know more get better answers because they ask better questions.

Who gets worse advice

The unevenness shows up most clearly by demographic group. The MIT study found that advice generated from prompts written by women led to nearly $60,000 less wealth at age 60 than advice generated from prompts written by men, a difference of 4.10%, largely because the model recommended less equity exposure and less active rebalancing (MIT Sloan, May 2026).

The low-literacy gap was nearly $50,000, or 4.11%, and the no-prior-AI-experience gap was nearly $100,000, or 5.71% (MIT Sloan, May 2026). Those numbers are not interchangeable. They point to different weak spots: lower equity exposure for women and low-literacy users, lower savings for people new to AI advice.

Part of the gender gap came from the prompts themselves. Women tended to use words like “family,” “grocery,” and “pay,” while men leaned toward “strategy,” “crypto,” and “growth” (CEPR, June 2026). The rest came from the model. When researchers labeled an otherwise identical prompt as coming from a man, the AI recommended more equity exposure; when it was labeled as coming from a woman, it recommended less (MIT Sloan, May 2026).

That default setting is not flattering. UC Berkeley Haas research from January found that without explicit demographic prompting, 55% of AI responses resembled those of young, high-income men, even though that group makes up less than 15% of the population. All unprompted responses assumed incomes above $54,000, and only 6% identified the user as 39 or older (UC Berkeley Haas, January 2026).

A Financial Planning Association study from June added another wrinkle: seven GenAI tools gave materially different emergency-savings and portfolio recommendations, and some returned stale tax data such as outdated 401(k) contribution limits. A tool can sound current and still be behind the curve.

How to use AI without overtrusting it

The cleanest takeaway is not to avoid AI for personal finance. It is to stop treating it like a substitute for judgment. The MIT study suggests AI can be useful for building financial understanding and sharpening your questions before you ask for recommendations, rather than accepting the first answer that lands in the chat window (MIT Sloan, May 2026).

The FPA study says GenAI may serve as a helpful starting point, but should complement, not replace, professional advice. The arXiv paper gives a practical test: if a recommendation barely changes when you alter your income, age, or time horizon, the model is not really using those inputs (arXiv, April 2026).

A few warning signs are worth remembering. Round-number savings rates and rigid 4% withdrawal advice are one. Another is guidance that ignores taxes, liquidity, or time horizon when those things clearly matter. A third is advice that looks almost identical across very different scenarios. Those patterns show up repeatedly as signs of heuristic thinking rather than genuine personalization (CEPR, June 2026; FPA, June 2026).

The bigger picture is moving faster than the guardrails. Consumer Reports reported last week that AI is already influencing loan approvals, pricing, and account coaching at scale, largely out of sight, while no clear framework defines what consumers should expect from an AI-powered financial product. The advice problem and the accountability problem are arriving together.

MIT’s Choukhmane summed up the state of play neatly: “Access to good financial outcomes may depend not just on better models, but on better questions, and who is asking them” (MIT Sloan, May 2026). That is a useful standard for now. Treat AI as a starting point, not a fiduciary. A smart one, maybe. Still not the adult in the room.