Chase 5/24 rule explained: how it works and counts

If Chase tells you you’re over 5/24, the reason is usually plain enough: you’ve opened too many personal credit cards in the last 24 months. The frustrating part is that the count reaches across issuers, not just Chase, so an Amex or Citi card can push you over the line just as easily as one from Chase itself (NerdWallet, June 2026; The Points Guy, May 2026).

That matters because Chase still holds some of the best rewards cards in the game, and most of them are subject to the Chase 5/24 rule. A strong credit score, decent income, or a long relationship with the bank does not reliably change the outcome (The Points Analyst, July 2025).

How the Chase 5/24 rule works

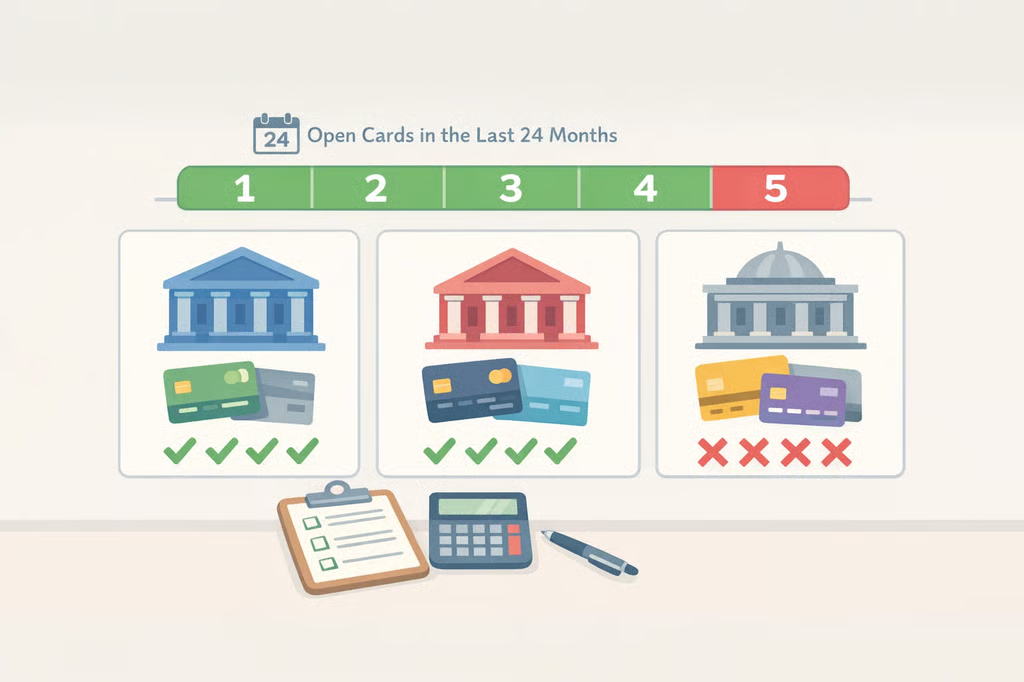

The Chase 5/24 rule is not an officially published policy, but it is well established through years of application data and customer experience (The Points Analyst, July 2025). Chase will likely deny most card applications if you have opened five or more personal credit cards with any bank in the past 24 months (The Points Guy, May 2026).

That count is broader than many applicants expect. It applies to all personal credit cards across banks, and most Chase-issued rewards cards are covered too, including co-branded cards (The Points Guy, May 2026; The Points Analyst, July 2025). In practice, that means the rule can shape an entire rewards strategy before the first application is even filed.

What counts toward Chase 5/24 status

This is where people most often miscount. Chase looks at whether an account was opened, not whether it is still open, so a card opened 18 months ago and closed last month still counts (The Points Guy, May 2026; CreditCards.com, February 2022).

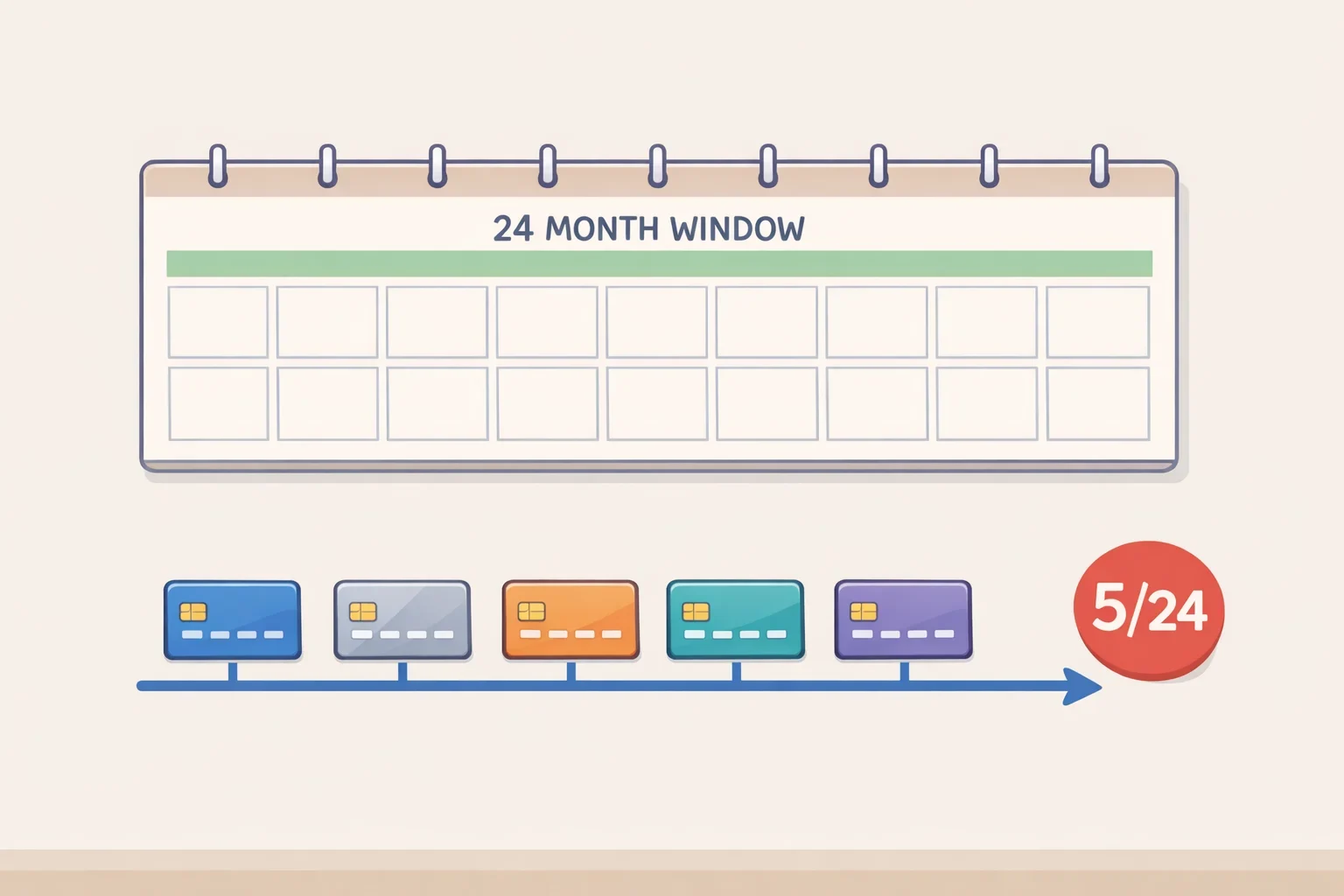

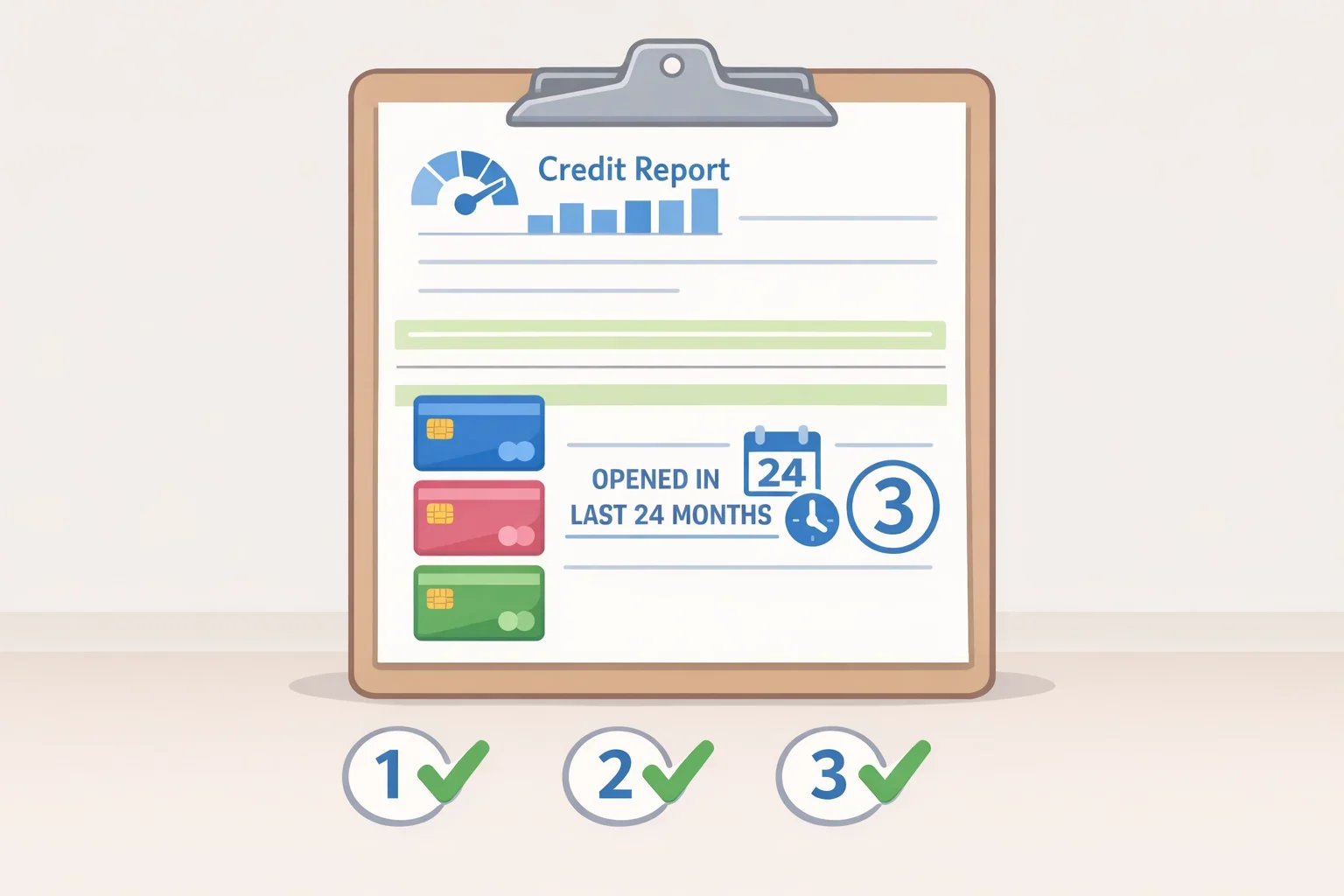

The easiest way to check your status is to pull a free credit report from Experian, Equifax, or TransUnion at AnnualCreditReport.com and count personal cards opened in the last 24 months (The Points Analyst, July 2025; CreditCards.com, February 2022).

A few cases trip people up:

- Authorized user accounts usually count if the account was opened within the last 24 months and shows up on your credit report (NerdWallet, June 2026; The Points Guy, May 2026).

- Business cards from most issuers do not count, but Chase’s guidance is not blanket-simple. Business cards opened with Discover and TD Bank count, as do most Capital One small-business cards, except the Capital One Venture X Business and Capital One Spark Cash Plus (The Points Guy, May 2026).

- Store cards can count if they appear on your credit report. Some reports suggest even single-store cards may now count, so the safest assumption is that if it is a credit card and it reports to your file, Chase may count it (The Points Guy, May 2026).

- Denied applications do not count, because inquiries are not the same thing as opened accounts (The Points Guy, May 2026).

There is also a timing wrinkle. You are not technically below 5/24 the moment 24 months pass on the fifth account. According to the most recent data points, you need to wait until the first day of the 25th month after that fifth card was opened (The Points Guy, May 2026). If your fifth most recent account opened in October 2024, do not apply before Nov. 1, 2026 at the earliest (The Points Guy, May 2026).

How to get around the Chase 5/24 rule

There is no magic switch here. If you are over 5/24, the most dependable move is to wait it out. Chase is unlikely to approve you for many of its cards until your count falls back under the limit (CreditCards.com, February 2022; The Points Guy, May 2026).

That said, a few paths are worth checking.

First, apply for a Chase business card while you are still under 5/24. Chase business cards generally require you to be below the threshold when you apply, but if you are approved, the account should not add to your 5/24 standing (The Points Guy, May 2026; CreditCards.com, February 2022). That is the cleanest workaround available, at least for readers who still have room.

Second, check Chase’s targeted offers. Some cardholders have reported getting approved through “Just for you” offers inside their Chase account even while over 5/24 (The Points Guy, May 2026; CreditCards.com, February 2022). To look, log in and check “Just for you” under “Explore products” in the left-hand menu. It is worth a glance, not a strategy you can bank on.

Third, use a product change instead of a new application. If you already have a Chase card, you may be able to convert it to another product within the same family without opening a new account (The Points Analyst, July 2025). That matters because product changes typically do not add to your 5/24 count, unless the change involves a hard inquiry or a new account number (The Points Guy, May 2026; The Points Analyst, July 2025). Ask Chase before you switch. Card issuers have a charming habit of making “simple” things not simple.

A few rumored shortcuts are less solid. In-branch applications and Chase Private Client status are sometimes mentioned as ways around 5/24, but the evidence for both is anecdotal and unreliable (The Points Analyst, July 2025). Fine to hear about. Not fine to plan around.

Chase 5/24 strategy: sequence your applications carefully

If you are new to rewards cards and nowhere near the limit yet, Chase cards deserve priority. Cards from other issuers can be picked up later without affecting your Chase approval odds, since 5/24 is a Chase-specific screen (The Points Guy, May 2026).

That said, speed is the enemy. Reader reports suggest Chase may scrutinize applicants who open too many cards too quickly, and some online reports indicate the bank will not approve more than two new accounts within 30 days (The Points Guy, May 2026). Many experts recommend spacing applications three to four months apart (The Points Guy, May 2026).

The Freedom family is the neatest example of why timing matters. Chase does not restrict how many types of Freedom cards you can have, and if you stay under 5/24, you can conceivably open all three currently available Freedom cards and earn a sign-up bonus on each one (NerdWallet, June 2026). That is a generous setup, but only for applicants who leave room in the calendar.

The small print worth remembering

Chase’s 5/24 rule is still one of the stricter gates in the points world, and it does not appear to be going anywhere soon (The Points Guy, May 2026). That makes the count itself the thing to watch. Not your approval odds after the fact.

So the practical move is simple: pull your report, count every personal card opened in the last 24 months, include authorized user accounts unless Chase excludes them, and treat business cards carefully because a few do count (The Points Guy, May 2026; CreditCards.com, February 2022). If you are under the line, apply deliberately. If you are over it, wait, or look for a targeted offer instead of forcing the issue.