- Debt avalanche method explained: setup, worksheet, steps

- When the debt avalanche method makes sense

- Build a debt avalanche worksheet first

- How to use the debt avalanche method

- How avalanche compares with snowball

- A quick example of the math

- When to switch away from avalanche

- The bottom line for setup

Debt avalanche method explained: setup, worksheet, steps

The debt avalanche method is the cleanest way to pay off multiple debts if the goal is to cut interest costs. The rule is simple: pay minimums on every account, then put every extra dollar toward the highest APR first. When that balance is gone, roll the same payment to the next-highest rate.

That part is easy enough. The harder question is whether avalanche is the right fit for a pile of debt, especially if the highest-rate account is not the smallest one. This guide walks through the decision, the setup, a practical debt avalanche worksheet, and the point where snowball may be the better play.

When the debt avalanche method makes sense

The case for avalanche rests on two things, how wide your APR spread is, and whether you can stay with the plan long enough to see it work. According to Unburden, modeled profiles with a 20-point spread between highest and lowest APR saved a median of $881 with avalanche, while profiles under 5 points saw roughly no difference. When rates sit close together, the savings can be small enough to shrug at.

That is the part people miss. Avalanche is mathematically neat, but it can be behaviorally dull. Unburden says research from Northwestern University’s Kellogg School of Management found completion rates predicted realized savings more than strategy choice did, and a 2016 Journal of Consumer Research paper by Kettle, Trudel, Blanchard, and Häubl points to why: motivation tracks the share of a balance eliminated, not just the dollars paid.

A rough rule of thumb follows from that. If your rates are far apart and you are the kind of person who will keep sending money at the same plan month after month, avalanche is probably the right tool. If your rates are clustered and you need early wins to stay engaged, the snowball method can be easier to live with.

Build a debt avalanche worksheet first

Before you move money around, make the list. A debt avalanche worksheet does not need to be fancy. It just needs to force the right order.

Use five columns, which match the planning structure SenseCentral recommends for money worksheets: goal, numbers, timeline, status, and action step. That format keeps the page useful instead of decorative, which is about as much praise as a worksheet deserves.

Set up your rows like this:

- Account name

- Balance

- APR

- Minimum payment

- Order in the payoff queue

- Current status

- Next action

Then sort the rows by APR from highest to lowest. That is the whole trick. Highest interest debt first, no drama, no sentimentality.

Example:

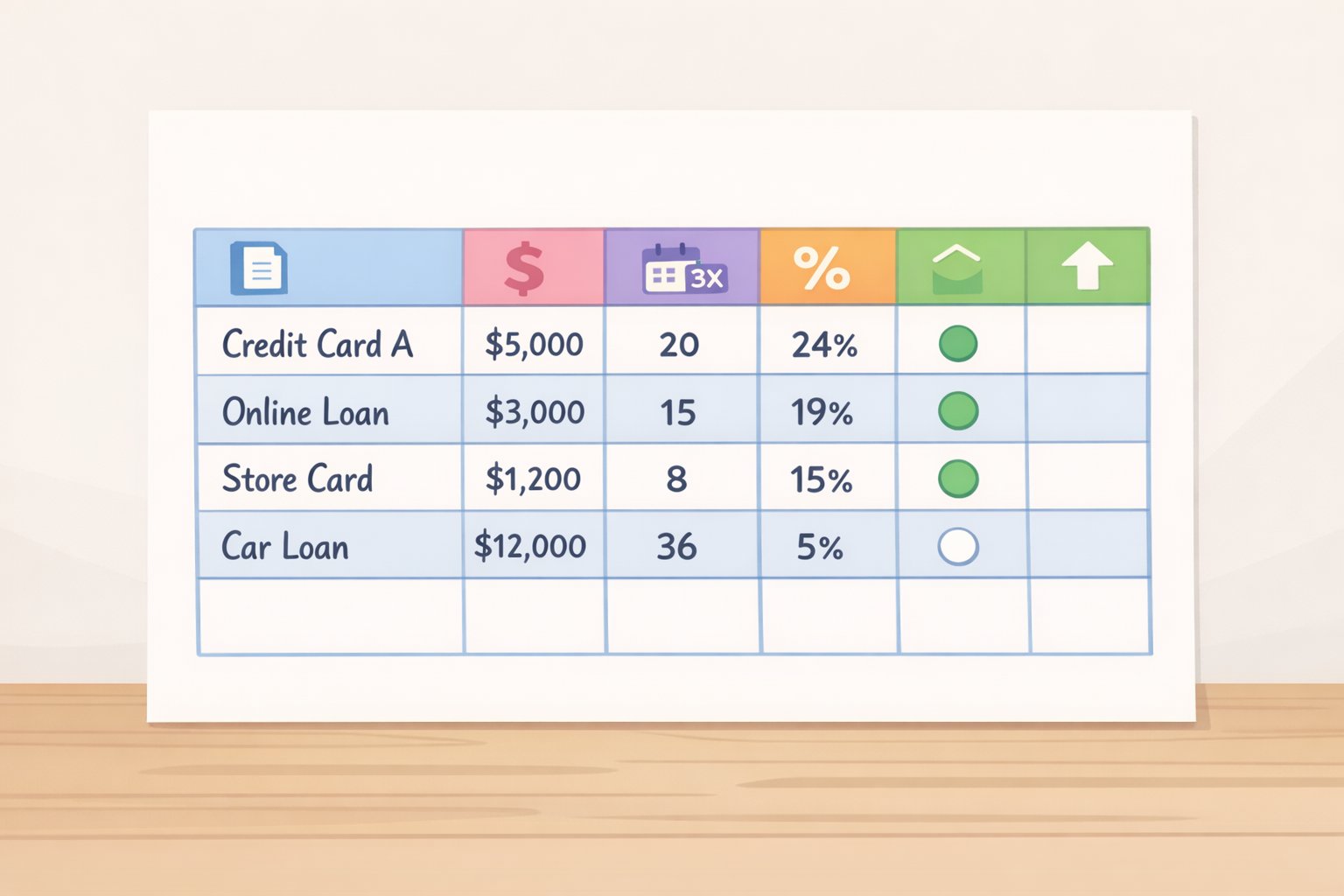

- Store card, $1,800 balance, 27.99% APR, $40 minimum

- Visa, $9,500 balance, 24.99% APR, $200 minimum

- Auto loan, $14,000 balance, 7.49% APR, $310 minimum

- Federal student loan, $6,700 balance, 5.50% APR, $90 minimum

In that setup, the store card goes first even though it is not the largest balance. That is the point. Balance size does not decide the order, rate does.

How to use the debt avalanche method

The setup itself is mechanical. Bring current statements for every account, then work through these steps. If your monthly minimums already exceed your take-home pay, stop here and talk to a nonprofit credit counselor. The NFCC says the first consultation is typically free.

Step 1: List every debt and sort by APR

Write down the current balance, APR, minimum payment, and account type for each debt. Then rank the accounts from highest APR to lowest. Unburden says that four-number checklist, balance, APR, minimum, account type, is enough to build the payoff order.

Do not let account age, balance size, or due date distract you. If one card charges 26.99% and another loan charges 6.5%, the card goes ahead of the loan even if the loan balance is ten times larger. That is the math talking.

Step 2: Set the monthly amount you can really sustain

Add up every minimum payment first. Whatever remains is your avalanche extra. The important part is not squeezing out the biggest possible number on a good month, but choosing an amount that still works on a bad one.

This is where people get clever and then regret it. Set the extra too high, miss it once, and the whole plan gets sloppy. Unburden says a single 30-day late report can cost 60 to 110 credit score points and may trigger a penalty APR on the late account. That is a very expensive way to save yourself from rounding up aggressively.

Step 3: Automate the minimums

Turn on automatic minimum payments for every account. Then set a separate automatic transfer for the avalanche extra to the highest-rate debt. Unburden says Equifax Canada and TransUnion Canada guidance points to this as the safest way to protect payment history while you direct extra money at the top of the queue.

This part matters more than it sounds like it should. If the minimums are automated, the plan keeps moving even when life is busy, which is most of the time. If they are not, the method is only as good as your memory, and memory is not a payment system.

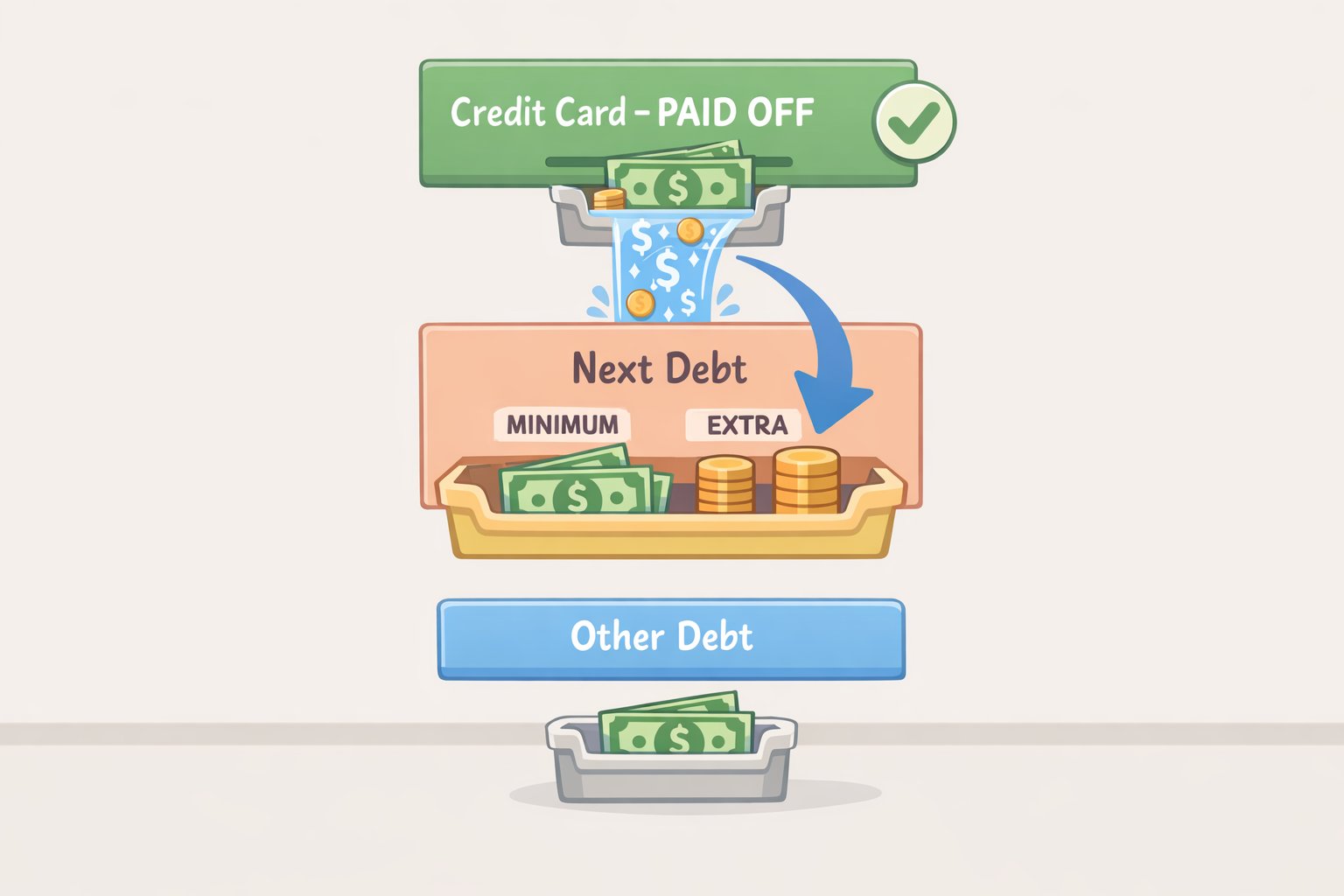

Step 4: Roll the payment forward when one account closes

When the top account hits zero, take the full payment that was going to it, minimum plus extra, and move it to the next account in line. Do not let that freed-up money drift back into spending. It has a job.

This is where avalanche starts to look less like a slog and more like a staircase. Every closed account makes the next one fall faster.

Step 5: Re-sort whenever a rate changes

A balance transfer promo ending, a variable APR reset, or a changed minimum can all alter the order. Unburden notes that 0% balance transfer offers usually revert after 12 to 21 months, and variable-rate accounts can reprice within one to two billing cycles after a Federal Reserve move.

That means the worksheet is not a one-and-done document. Re-run it whenever a balance, rate, or minimum changes. A neat list is only useful if it is still true.

How avalanche compares with snowball

Avalanche and snowball are really different answers to the same problem. Avalanche minimizes total interest paid. Snowball minimizes time to the first closed account.

The trade-off shows up fast in modeled examples. On a four-account stack with $32,000 in total debt and $1,100 a month to work with, Unburden says avalanche closes the store card in month four, the Visa around month 30, the auto loan around month 57, and the student loan around month 60. Total interest lands near $9,400. The same balances under snowball come in near $12,800.

That is a real gap. It is also not the whole story. Unburden says research from Northwestern University’s Kellogg School of Management on roughly 6,000 debt management clients found that snowball users were more likely to fully eliminate their debt, even when paying slightly more in interest. Early closed-account momentum explained most of the difference.

So the decision is not moral. It is practical. If you need the cheapest total path and can stick with it, avalanche wins. If you need the psychological jolt of crossing something off quickly, snowball may keep you in the game longer. The right method is the one you will still be using next year.

A quick example of the math

Take the simple comparison Unburden uses: $5,000 on a credit card at 24.99% and $5,000 on a personal loan at 8%. The card accrues roughly $104 in interest this month, the loan accrues roughly $33. Put an extra $300 toward the card and you prevent about $6 of next month’s interest. Put it toward the loan and you prevent about $2.

Same $300. Different result.

That is why avalanche puts the extra payment where the rate is highest. It is not about being tidy. It is about stopping the most expensive balance from growing first.

When to switch away from avalanche

There are a few cases where avalanche is not the smartest default.

- Your APRs are all within about 5 points of each other

- Your highest-rate debt is also your largest balance, and the first closure feels miles away

- You need visible wins to stay disciplined

- You have a small debt under $500, where a hybrid approach can give you momentum without giving up much interest savings

Unburden says that on profiles with under a 5-point spread, the savings from avalanche versus snowball fall to roughly zero. In that territory, the argument for avalanche gets thin fast. There is no prize for being mathematically pure if the plan falls apart by month eight.

The bottom line for setup

If you have multiple debts with different APRs, avalanche is straightforward: list the balances, sort by rate, pay the minimum on everything, and send the rest to the highest-interest debt. If you want a worksheet, build one with the five zones SenseCentral recommends, then keep it updated as rates change.

And if you are still unsure whether avalanche or snowball fits better, run both on your numbers. Unburden says its debt payoff calculator does exactly that, which is usually better than arguing with yourself in the dark.