- Social Security retiree tax deduction: who qualifies

- Who qualifies for the social security retiree tax deduction

- Step 1: Check your age first

- Step 2: Confirm the SSN requirement

- Step 3: File jointly if married

- Step 4: Stay under the income limits, or know how the phaseout works

- Step 5: Make sure Schedule 1-A is on the return

- How the $6,000 tax deduction for seniors stacks with other breaks

- Why some retirees may not benefit much

- Conclusion

Social Security retiree tax deduction: who qualifies

The social security retiree tax deduction is a new $6,000 break for people 65 and older, or $12,000 for a married couple if both spouses qualify. The IRS said on Feb. 27, 2026 that the deduction runs from tax years 2025 through 2028. It sounds like a neat little fix for Social Security taxes. It is not that.

The deduction does not change how Social Security benefits are taxed. The old formula still controls that part of the return, based on combined income, which means adjusted gross income, tax-exempt interest, and half of Social Security benefits. Up to 85% of benefits can still be taxable under existing rules, CRS noted in August 2025.

What follows is the practical version, stripped of the usual tax-season fog.

Who qualifies for the social security retiree tax deduction

To claim the deduction, four things have to line up. Miss one, and the tax break starts shrinking or disappears.

- Be age 65 or older by the end of the tax year. For a 2025 return, the IRS says that means born before Jan. 2, 1961. IRS says age 65 counts at the end of the year if the birthday falls on or before Jan. 1 of the following year.

- Have a valid Social Security number. For married couples filing jointly, the spouse claiming the deduction must have a valid SSN issued by the SSA before the due date of the return, including extensions. An ITIN does not qualify. IRS says the SSN must be valid for employment.

- File jointly if married. IRS says married taxpayers must file a joint return to claim it.

- Stay under the income limits, or accept a smaller deduction. The deduction starts phasing out above $75,000 of modified adjusted gross income for single filers and $150,000 for joint filers. IRS confirmed those thresholds on Feb. 27, 2026.

That is the whole test. Age, SSN, filing status, income. Tax law rarely gets cleaner than that, which is saying something.

Step 1: Check your age first

The age rule is blunt. If you are not 65 by year-end, the deduction is off the table for that tax year.

That applies even if you are already retired and collecting Social Security. The deduction is age-based, not benefit-based. The CRS said in August 2025 that a taxpayer does not need to receive Social Security benefits to qualify for the deduction at all.

Step 2: Confirm the SSN requirement

The IRS is equally blunt here. A valid SSN is required, and for a married couple filing jointly, the spouse claiming the deduction must have one too. The agency defines a valid SSN as one that is valid for employment and issued before the filing deadline.

That matters more than it sounds. Plenty of tax breaks are generous on paper and fussy in practice. This one is fussy in practice.

Step 3: File jointly if married

If married taxpayers want the deduction, they need one return, not two. Married filing separately shuts the door on the deduction entirely.

Single filers, heads of household, and qualifying widows or widowers do not face that filing-status hurdle if they meet the other rules.

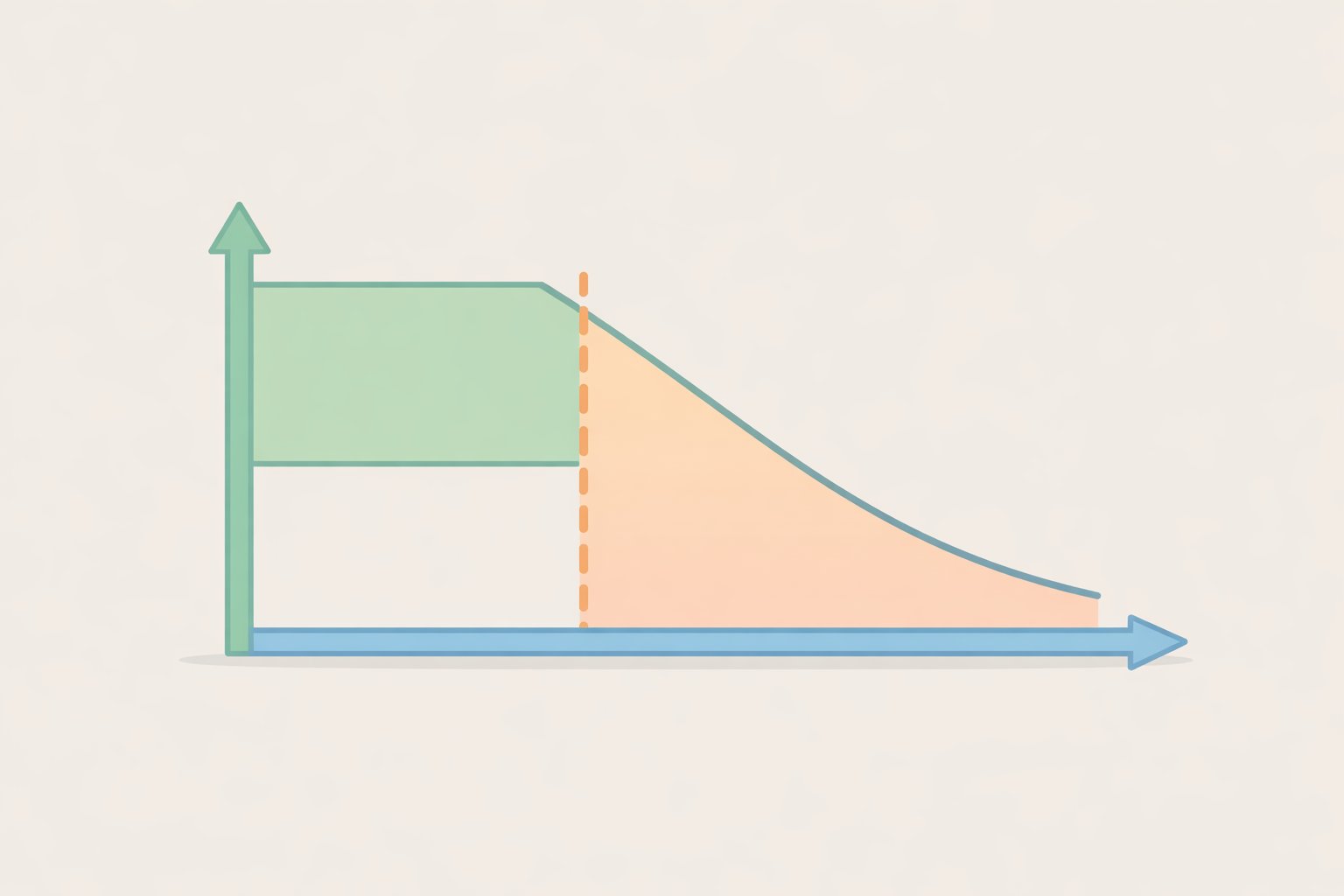

Step 4: Stay under the income limits, or know how the phaseout works

The deduction begins phasing out once modified adjusted gross income goes over $75,000 for single filers and $150,000 for joint filers, according to the IRS. The phaseout rate is 6%, or $60 for every $1,000 above the threshold.

That means a single filer at $85,000 MAGI loses $600 of the deduction and keeps $5,400. The deduction is fully phased out at $175,000 for single filers and $250,000 for joint filers. IRS and CRS both put the same limits in writing.

One thing worth watching: MAGI here includes adjusted gross income plus tax-exempt interest. It does not include Roth distributions, because those are already tax-free. That is one reason retirees with mostly Roth money may get little out of the new deduction.

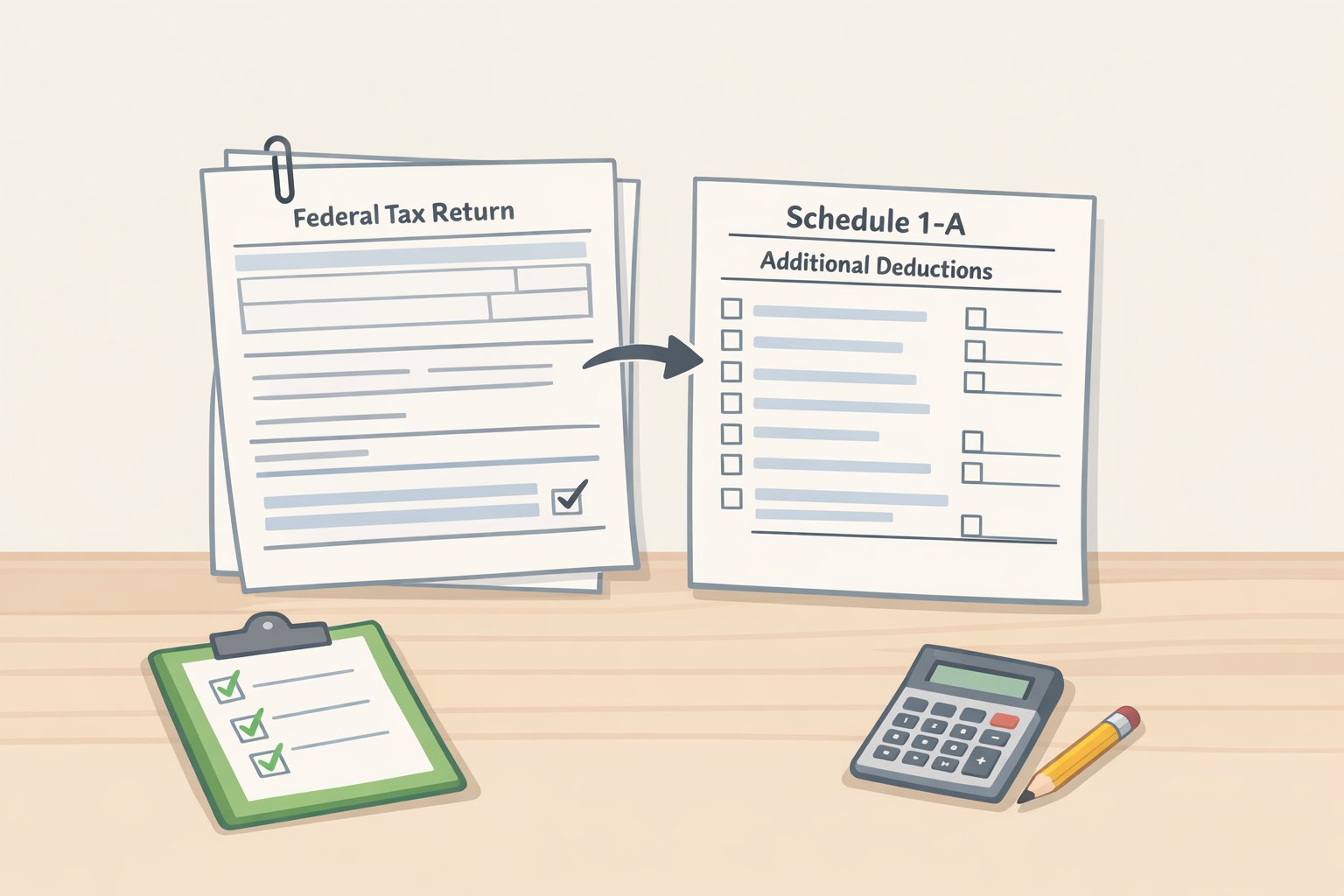

Step 5: Make sure Schedule 1-A is on the return

The deduction is claimed on new Schedule 1-A under Additional Deductions. USA Today reported in January that if the form is left off, the deduction is lost.

The deduction is available whether a taxpayer itemizes or takes the standard deduction. IRS said in Feb. 2026 that the break sits alongside the existing standard deduction rules, not inside them.

How the $6,000 tax deduction for seniors stacks with other breaks

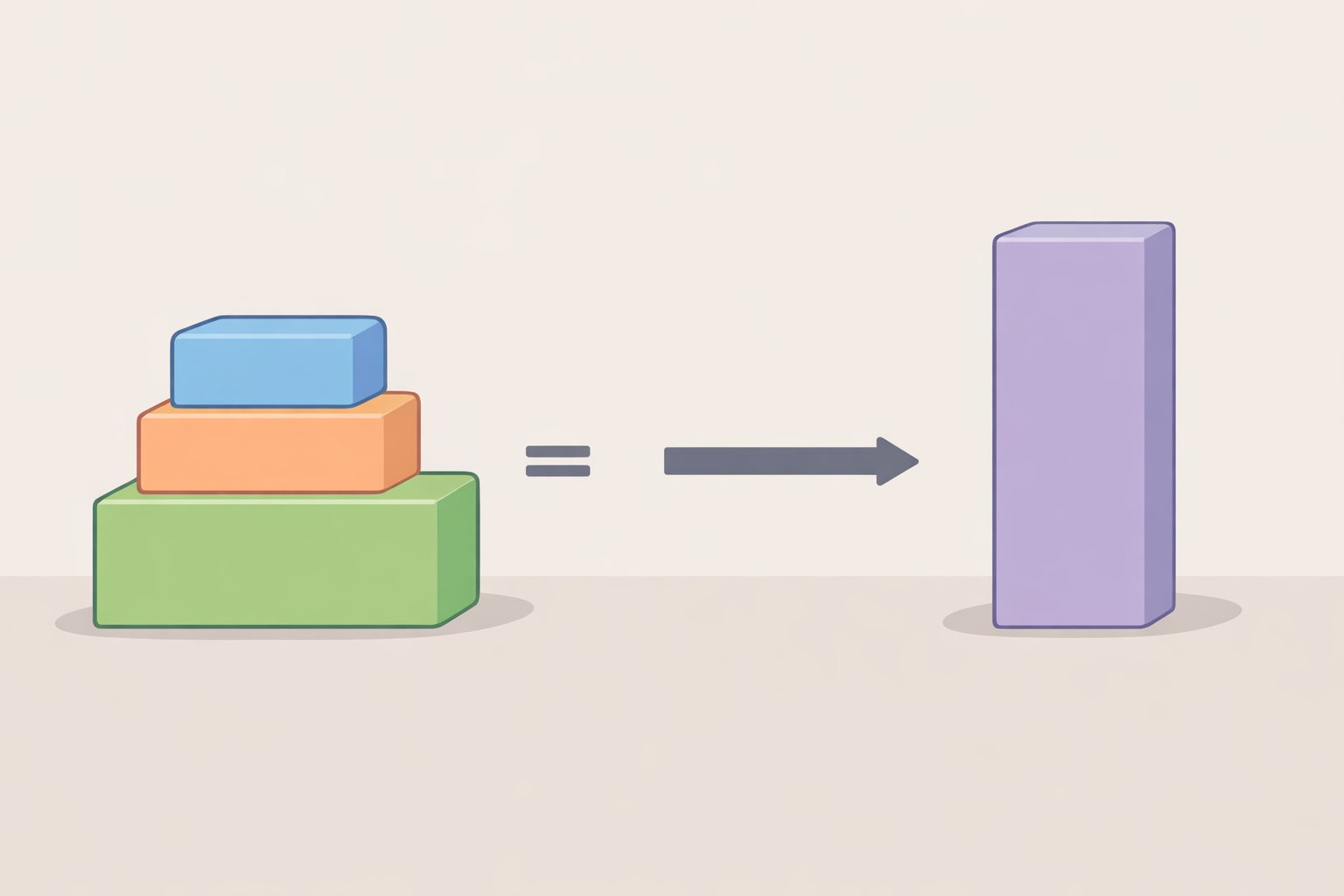

The new deduction is not replacing the standard deduction or the older extra deduction for taxpayers 65 and over. It stacks on top.

For 2025, a single filer age 65 or older can combine the $15,750 standard deduction, the existing $2,000 senior add-on, and the new $6,000 deduction. That adds up to $23,750 in sheltered income, according to IRS Publication 554 and Motley Fool.

For a married couple where both spouses qualify, the total is $46,700, using the $31,500 standard deduction, the $3,200 existing senior add-on, and the $12,000 new deduction. Motley Fool reported that figure in March 2026.

That is where the deduction gets interesting. It is not a credit, so it does not knock $6,000 straight off a tax bill. It reduces taxable income, which means the value depends on the marginal rate.

At a 12% marginal rate, a $6,000 deduction saves $720. At 22%, it saves $1,320. USA Today used those exact examples in January.

The terminology around Social Security matters, because this deduction does not touch the taxability formula itself. That formula still uses combined income, meaning adjusted gross income, tax-exempt interest, and half of annual Social Security benefits. Below the first-tier thresholds, benefits are not taxed. Between the first and second thresholds, up to half can be taxed. Above the second tier, up to 85% can be taxable. Tax Foundation laid out the structure in July 2025.

The new deduction comes after that calculation, not before it. That is why the CRS kept stressing that the deduction is separate from the determination of taxable Social Security benefits. The order of operations is the whole story.

The White House Council of Economic Advisers estimated that the deduction would raise the number of Social Security recipients owing no federal income tax on their benefits from 37.2 million to 51.4 million, or about 88% of recipients. Motley Fool reported that estimate in March 2026.

Why some retirees may not benefit much

The deduction is useful only if there is taxable income left for it to shelter. If taxable income is already wiped out by existing deductions, the new break has nowhere to go.

That is the limit of all deductions. They can reduce taxable income to zero. They cannot push it below zero, and they cannot create a refund on their own. The CRS said that plainly in August 2025.

Retirees leaning heavily on Roth accounts may feel this the most. Roth distributions are tax-free, so they do not show up in MAGI and do not help create taxable income that the deduction can erase. Motley Fool said in March 2026 that people living mostly on Roth withdrawals may find the new deduction does little or nothing.

That is not a rare edge case. About 40% of Social Security recipients currently pay income taxes on their benefits, according to an SSA-cited figure reported by USA Today in January. The rest were already outside the tax net, so another deduction may have limited practical value.

There is, however, one planning angle that has drawn attention. NewsBreak/GOBankingRates reported in February 2026 that some advisers see room for Roth conversions during the four-year window, especially for retirees with pre-tax IRA balances. The logic is simple enough: use the deduction to offset some or all of the conversion income while the provision lasts. Whether that works depends on the rest of the tax return, which is usually where the interesting part starts.

Conclusion

The social security retiree tax deduction is easy to describe once the clutter is cleared away. Be 65 or older by year-end, have a valid work-authorized SSN, file jointly if married, and stay within the MAGI limits. Then attach Schedule 1-A, because the IRS is not going to guess for you.

The deduction is real, and for retirees with moderate taxable income it can be valuable. It is also narrower than some of the headlines suggest. It does not repeal Social Security taxation, and it does not help much once taxable income is already gone.

The law runs from 2025 through 2028, IRS said in Feb. 2026. After that, the tax picture goes back to normal unless Congress decides to keep tinkering with it, which is never a thrilling bet but often the only one on offer.