- When to Consolidate Debt: Readiness, Costs, and Options

- Start with readiness, not the product

- How to know if debt consolidation is right for you

- Choose the method that fits the problem

- Watch for debt settlement dressed up as consolidation

- Use counseling when the loan math does not work

- Make the call this week

When to Consolidate Debt: Readiness, Costs, and Options

By the end of this guide, you'll know when to consolidate debt, when to leave it alone, and which option fits the mess in front of you. That means answering three questions in order: is the debt expensive enough to justify the move, is the cash flow problem under control, and does the product match the situation. Skip the order, and the loan usually just becomes another bill with better branding.

Credit cards are the main place this question comes up. Balances reached $1.28 trillion in Q4 2025, up $44 billion in a single quarter, and about 60% of credit card accounts still carry a balance from one month to the next, according to the New York Fed and Liberty Street Economics. Those balances matter because card rates averaged 23% annually in 2023, a level that is not a temporary nuisance so much as the business model.

That is the basic frame. Consolidation is a cost-cutting tool, not a cure for the habits or shocks that created the debt. If the income side and spending side are still broken, the loan just gives the problem a new payment date.

Start with readiness, not the product

The CFPB is blunt about the first test: if debt piled up because spending outpaced income, a consolidation loan probably will not help unless spending falls or income rises too, according to the CFPB. That is the part people like to skip. It is also the part that decides whether consolidation is useful or just expensive theater.

Before looking at offers, do three things.

- Check your real cash flow. Pull three months of actual spending, then compare it with take-home income. If expenses beat income most months, consolidation is not the first move. It may lower the rate, but it will not change the math that got you there.

- Figure out what caused the debt. A one-off event, such as job loss or medical costs, is different from a pattern of spending that keeps refilling the bucket. The first can be cleaned up with the right tool once income stabilizes. The second usually needs a budget fix before anything else.

- Call existing creditors first. The CFPB says some creditors may lower minimum payments, waive fees, cut rates, or shift due dates to better match payday, according to the CFPB. That is often the least glamorous option, which is usually a sign it deserves a look.

Readiness is really the dividing line between a temporary cash crunch and a structural problem. If the debt came from a short, identifiable stretch and the budget now works, consolidation may have a role. If the account balances are just a snapshot of ongoing overspending, the fix is upstream, not financial plumbing.

Consolidation is more likely to make sense when:

- Income reliably covers monthly expenses, with room left over

- The debt came from a specific event, not a habit

- You plan to stop using the accounts you consolidate

- Your credit is strong enough to unlock a meaningfully lower rate

Consolidation is probably premature when:

- Spending still outruns income

- The debt reflects an ongoing pattern

- Your credit has already been damaged enough to block good offers

- Your income or job feels unstable enough to make a fixed payment risky

The broader delinquency picture helps explain why that distinction matters. Aggregate delinquency reached 4.8% of outstanding debt in Q4 2025, and stress is not evenly spread, according to the New York Fed and the Fed. Some borrowers are managing fine. Others are already standing on the trapdoor.

How to know if debt consolidation is right for you

Once the cash flow picture is stable, the next question is boring but decisive: will the new rate actually beat what you are paying now? For credit cards, the answer often is yes. For everything else, it depends.

The structural reason is simple enough. Credit card rates averaged 23% annually in 2023, while the average spread over expected losses was 8.8 percentage points, according to Liberty Street Economics. The spread is even wider for weaker credit profiles and narrower for stronger ones. In that same analysis, borrowers with a FICO score around 600 faced a spread of roughly 21 percentage points above baseline, while those at 850 were closer to 7.22 percentage points. Your score decides how much room there is to improve.

Here is the practical version.

- List every debt you might consolidate. Write down the balance, rate, and monthly payment for each account. The point is not to make the list look tidy. It is to see which debts are expensive enough to justify a move. High-interest cards are usually the first candidates.

- Check your credit before shopping. A score around 670 or higher gives the best chance of qualifying for an interest rate below what you are already paying, according to InCharge. Below that, the offers may still exist, but the savings can disappear once fees are included.

- Compare total cost, not just the monthly bill. A lower payment can be a trap if it comes from stretching repayment over a longer term. The CFPB warns that longer repayment can mean paying substantially more overall, including fees you would not have paid if you had stayed on your existing plan, according to the CFPB.

- Run one simple test. If you are looking at a balance transfer, divide the amount you want to move by the number of months in the promotional window. If the required payment is not realistic, the promotion will end before the balance is gone. If you are looking at a personal loan, add the origination fee to the total interest and compare that number with what you would pay by attacking the current debt more aggressively.

A quick example helps. Say someone owes $18,000 on cards at 24% APR and is offered a personal loan at 11% with a 5% origination fee. The headline rate looks great, but the fee adds $900 before a single payment lands. If the new loan also stretches repayment longer than the current payoff plan, the monthly payment may fall while the total cost quietly climbs. That is the kind of trade that feels smart for a week and irritating for years.

For card debt, the rate gap is usually large enough that consolidation can work. For lower-rate debt, the gap may not be there. A car loan or mortgage often belongs in a different conversation altogether, which is just another way of saying not every debt needs the same tool.

Choose the method that fits the problem

If the numbers check out, there are three main routes. Each solves a slightly different version of the same problem, and each has its own way of going sideways.

Balance transfer cards

These can offer zero-percent or low introductory rates for a limited time, sometimes up to 21 months, according to InCharge. They work best when the balance can be cleared before the promo ends. They also come with a fee, and the CFPB says that if you use the same card for new purchases, you will not get a grace period for those charges and you will owe interest until the entire balance is paid off, including the transferred amount, according to the CFPB.

One more gotcha: if you are more than 60 days late, the card company can raise the rate on all balances, including the transferred one, according to the CFPB. That is not a clerical issue. That is the deal disappearing.

- Best fit: strong credit, short payoff window, no intention of running new charges on the card

Personal consolidation loans

These roll multiple debts into one fixed monthly payment, usually for one to five years, according to InCharge. They can be useful if you want a defined payoff date and do not want the clock ticking on a promo rate. Origination fees usually run from 1% to 8%, so they need to be included in any comparison, not waved away like annoying small print.

The risk is that a lower payment can hide a longer repayment period. The CFPB makes the point plainly: monthly relief can mean a higher total bill, especially once fees and interest are counted, according to the CFPB.

- Best fit: credit around the 670 range or better, preference for a fixed structure, no collateral at stake

Home equity loans

These borrow against home equity, which is why the rate may be lower. They also turn unsecured debt into debt secured by the house, and that changes the stakes fast. The CFPB says you could lose your home in foreclosure if you do not repay, and you may also have to pay closing costs that can run into the hundreds or thousands, according to the CFPB.

The New York Fed says HELOC balances increased by $11.6 billion to $434 billion in Q4 2025, while HELOC limits rose by $25 billion, continuing an expansion that began in 2022, according to the New York Fed. That tells you the product is active. It does not tell you it is wise.

- Best fit: substantial stable equity, reliable income, full understanding of the foreclosure risk

Watch for debt settlement dressed up as consolidation

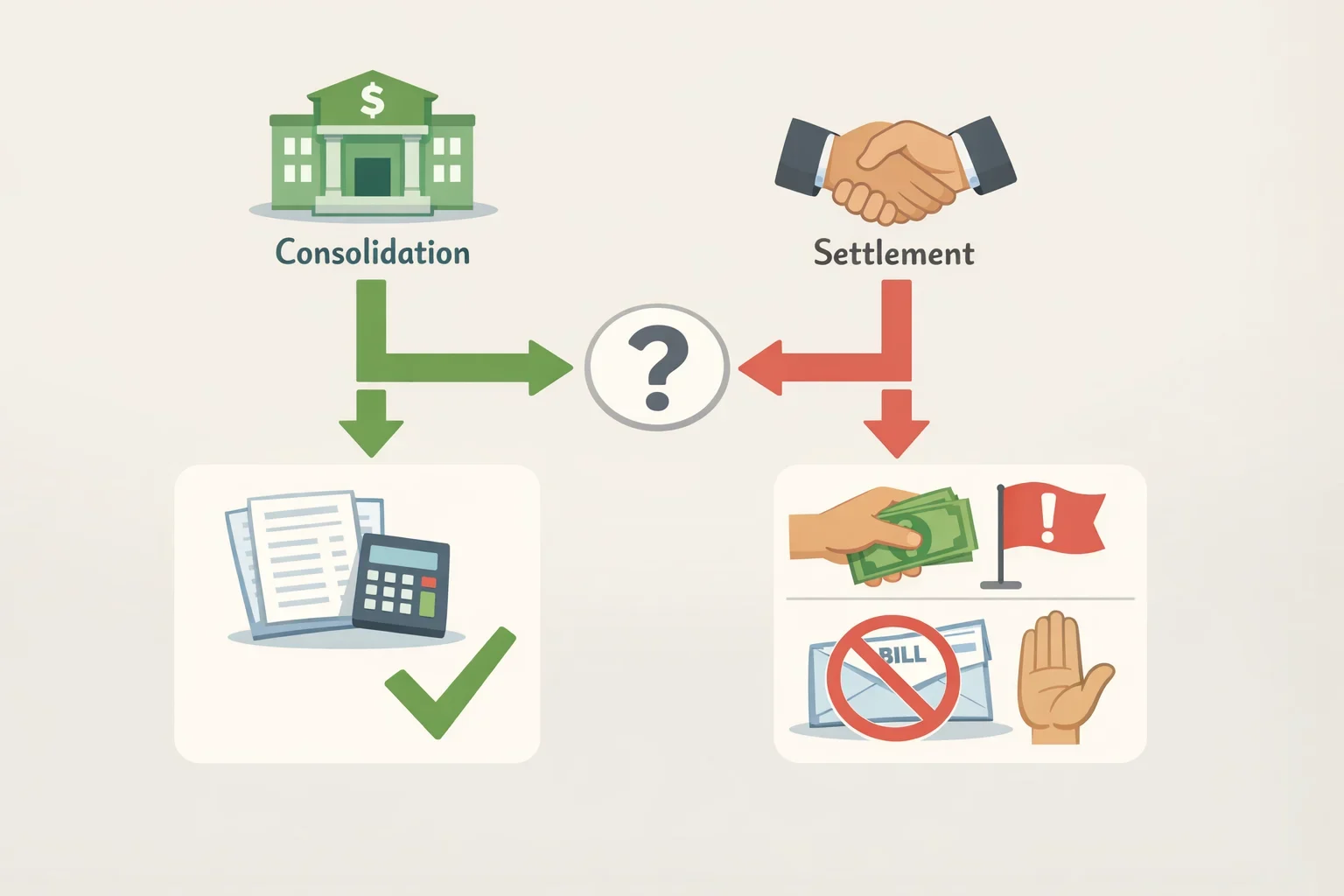

There is one more thing to sort out before signing anything. Some companies that advertise consolidation are really debt settlement operators, and the CFPB says they may charge upfront fees and even push people to stop paying creditors while money is moved into a special account, according to the CFPB. That is not the same thing as consolidation. It is a different product with a different risk profile.

If the pitch sounds too slick, read it twice. Consolidation means borrowing to pay off debt. Settlement means trying to negotiate down what you owe, often by following a much rougher path.

Use counseling when the loan math does not work

There is a fourth option that gets buried in most product pages: debt management plans through nonprofit credit counseling. These do not require a loan application or a credit check, and InCharge says creditors may agree to lower interest rates to around 8%, sometimes lower. The CFPB also recommends nonprofit credit counselors as a first resource for people evaluating their options, according to the CFPB.

That matters for borrowers who have the income to repay debt but not the credit profile to get a workable consolidation offer. A good counseling session can show whether the path is a loan, a management plan, or simply a stricter budget and a few uncomfortable phone calls. The session is typically free, and InCharge says it can be done over the phone or online.

Make the call this week

If the debt is expensive, your budget is stable, and the rate savings are real, consolidation can make sense now. If the problem is still cash flow, use the next few months to fix that first. If the loan offers are weak or your credit is too bruised, talk to a nonprofit counselor instead.

The cleanest rule is the oldest one in the CFPB guidance: do not use new debt to bury old debt unless the conditions that created the old debt have changed too, according to the CFPB. Credit card rates are high enough to make the math tempting, and for some borrowers, the savings are real. The trick is knowing when the math is working, and when it is just being optimistic.