When Federal Student Loan Consolidation Helps (and Hurts)

Federal student loan consolidation can solve a real problem. It can also erase progress a borrower has spent years making, which is why the decision is rarely neutral.

The simplest way to think about it is this: consolidate if you need access to a program or loan structure you otherwise cannot get, and avoid it if you already have qualifying progress worth protecting. That is the whole game. Everything else is detail.

What consolidation does

Consolidation combines eligible federal loans into one new Direct Consolidation Loan. The old loans are paid off and replaced by a single new loan with its own terms.

That new loan is not just an administrative wrapper. It is a fresh account, and that matters because a fresh account can change how repayment history is treated and how the loan fits into future repayment options. A move that looks tidy on a servicer dashboard can still change the borrower’s position in a material way.

It also changes the shape of the debt itself. Any unpaid interest tied to the old loans can be added into the new balance, which means the borrower can begin the consolidated loan owing more than they did the day before. That is not a bookkeeping detail. It is the part that makes consolidation more than a paper shuffle.

The risks that matter most

Forgiveness progress can be lost

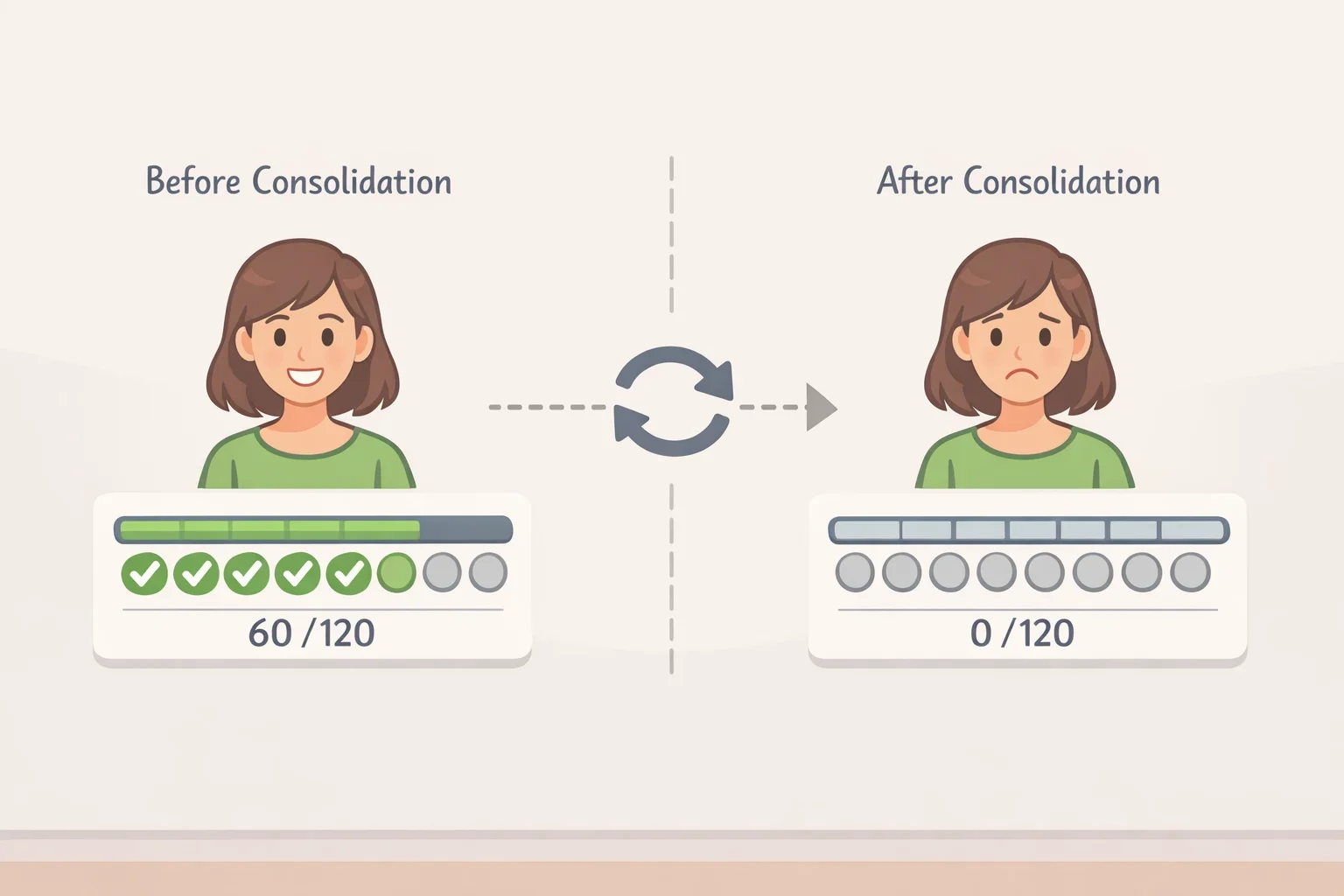

The biggest danger is losing credit toward forgiveness. For borrowers working toward income-driven repayment forgiveness or Public Service Loan Forgiveness, consolidation can reset progress because the new loan does not automatically carry over the payment history attached to the old ones.

That is why consolidation is especially risky once a borrower has already made meaningful progress. A borrower close to forgiveness can turn a short remaining stretch into a much longer one. The debt may look cleaner, but the road back to forgiveness can get a lot longer.

A simple example shows the problem. A teacher who is a few years into PSLF-qualifying payments and then consolidates at the wrong time may find that the new loan starts counting from zero. That is not a minor adjustment. It is the difference between finishing soon and starting over.

Repayment plan access can change

Consolidation can also change which repayment plans are available. That is one reason it can be useful for borrowers whose current loan mix blocks access to the plan they need.

But the reverse is also true. A borrower who consolidates without checking the resulting options can end up with fewer choices than expected. In student loans, the form you choose often matters as much as the balance you carry. The loan may be federal either way, but that does not mean the menu of repayment paths stays the same.

Parent PLUS borrowers need particular caution here. Their repayment options are often narrower than those for standard Direct Loans, so consolidation should be treated as a route change, not a simple cleanup step. If the borrower does not know what the new loan can and cannot do, the decision is premature.

Interest can be added to the balance

The most predictable cost is interest capitalization. Unpaid interest can be added to principal at consolidation, and once that happens, future interest accrues on a larger amount.

That can make the loan more expensive from day one. A borrower with a significant interest balance is not just rearranging debt, they are potentially converting old unpaid interest into new principal before making the first payment on the consolidated loan.

Borrowers who have spent long stretches in forbearance, or who simply have not paid down interest for a while, should check the accrued interest figure before consolidating. If that number is large, consolidation may be a costly move even when it solves an access problem.

Which risks are inherent, and which depend on the rules

Not every consequence works the same way.

Loss of forgiveness progress is the most serious risk because it is tied to the act of consolidation itself. If a borrower consolidates while sitting on qualifying history, the problem is not theoretical. The borrower has traded away old progress for a new loan structure.

Repayment plan access is more conditional. It depends on the loan type involved and the rules in effect at the time the new loan is created. That makes it a moving target, which is exactly why borrowers should not assume consolidation will preserve the same options they had before.

Interest capitalization sits in a different category again. It is the most concrete cost because it can change the balance immediately. No elaborate legal analysis is needed to see why that matters. A larger principal amount means a larger amount on which interest can accrue later.

Who should be most careful

Borrowers with years of qualifying payments should be the most cautious. If the loan is already moving toward forgiveness, consolidation can replace a nearly finished track with a new one. That is a bad trade unless the borrower truly needs access to something the current loans cannot provide.

Parent PLUS borrowers also need to slow down and check the details. Their repayment choices are often more limited, so the question is not just whether consolidation is possible, but whether it opens the right door or the wrong one.

Borrowers carrying significant unpaid interest should think through the balance effect before they act. The temptation is to focus on simplification, but the larger balance can be the cost that survives long after the paperwork is done.

When consolidation still makes sense

There are cases where consolidation is the right call.

The clearest one is when a borrower holds older federal loans that do not already fit the repayment or forgiveness program they need. In that situation, consolidation may be the only path into the loan structure that unlocks access. If the borrower is early in repayment and has little or no qualifying history to lose, the reset risk is small compared with the benefit of getting into the right program.

Borrowers with several loans and no meaningful forgiveness progress may also find consolidation useful. Fewer loan accounts can mean simpler billing and a cleaner repayment setup. That is a practical benefit, especially when there is not much interest sitting unpaid on the account.

But that does not make consolidation a default good idea. The decision only works when it solves a real problem. If the borrower already has access to the repayment path they want and has built up qualifying progress, the case for consolidating weakens fast.

A cleaner way to decide

The easiest mistake is deciding based on convenience. The better approach is to check three things first.

- What kind of loans are in the mix?

- How much qualifying payment history exists?

- How much unpaid interest would be rolled into principal?

Those three numbers tell most of the story. They show whether consolidation is unlocking access, or simply trading away value the borrower already has.

A borrower who holds older federal loans and has little or no qualifying history may have a straightforward answer. Consolidation can make sense if it opens the path to the program they need.

A borrower with Direct Loans and years of qualifying payments is in a different position. For that borrower, consolidation should be treated as a high-stakes move, not a tidy-up task. The risk is not abstract. It is the loss of hard-won progress.

Borrowers with large interest balances fall somewhere in between. Consolidation may still be the right choice, but only after the numbers are clear. If the borrower cannot live with the new principal amount, the answer is already visible.

The July 1 question

July 1 often matters in federal student aid because it is a common point at which new rules and annual adjustments take effect. That makes it a date borrowers watch closely.

Still, the date itself is not the main issue. The real question is whether a borrower is consolidating under rules that help or rules that hurt. A move that is reasonable under one framework can be a mistake under another, especially when loan types and repayment access are shifting.

That is why consolidation should not be treated as a generic administrative choice. Timing matters, but only because it changes the consequences attached to the loan. The calendar is not the point. The loan history is.

Bottom line

Consolidation is worth considering when it gives a borrower access to a repayment or forgiveness path they otherwise cannot reach. It is much harder to justify when the borrower already has the right loan type, meaningful qualifying progress, and unpaid interest that would be folded into principal.

Before acting, borrowers should know the loan types they hold, how much qualifying history they have built, and how much interest is sitting unpaid. Those are the numbers that determine whether consolidation is a useful tool or an expensive mistake.