Judge blocks Trump student loan caps—Grad PLUS on hold

A federal judge has blocked the Trump administration’s graduate and professional student loan rule, stopping a set of borrowing caps that was due to begin on July 1, 2026, just days from now. For students heading into programs this fall, that means Grad PLUS remains available for the moment, and the hard new federal student loan limits for graduate students are on hold while the case moves forward.

The immediate practical effect is simple enough, even if the legal file is not. Schools should not be treating the July 1 changes as a done deal yet, and aid packages built around the coming caps may need to be adjusted if the block holds.

The Department of Education finalized the rule on April 30, 2026, to implement the student loan provisions of the Working Families Tax Cuts Act, which Congress passed in July 2025. The department said the new regulations would cap borrowing for graduate and professional students, eliminate new Grad PLUS loans for borrowers who do not qualify for an interim exception, and set new limits for Parent PLUS loans too, per the ED fact sheet published in May 2026.

What the judge’s block means for graduate student loan borrowing caps

For now, the rule’s July 1 start date is paused. Graduate and professional students who would have lost access to Grad PLUS can still borrow under the current system until the court says otherwise.

The department’s own fact sheet carved out one narrow interim exception that would have protected borrowers already enrolled in a program before July 1, 2026, and who had already taken a loan for that program, according to the ED fact sheet published in May 2026. The court’s order makes that distinction temporarily less important, but it may matter again if the block is narrowed or lifted.

That leaves three groups watching closely. Current students who had already borrowed were already covered by the rule’s exception. Students starting a new program this fall are the ones who stood to lose the most if the rule took effect. Future applicants remain in limbo, because the legal fight is about whether the regulations can stand, not whether Congress passed the law that set them in motion.

The legal and policy timeline is easy to blur, so it helps to separate the pieces. The law came first in July 2025. The Education Department’s final rule followed in April 2026. The effective date was July 1, 2026, and that is the date the judge has now stopped, at least for the moment.

How the blocked rule would have changed federal borrowing

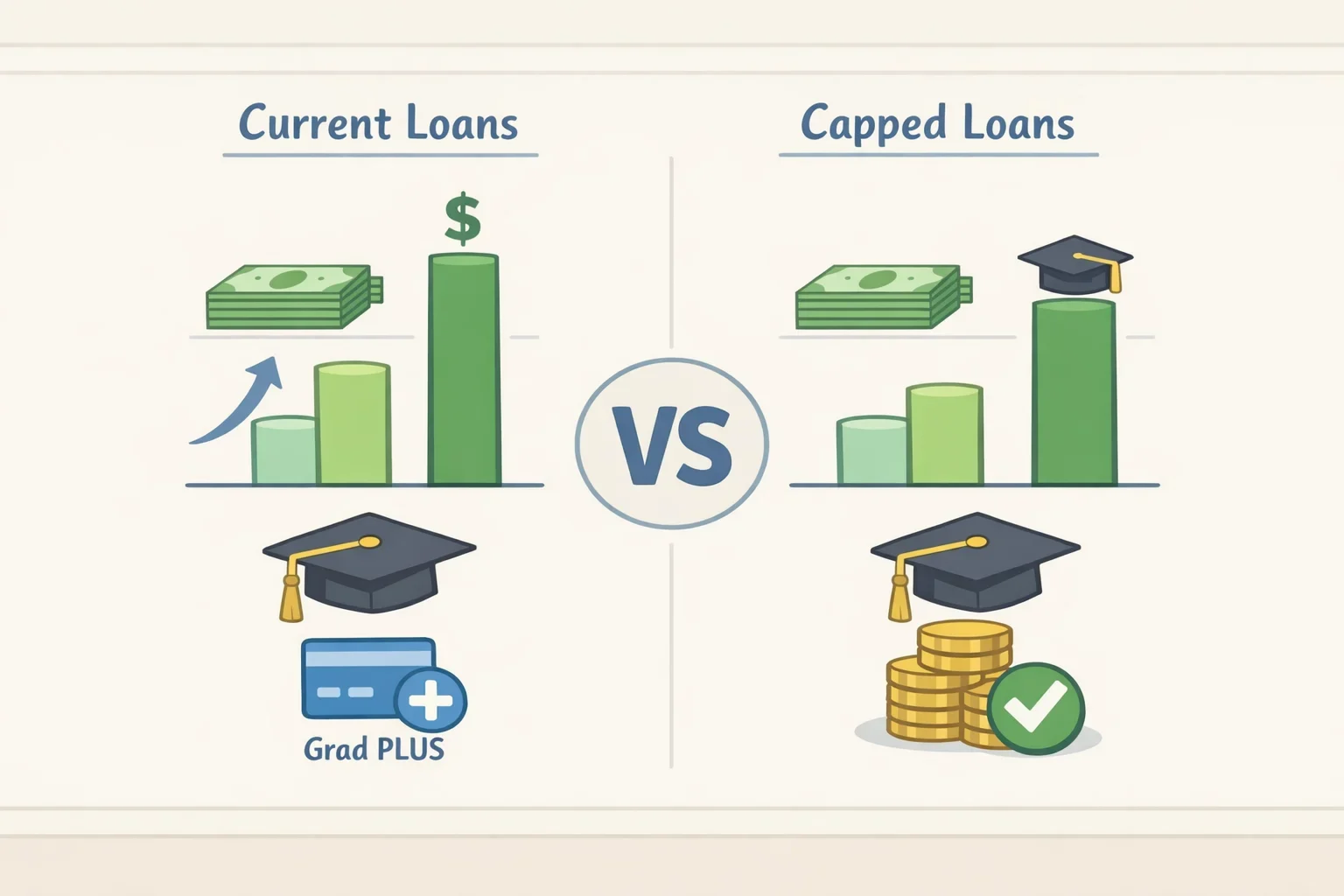

The rule would have capped graduate student loans at $20,500 a year and $100,000 in total, while professional students would have faced a $50,000 annual cap and a $200,000 aggregate limit, per the ED fact sheet. It also would have put a lifetime borrowing limit of $257,500 on loans made on or after July 1, with Parent PLUS loans excluded from that lifetime tally, according to the same fact sheet.

The headline numbers sound tidy. The reality is a little less polite. Limits are prorated for students who attend less than full time, and the Urban Institute noted that a typical two-year full-time master’s program would, in practice, be capped at about $41,000 rather than the $100,000 aggregate figure that appears on paper, the Urban Institute found in July 2025.

Grad PLUS was the real pressure valve. Under the current system, graduate students can borrow up to the full cost of attendance through the program, the Urban Institute noted in July 2025. The blocked rule would have ended that option for new borrowers who did not qualify for the interim exception, forcing them to patch together private loans, savings, or a less expensive plan.

One unresolved wrinkle was classification. The department’s distinction between “graduate” and “professional” programs determines whether students fall under the $20,500 cap or the higher $50,000 limit, and Brookings noted in November 2025 that the list was still subject to public comment before the final rule. That matters because a program placed on the wrong side of the line can cut borrowing room almost in half. College bureaucracy rarely makes a simple thing simpler.

Which programs would have felt the squeeze first

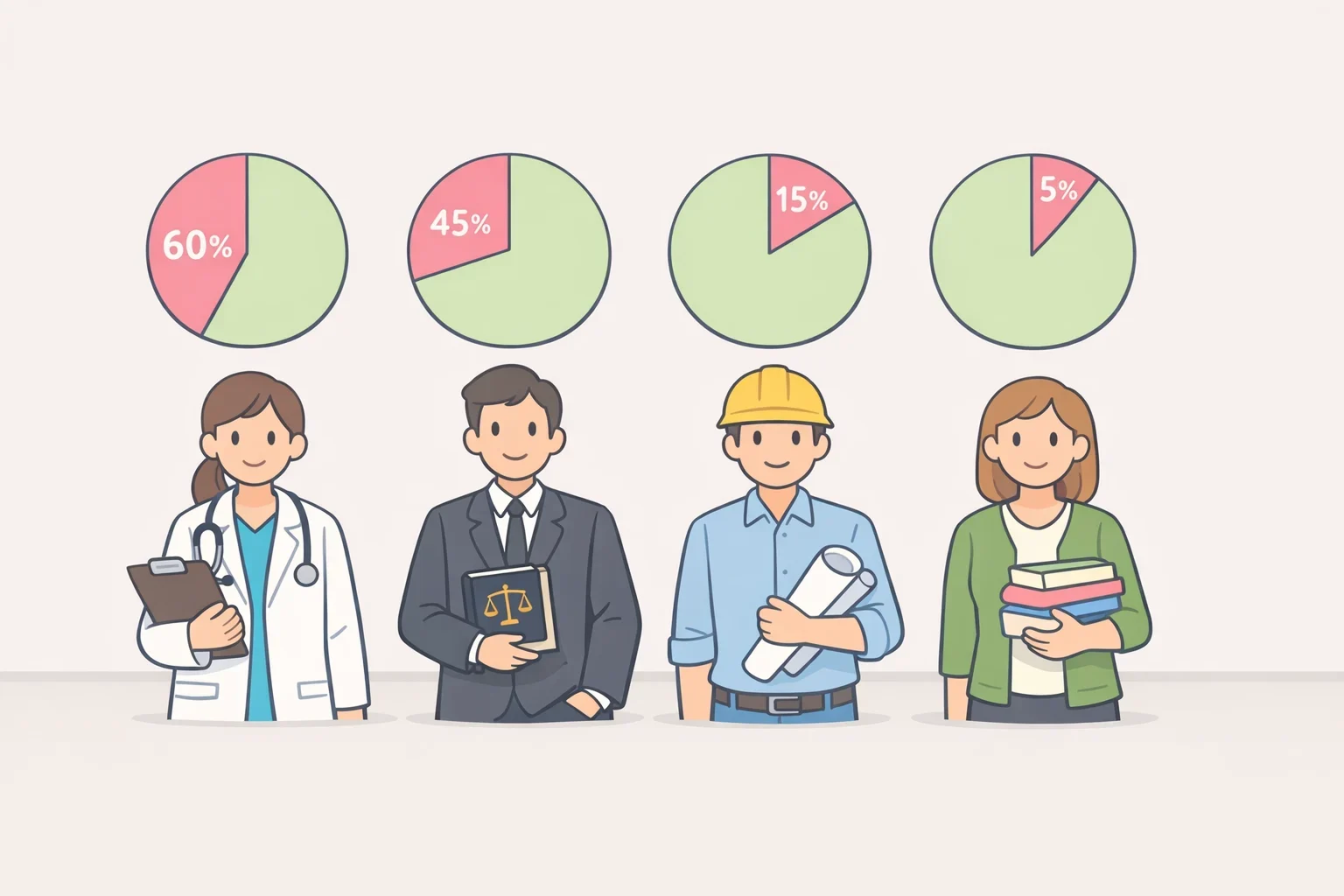

Dentistry would have been hit hardest. The Urban Institute estimated in July 2025 that 56% of full-time dentistry students borrowed above the new $50,000 annual cap in 2019-20, and 58% of dentistry graduates that year carried debt above the proposed $200,000 aggregate limit, the Urban Institute found in July 2025.

Medicine and osteopathic medicine were not far behind, with 41% of students borrowing above the annual limit, according to the Urban Institute’s July 2025 analysis. At least one in five students in veterinary medicine, optometry and law would also have been affected by the annual cap, the Urban Institute found in July 2025.

The pain would not have been confined to high-salary professions. More than half of students borrowing for a master’s in public health were already above the new annual cap, and 29% of public health students, 26% of fine arts students and 24% of social work students were above it too, the Urban Institute reported in July 2025. Those are fields where graduates often do not walk straight into lavish paychecks, which is part of the problem.

The burden also falls unevenly by income. In professional practice programs, 38% of former Pell Grant recipients would have been affected by the annual cap, compared with 25% of non-Pell students, the Urban Institute found in July 2025. In master’s and academic doctoral programs, the gap was 17% versus 10%, according to the same analysis. Students with less family wealth do not get many clean exits when federal lending tightens.

There is also no built-in inflation adjustment. The Urban Institute noted in July 2025 that undergraduate loan limits have been frozen since 2008 and have lost more than 20% of their real value over that period, the Urban Institute reported in July 2025. If the graduate caps remain fixed, they will erode too.

What happens next

The judge’s order is a pause, not a final answer. The Working Families Tax Cuts Act still exists, and the Education Department’s regulations still exist on paper, even if their July 1 start date is now blocked.

That is why the court fight matters so much for students in high-cost programs, especially dentistry, medicine, law and public health. If the injunction is narrowed or lifted before fall enrollment is locked in, the caps and the end of new Grad PLUS loans could still come back into play, per the terms of the ED final rule. Financial aid offices may have to rewrite award letters before the semester even starts.

A few things are worth watching over the next several weeks:

- Education Department guidance: Schools are likely updating aid packages now. Students should check whether any award depends on Grad PLUS and whether it could change.

- The court docket: The government could appeal, seek faster action, or ask for a narrower order. The duration of the block matters as much as the block itself.

- Program classification rules: If the regulations return, the fight over which programs count as “professional” will still shape who gets the higher borrowing limit, Brookings noted in November 2025.

For the moment, graduate borrowers have been given a little more breathing room than they expected this week. That relief may be temporary, but it is real enough for anyone about to sign an enrollment deposit.