Is an MBA still worth it? ROI as salaries cool

The short answer is yes, for some applicants and not for others. That is the point this year, and it is why the question is an MBA still worth it deserves a harder look than a single salary average can give it.

The MBA market has cooled since the post-pandemic hiring rush, but the story is not simple collapse or even broad decline. AACSB’s most recent survey puts average MBA starting pay across accredited programs at $68,014 for 2024–25, down from $89,657 the year before, while U.S. MBAs in GMAC’s regional data were closer to $125,000 and Western Europe was far lower at $38,000 (AACSB, nine months ago). That spread is the problem. The average is doing too much work.

The smarter way to ask the question is more specific: which MBA, at what cost, for what outcome? Once that is clear, the salary debate becomes less noisy and a lot more useful. It also explains why one graduating class can look flat on paper while elite programs still look healthy.

MBA return on investment in 2026

The clearest sign of cooling is at the top of the market, where salaries are still strong but no longer racing ahead. Clear Admit’s latest look at the seven M7 schools shows average median base salaries rising 40% over the last decade, from $128,143 for the Class of 2016 to $179,214 for the Class of 2025 (Clear Admit, this month). That is still a real gain after inflation, which the same report puts at 33.4% over the period, leaving roughly 6.6% of actual purchasing-power growth (Clear Admit, this month).

But the momentum has faded. Clear Admit says M7 salaries had 6.3% real growth in 2022, then fell to -1.3% in 2023 and -3.4% in 2024, before 2025 came in about even at -.3% (Clear Admit, this month). That is not a crisis. It is a sign that the easy part of the cycle is over.

The elite schools also remain clustered near the top of the pay scale. Harvard, Stanford and Wharton were close to a $185,000 median base salary in 2025, while Booth, Columbia, MIT Sloan and Kellogg were at a $175,000 median base salary (Clear Admit, this month). In other words, the M7 is not moving in lockstep, but it is still a different labor market from the broader MBA pool.

That is why the AACSB average is useful only as a warning label. It tells you the market is mixed. It does not tell you whether a top program, or a local part-time one, makes sense for a specific candidate. Even its regional comparison makes the point: GMAC data cited by AACSB shows average MBA salaries of $125,000 in the United States, $55,000 in Canada and $38,000 in Western Europe, while Oxford Saïd’s average MBA salary was 74,143 GBP, or $99,000 (AACSB, nine months ago). A global average across that kind of spread is more fog than signal.

Employment numbers still argue against any dramatic read on the degree. AACSB says full-time MBA employment three months after graduation was 85% in 2024–25, down from 87.5% the year before, which suggests some softening but not a collapse (AACSB, nine months ago). That matters because salary headlines can obscure the more basic question: are graduates still getting hired? For now, the answer is yes.

The real change is simpler than the headlines make it sound. The MBA still pays, but it no longer pays automatically. Timing, school tier and geography now matter more than they did when demand was roaring.

Why the long-term MBA salary outlook still holds up

Short-term salary data can make the degree look flatter than it is over a career. The long view is where advocates of the MBA make their strongest case, and where the evidence is best handled with a little skepticism.

The University of Iowa’s Tippie College of Business cites a Forte Foundation study projecting MBA salaries rising between 9% and 35% over the ten years after graduation (University of Iowa/Tippie, 2024). It also cites GMAC alumni survey data showing that 84% of respondents said a graduate degree improved their professional situation, while two-thirds advanced at least one job level after graduation (University of Iowa/Tippie, 2024). Those are self-reported outcomes, not controlled experiments, so they show direction more than proof. Still, the pattern is hard to ignore.

The same source points to a 2021 analysis cited by Poets & Quants that estimated an MBA could be worth up to $2.3 million more than a bachelor’s degree over a lifetime, and says lifetime median cash compensation for MBA graduates from the top 50 business schools is more than $5.7 million over 35 years (University of Iowa/Tippie, 2024). Those figures are useful as a ceiling, not a promise. They do not account for forgone income, debt service or the possibility that the same person might have done just fine on another path.

There is also a practical reason the degree still has staying power. AACSB’s data show specialized master’s graduates with just over 70% employed or holding offers within three months, rising to 85% after six months, while MBA graduates were already at 85% after three months (AACSB, nine months ago). That timing gap is not trivial for anyone paying tuition, borrowing heavily or stepping away from a paycheck.

The strongest case for the MBA, then, is not that it guarantees a higher salary next month. It is that, used well, it can change the slope of a career. For candidates with a clear target and the right school fit, that is still a credible investment.

Where the MBA still pays, and where it does not

Not all MBAs are trying to do the same job. That sounds obvious, but a lot of degree advice skips over it and jumps straight to salary bragging rights.

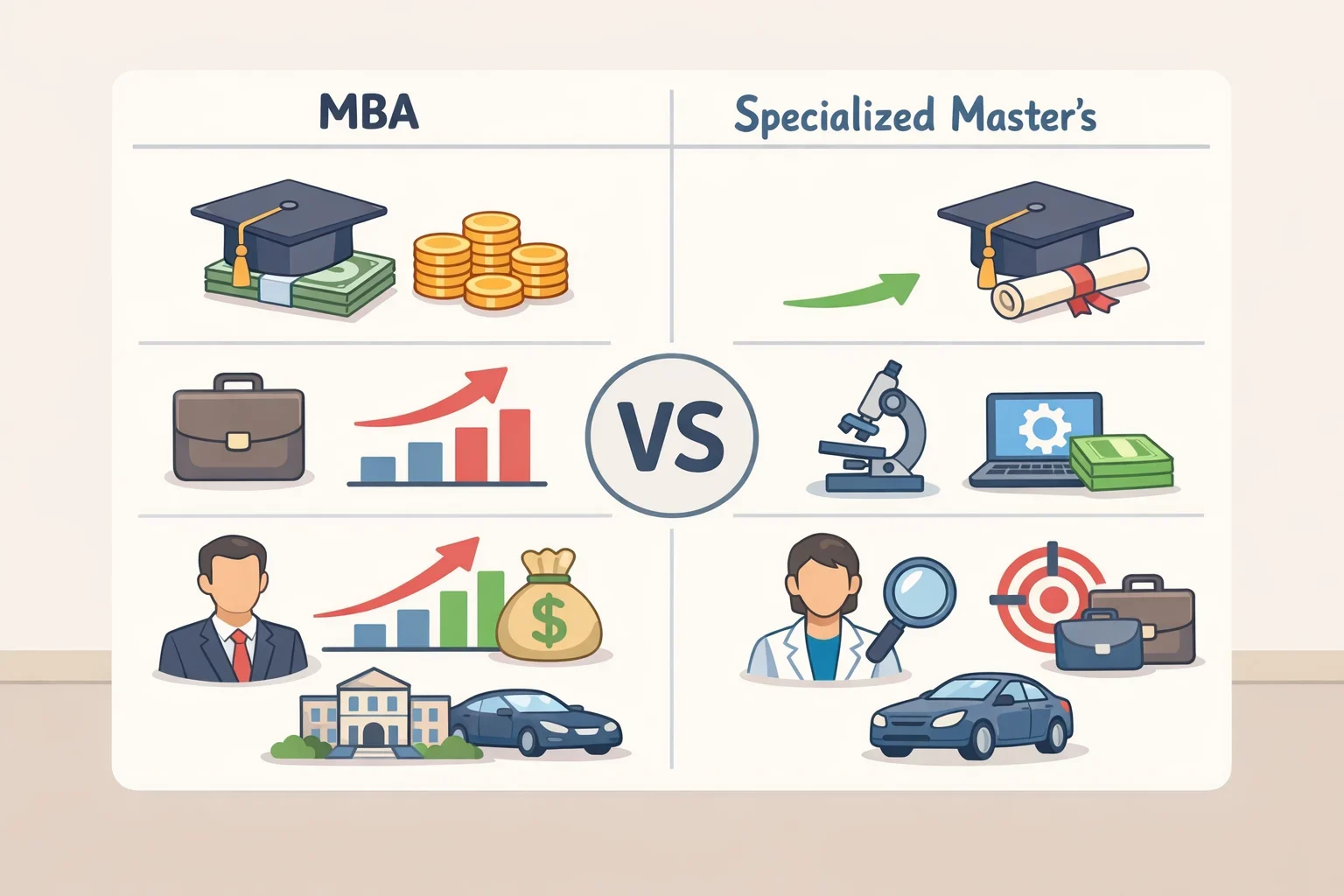

For a career switcher aiming at consulting, investment banking or brand management at large consumer companies, the MBA remains a strong filter. Those industries recruit through established pipelines, and the degree buys access to firms that do not usually hire off-cycle or outside campus channels. That access is the product, not just the salary at the end of it.

The case is weaker for someone already on a strong track in tech, engineering or specialized finance. If the employer is paying, or if the degree unlocks a specific strategic or general-management role, it can still make sense. If the main goal is a raise, the math gets tighter fast. Specialized master’s degrees often cost less and can deliver similar starting pay without a two-year earnings gap.

That is visible even in the broad salary data. AACSB says specialized business master’s graduates averaged $66,435 in 2024–25, compared with $68,014 for MBAs, a gap of only about $1,600 (AACSB, nine months ago). Pay alone does not explain why someone would choose one path over the other. The difference is more often about function, mobility and recruiting access.

Business undergraduates averaged $63,905, and AACSB says that number has increased steadily over the past few years (AACSB, nine months ago). That makes the ladder easier to see. The MBA earns its premium when a candidate needs the generalist credential to open doors that functional expertise alone will not.

Cost changes the answer just as much as school tier. Tippie notes that tuition can range from $20,000 to over $100,000 across MBA programs, and also points to Iowa’s own MBA tuition of $33,750 as a lower-cost example (University of Iowa/Tippie, 2024). That spread is enormous. It means two people can say they “got an MBA” and be talking about completely different financial decisions.

A full-time program is hardest to justify when it comes with large debt and only a modest salary increase. A part-time or online MBA changes the equation by preserving income and reducing the opportunity cost of leaving work. Tippie says online MBA programs can be equally valuable if they are accredited and reputable (University of Iowa/Tippie, 2024). The tradeoff is real, though: less immersive recruiting, less networking intensity and, in some markets, a different signal to employers.

The break-even test is not mystical. If the post-MBA salary uplift, over a few years, comfortably covers tuition, lost wages and debt service, the degree is easier to defend. If it does not, the credential may still make sense for other reasons, but the financial case is thinner. That is not cynicism. It is arithmetic.

How to judge your own case

The cleanest way to think about the MBA now is by candidate type.

A switcher headed into a field that hires through campus pipelines usually gets the strongest return. Access matters there, and the degree can do more than raise pay.

A high-performing professional with a solid trajectory has to be more selective. The MBA can still help, especially if an employer helps pay for it or a specific role requires it, but the degree no longer wins by default.

A candidate looking at a regional, part-time or online accredited program should focus less on brand and more on local employer relationships, debt load and the likelihood of promotion where they already work. That version of the degree can be the smartest one in the room. It just does not always get the loudest headlines.

So, is an MBA still worth it?

Yes, but only under the right conditions. The degree is not fading; it is stratifying. The top programs still post strong salaries, employment remains solid, and the long-term earnings case has not disappeared. What has disappeared is the illusion that any MBA, at any price, pays back the same way.

That leaves a better question than the one that gets the clicks. Does this specific program have the employer access, the cost structure and the career upside to justify the sacrifice? If the answer is yes, the MBA still works. If the answer depends on wishful thinking, it probably does not.