- Should You Buy SpaceX IPO Stock? Valuation Insights

- SpaceX stock valuation: a strong business at a hard price

- Is the SpaceX IPO overvalued? The bull case leans on unbuilt things

- SpaceX IPO risks that retail buyers should not skip

- How to invest in SpaceX IPO stock if you cannot buy it directly yet

- What patient investors should watch after the IPO

Should You Buy SpaceX IPO Stock? Valuation Insights

If you’re asking should you buy SpaceX IPO stock, the short answer is this: the company looks excellent, but the offering price appears to assume a lot of success that has not been earned yet. SpaceX is not being sold as a bargain. It is being priced as if several hard things are already nearly solved.

That distinction matters because SpaceX is the kind of business that can make almost any valuation deck look plausible. It has a real moat, a fast-growing satellite network, and a launch franchise that changed the economics of getting to orbit. The question for public investors is narrower and less romantic: does the IPO price already bake in too much of the future?

SpaceX stock valuation: a strong business at a hard price

Start with what SpaceX actually is today. Morningstar reported this week that the company has more than 80% global share of mass delivered to orbit and has cut launch cost per kilogram by more than 95%. That is a serious industrial advantage, not a PowerPoint trophy.

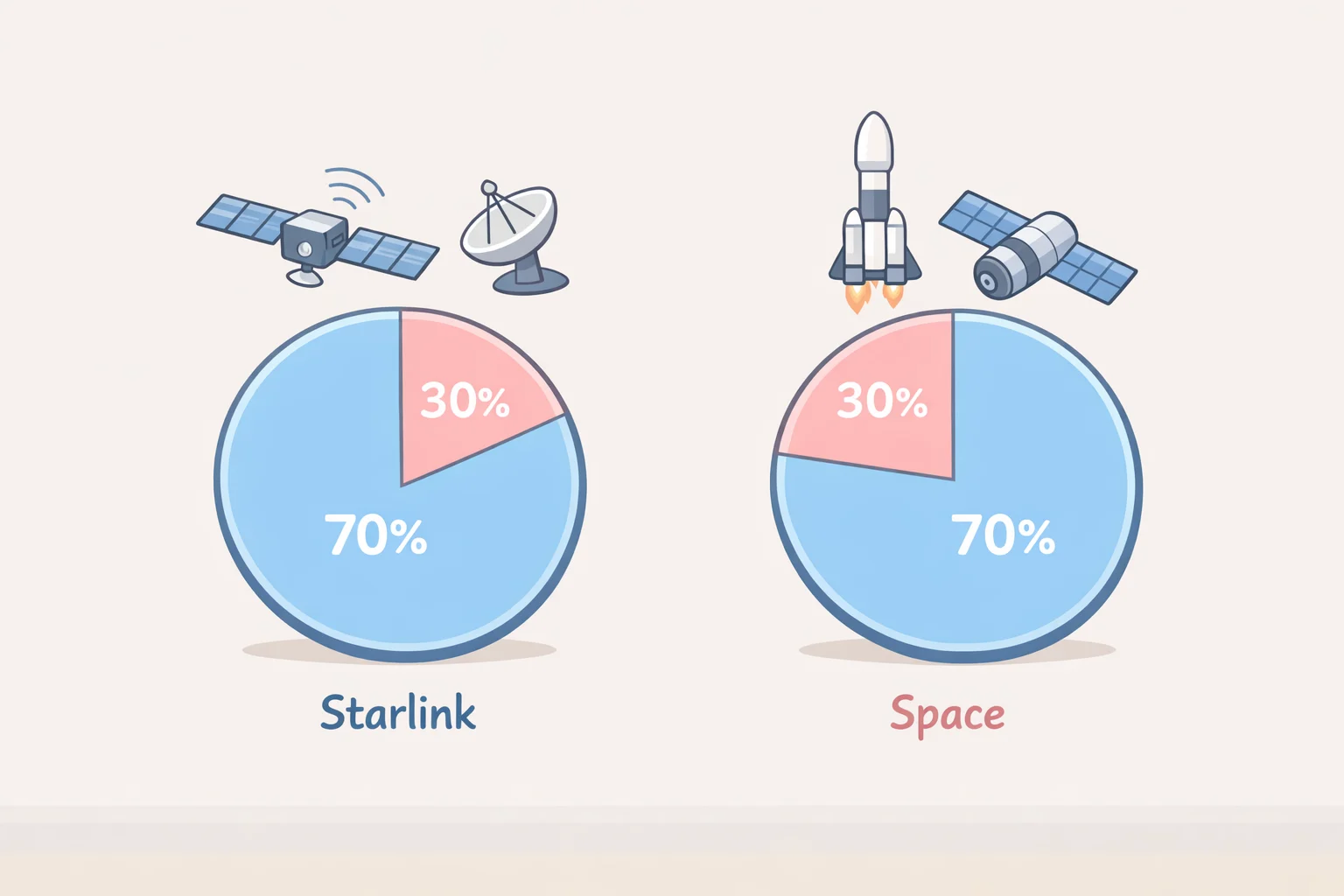

The revenue mix is more grounded than the headline valuation suggests. Investing.com reported last month that Starlink brought in about $11.4 billion in 2025, or roughly 61% of total revenue, while the space segment generated about $4 billion. Starlink matters because it is subscription-based, which gives SpaceX something rare in aerospace, a recurring revenue stream built on its own orbital infrastructure.

That business is still growing. Investing.com also reported that Starlink subscribers roughly doubled year over year to 10.3 million by early 2026, while average revenue per user fell from about $99 in 2023 to around $66. That is a useful reminder that fast subscriber growth is not the same thing as clean pricing power. The line can still go up while the unit economics get messier.

Morningstar’s own valuation lands far below the IPO talk. It values SpaceX at $63 per share, a 53% discount to the expected offering price. Morningstar also puts the company at about $780 billion, roughly 48% below the private-market valuation cited in its earlier note. If the IPO is priced at $135 a share, Morningstar says investors are paying $72 per share in “option premium,” meaning they are paying now for future projects that may or may not pay off.

That is the whole tension in one number. Morningstar says that to justify $135 on its own framework, its fair value estimate would have to be $270 per share. That is more than four times its $63 estimate, which is a polite way of saying the spread is not small enough to ignore.

Is the SpaceX IPO overvalued? The bull case leans on unbuilt things

The bull case for SpaceX is not really about today’s Starlink cash flow. It is about what SpaceX might do next, and whether those next steps can be executed at scale.

Investing.com reported that the IPO filing reportedly puts the company’s total quantifiable opportunity at $28.5 trillion and describes it as the “largest actionable market in human history.” That is a dramatic phrase, and also a forecast. Forecasts can be useful. They can also become very expensive wallpaper.

Morningstar’s scenario work shows why the price is so sensitive to assumptions. In its most optimistic “moonshot” case, SpaceX would be worth $1.97 trillion, or $154 a share. Morningstar assigns that outcome a 7% chance. That case assumes Starship is reusable and scaled orbital data centers are highly successful.

Morningstar then does something more useful than hand-waving. It backs into the probability mix needed to make $135 work at all. Using its own scenario framework, the IPO price only clears if the moonshot case is reweighted to 77% and the minimum-viable-product case to 23%, with the no-go case excluded. That is not a forecast. It is a stress test of how much optimism the market is already charging for.

The technical hurdles are not abstract either. Morningstar says the challenge is to build heat-shield materials that can withstand 1,800 degrees Fahrenheit and the stresses of reentry without time-consuming or costly remanufacture, while also solving upper-stage recovery mechanics. Neither problem has been solved, and Morningstar does not expect them to be solved until at least 2028.

That makes the timing awkward for buyers at the open. You would be paying now for engineering that may not be ready for several years, at a valuation that already assumes a lot of it works.

Morningstar’s middle case is more plausible and less glamorous. It deems the minimum viable product scenario the most likely, though far from guaranteed. In that version, orbital data centers prove viable but limited, and SpaceX captures about 4% of its forecast global AI compute capacity, mainly in latency-tolerant uses. Morningstar values that scenario at $23.50 per share, or $11.75 on a probability-weighted basis.

That is a real contribution. It is just not the same thing as paying up for inevitability.

SpaceX IPO risks that retail buyers should not skip

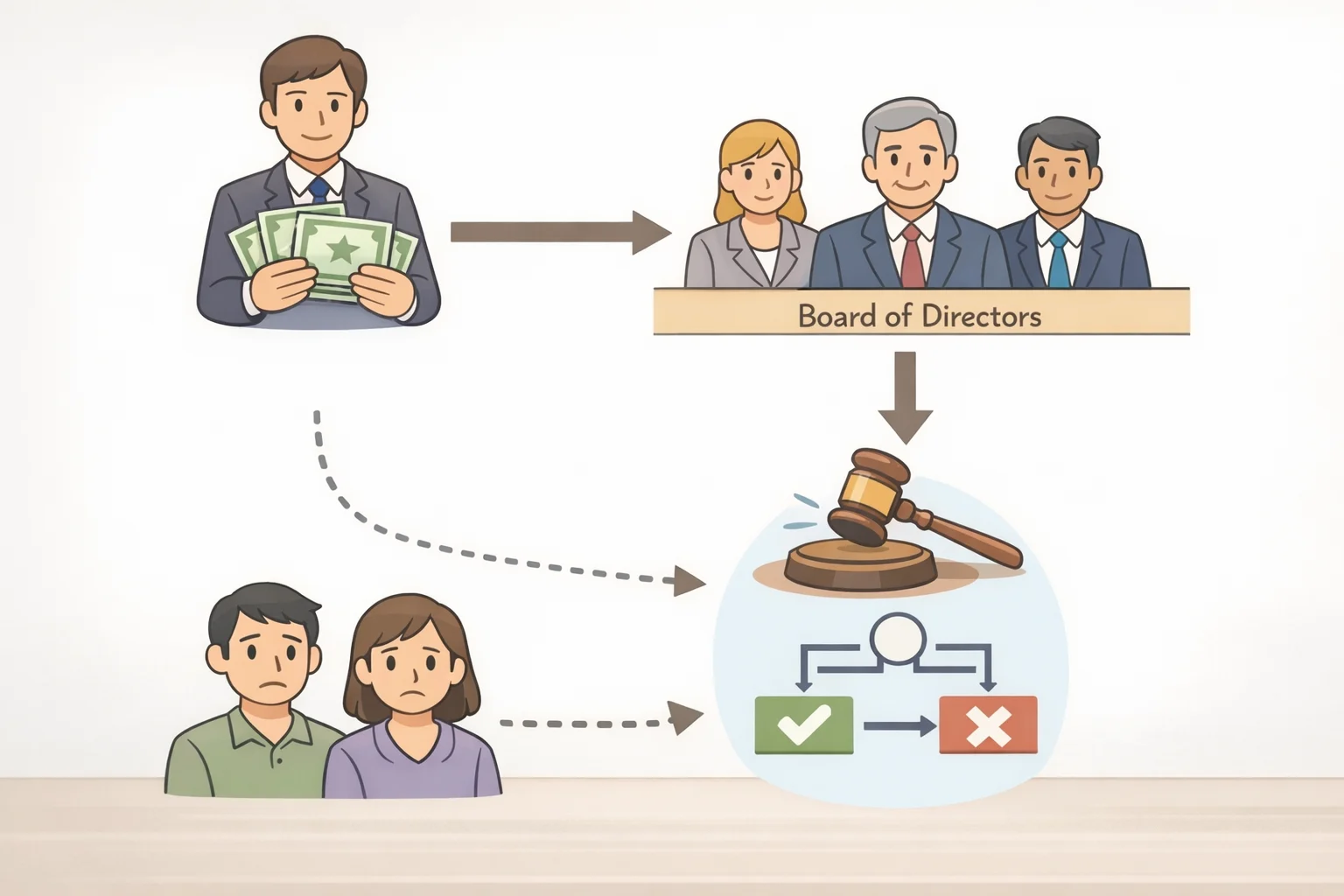

The price is only half the story. The governance structure is the other half, and it is not especially comforting.

Morningstar says Elon Musk is expected to retain roughly 85% voting control through a dual-class share structure. Public shareholders will have severely limited ability to influence board composition, executive compensation, capital allocation, or strategic decisions. That is not unusual in founder-led tech firms. It is just more consequential when the valuation is already stretched.

The Harvard Law School Corporate Governance Forum was blunter. It wrote this week that SpaceX is planning to go public in mid-June with a governance structure that frees Musk from constraints on his power. The forum says the charter, filed under Texas law, would let Musk take for himself business opportunities first presented to SpaceX, and would also permit related-party transactions that could benefit him at public investors’ expense.

That is not a minor footnote. It means the same person who controls strategy also has unusual freedom to decide how the pie gets split.

Harvard also points to succession risk. If Musk were incapacitated or died, voting control would pass to heirs or trust managers, but the prospectus does not identify who those people are. Investors do not like uncertainty, though they usually tolerate it more cheerfully when the stock is cheap.

There is also a practical concern about attention. Harvard notes that at Tesla, Musk was not required to limit outside activities or commit a specific amount of time to the company, and that he spent substantial time away during the Twitter acquisition period. The SpaceX structure does not impose a meaningful time commitment either, even as it locks him in as CEO and chair.

At a cheaper price, those governance quirks would be easier to shrug off. At $135 a share, they matter more because there is less cushion if the story goes wrong.

How to invest in SpaceX IPO stock if you cannot buy it directly yet

A lot of retail money is already trying to get in before the shares list. Morningstar said this month that there is a frenzy among investors seeking SpaceX exposure before it goes public. Four funds, Baron Partners, Baron First Principles ETF, ERShares Private-Public Crossover ETF, and Tema Space Innovators ETF, took in a combined $7.9 billion in May alone.

That route has a catch. When fresh money pours into a fund that already owns a private stake, the SpaceX position can shrink as a percentage of the portfolio even if the dollar value stays the same. Morningstar gives a simple example: a fund with a $200 million SpaceX stake equal to 10% of assets would see that weight fall to 7.5% if it took in $500 million of new cash.

Baron Partners is the clearest case. Morningstar said the fund entered May with about 31.7% of assets in SpaceX and then took in roughly $3.8 billion more during the month. That almost certainly diluted the exposure, even if the headline says otherwise.

The other issue is that these products are not pure SpaceX plays. Morningstar notes that the Tema Space Innovators ETF also owns Rocket Lab, Planet Labs, Intuitive Machines, and around three dozen other names tied to the emerging space economy. It adds diversification, sure. It also adds a lot of other risk and a healthy dose of valuation froth.

ERShares is no magic shortcut either. Morningstar says its underlying basket has underperformed the Russell 1000 Growth Index by more than seven percentage points annually since inception. So if the idea is to buy a fund just to get a quasi-early shot at SpaceX, the wrapper deserves scrutiny too.

Once SpaceX begins trading, the math changes. Morningstar says anyone who wants the stock can buy it on the open market. That removes the need to pay through a fund that also bundles in other holdings you may not want.

What patient investors should watch after the IPO

The first trading day will be dramatic and probably not very useful. Investing.com put it neatly last month, the first trading day will get attention, but it will not answer the real question.

What matters instead is execution. Morningstar expects Starlink to remain the main cash engine in the near term and projects operating profits will exceed $5 billion in 2026. It also estimates Starlink could generate $24 billion in revenue by 2035. That is the stable piece of the story.

The rest is the harder part. Investors should watch Starlink subscriber growth, ARPU, launch cadence, Starship milestones, AI segment losses, capital expenditures, government contract renewals, related-party disclosures, and insider selling after lock-up periods, as Investing.com put it last month. Morningstar also expects selling pressure to build in the months after the IPO, as successive tranches of stock held by private investors and employees become eligible for sale during 2026 and 2027.

That is the part public buyers should care about. If Starship advances faster than expected, if the AI ambitions start looking less speculative, and if the post-IPO selling pressure is absorbed without damage, the stock can justify more. If not, the opening price will look less like a launch and more like a long way down.

For now, the clean answer to should you buy SpaceX IPO stock is no, not at the opening price unless you are unusually confident in the moonshot case and unusually comfortable with weak minority protections. SpaceX is a real company with real strengths. The stock, at least as described in the reporting available now, asks investors to pay for a future that is still under construction.