SpaceX lockup period for investors: timing and supply

SpaceX’s lockup period is not the usual IPO waiting room. For public investors, the practical question is simple: when can SpaceX shareholders sell, and how much stock could hit the market at each step? The answer is a tiered schedule with several release windows, not a single 180-day door.

That matters because most IPOs use one blunt restriction. Insiders generally cannot sell for 90 to 180 days after listing, The Motley Fool reported this week. SpaceX built something more complicated, with multiple gates tied to earnings dates, calendar milestones, and stock performance, a setup the company says is meant to reduce volatility.

The other number that matters is the one not spelled out clearly in public summaries. The prospectus refers to a pool of “Early Release Eligible Shares,” but the total size of that pool is not clearly disclosed in the material at hand. Without that figure, no one can do more than guess at the eventual selling pressure.

How the SpaceX lockup period works

A lockup period is a contractual limit that keeps insiders and early investors from selling immediately after an IPO. The point is to stop a flood of stock from hitting the market on day one. Think of it as a release valve, not a wall.

SpaceX’s version is unusual because it uses several release valves instead of one. CNBC reported last month that the company created a series of windows that open in stages after the IPO.

Here is the basic schedule, according to the prospectus summarized in the research:

- On the second full trading day after SpaceX reports second-quarter results, early investors may sell up to 20% of their eligible locked-up shares.

- If the stock trades at least 30% above the IPO price for at least five of the 10 trading days after that earnings report, they may sell an additional 10% on or after the second full trading day after that date.

- On or after days 70, 90, 105, 120, and 135 after the IPO, another 7% of eligible shares may be transferred at each step.

- On the second full trading day after third-quarter results, investors may sell 28% more.

- After 180 days, whatever remains is fully released. The Motley Fool outlined the same structure this week.

The result is not hard to understand, just easier to overstate. Shares do not suddenly pour out at one moment. They dribble out in chunks, and some of those chunks depend on how the stock performs.

There is also a longer lockup for the biggest holders. Elon Musk and certain other large investors are subject to a 366-day restriction, according to Cape Fear Advisors, which said this last month. The founder is excluded from the early-release provisions available to other early investors during that extended period.

That distinction matters. The schedule governs when various holders can sell, but it does not say how much stock is actually in each bucket. The public filings cited in the research do not clearly identify the full list of holders covered by the early-release terms, either.

Why the timing matters

The lockup schedule would be interesting on its own. It becomes more interesting when placed next to Nasdaq’s index rules.

As of May, Nasdaq’s fast-entry rules allowed large enough new listings to qualify for Nasdaq 100 inclusion about 15 trading days after the IPO, Cape Fear Advisors reported last month. For a June 12 IPO, that would put the seasoning period into early July and the next quarterly Nasdaq 100 rebalance into mid-July.

That matters because inclusion in the index forces passive funds to buy. Index-tracking vehicles have to match the benchmark, and that means buying SpaceX shares whether they like the valuation or not. Cape Fear Advisors said independent analysts estimated that forced buying could reach roughly $30 billion concentrated into the days immediately after inclusion.

There is a catch, and it is a sensible one. Nasdaq gives newly listed companies lower weight until more shares are available for trading, CNBC reported last month. SpaceX’s float is likely to be small at first because so much stock is locked up. That means the passive buying should be real, but not infinite.

The timing still lines up neatly. Cape Fear Advisors said the first major earnings-based release arrives about a month after Nasdaq 100 fast-entry inclusion would occur. So the first meaningful insider selling window opens after a stretch when passive demand may still be unusually heavy.

Whether that was planned is another matter. The disclosures support a structural overlap, not a clean statement of intent. Still, the sequence is hard to miss.

What the SpaceX lockup period means for the stock

For early trading, the main effect is supply management. Limited float can support a tight market, but it also makes prices jumpy because there are fewer shares available to absorb orders.

That is the part most investors will watch first. The second-quarter earnings date is the first meaningful release trigger, and it will be the first test of how much stock actually becomes available. If the shares are trading more than 30% above the IPO price for the required stretch, the extra 10% release kicks in too.

The bigger point is that the lockup does not stand alone. It interacts with index demand, a thin float, and a stock price that may already be carrying a lot of expectation before insiders are allowed to sell in size. That is a lot of moving pieces for one ticker.

Control does not move with the lockup

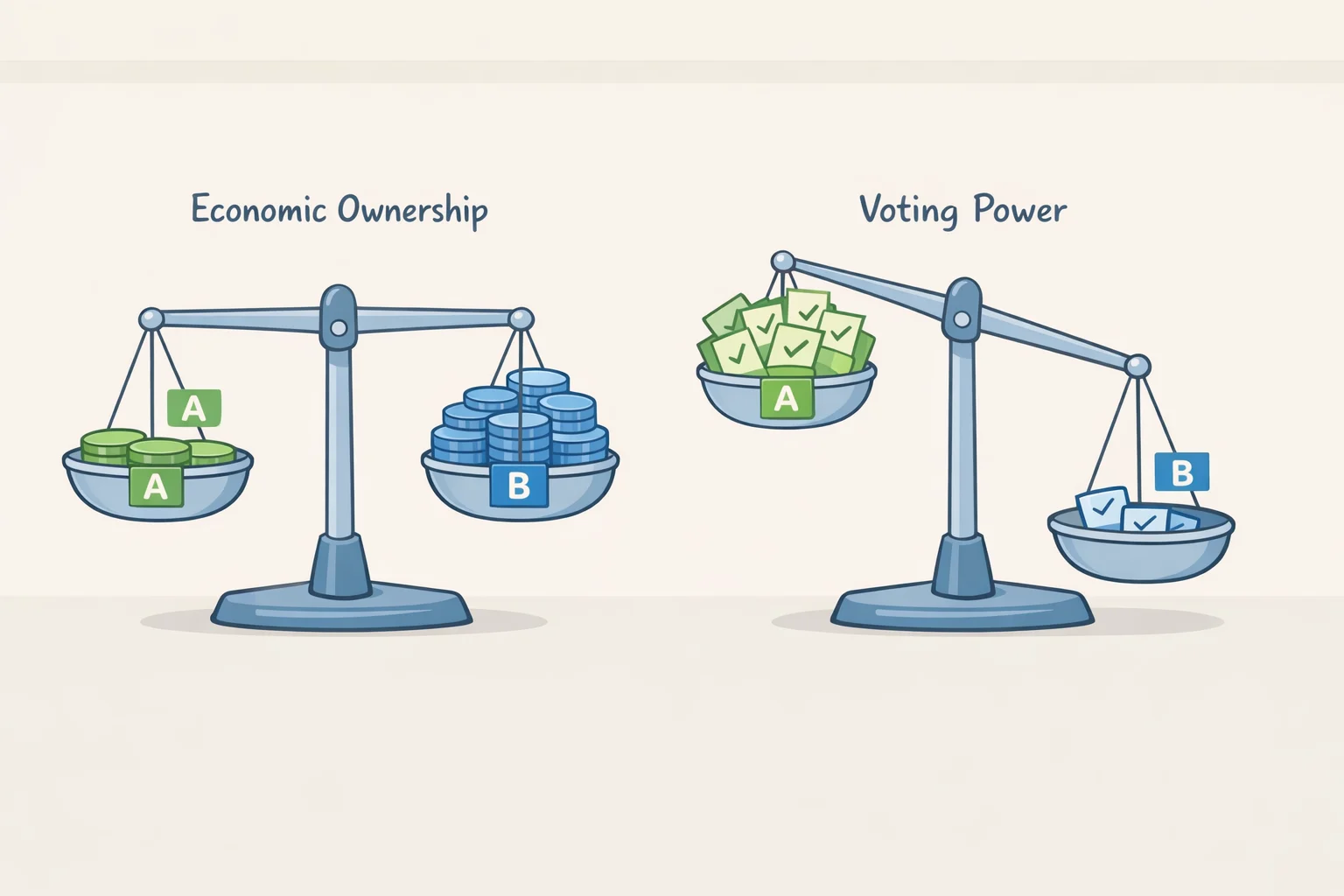

The selling rules are only half the story. The other half is governance, and SpaceX’s structure gives public shareholders far less control than their economic stake might suggest.

SpaceX will sell Class A shares to the public, each with one vote, while Musk’s Class B shares carry 10 votes each, Cape Fear Advisors said last month. Public shareholders are expected to hold about 60% of the company’s economic interest but only around 15% of combined voting power.

That is the basic imbalance. They own most of the economics and very little of the direction.

The structure also tends to reinforce itself over time. Harvard Law School Forum on Corporate Governance argued last month that when non-Musk holders of Class B shares sell, those shares convert into low-vote Class A shares. New Class B shares can be issued only to Musk and Musk-related entities. The practical effect is that Musk’s voting power can become even more concentrated as other holders cash out.

Harvard’s analysis goes further. It modeled a scenario in which Musk could theoretically keep absolute voting control while holding as little as roughly 9.1% of total equity, Harvard Law School Forum on Corporate Governance said last month. That was presented as a structural possibility, not a plan.

The broader governance picture is straightforward enough. The lockup controls when shares can be sold. The share classes control who really runs the company, even after sales begin.

The limits on shareholder pushback

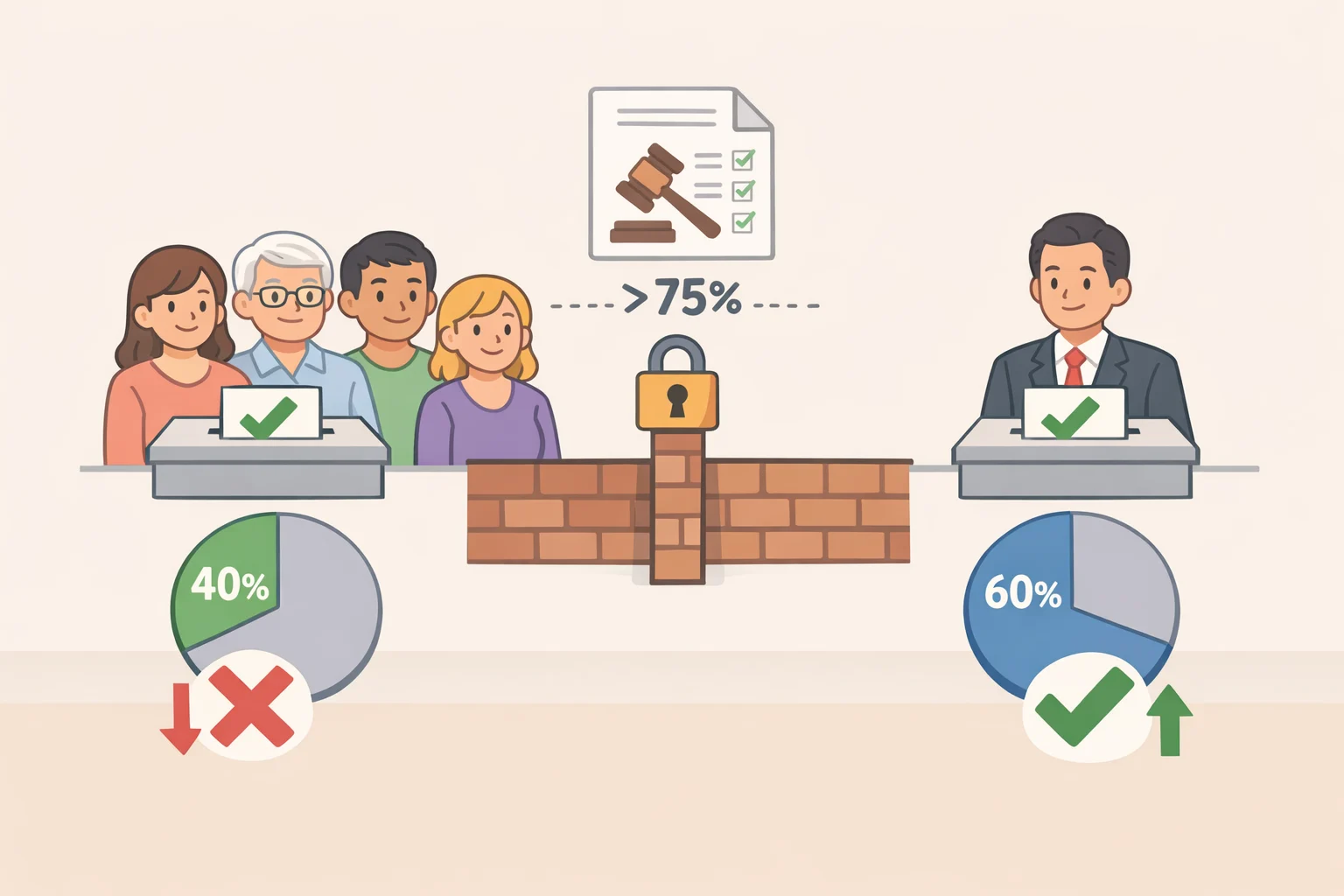

Public investors should also be realistic about how much they can do if they object to how SpaceX is run.

Cape Fear Advisors said last month that public shareholders will not have enough voting power to meet Texas’s shareholder-proposal threshold without controller cooperation. The rule requires holders to solicit at least 67% of voting power, which is far beyond the roughly 15% public shareholders are expected to have collectively.

The legal machinery is narrow, too. SpaceX’s bylaws route internal disputes to the Texas Business Court, a venue established by the Texas Legislature in 2024, Cape Fear Advisors reported last month. The bylaws also prohibit class actions, mass actions, and collective actions, and require disputes to be brought individually. Anyone who buys shares is deemed to have notice of, and consented to, those provisions.

The jury-trial waiver is part of that same package. Cape Fear Advisors quoted the filing language last month saying that anyone acquiring shares is deemed to have “irrevocably and unconditionally waived” any right to a jury trial in an internal dispute. That is the exact point investors should take away. It is not a side note.

The result is a company where public ownership means exposure to the economics, not much use over the governance.

What investors should watch next

The next few weeks matter more than the calendar alone. The first thing to watch is the second-quarter earnings release, because that is the first major point at which early investors may sell. The second is whether the stock meets the 30% price condition for the extra 10% tranche. The third is the Nasdaq 100 inclusion process in early to mid-July, Cape Fear Advisors said last month.

The unknown share pool remains the big gap. Without a clear count of Early Release Eligible Shares, investors cannot judge how much supply might arrive at each stage, only when the gates open. That is the number to look for in the full S-1, not the headlines.

For anyone thinking about SpaceX stock, the lesson is not complicated. The lockup period is staged, the selling windows are tied to both time and performance, and the governance structure gives Musk exceptional staying power regardless of how much equity changes hands. The real test for public investors will be how much stock comes loose, and how much control never does.