- How to Protect Your Savings From Inflation With I Bonds

- Where to keep money during inflation

- Step 1: Check whether I bonds fit your money

- Step 2: Understand how I bond returns work

- Step 3: Work out the tax tradeoff before you buy

- Step 4: Size the allocation without pretending I bonds solve everything

- Step 5: Buy only after you confirm the terms

- Conclusion

How to Protect Your Savings From Inflation With I Bonds

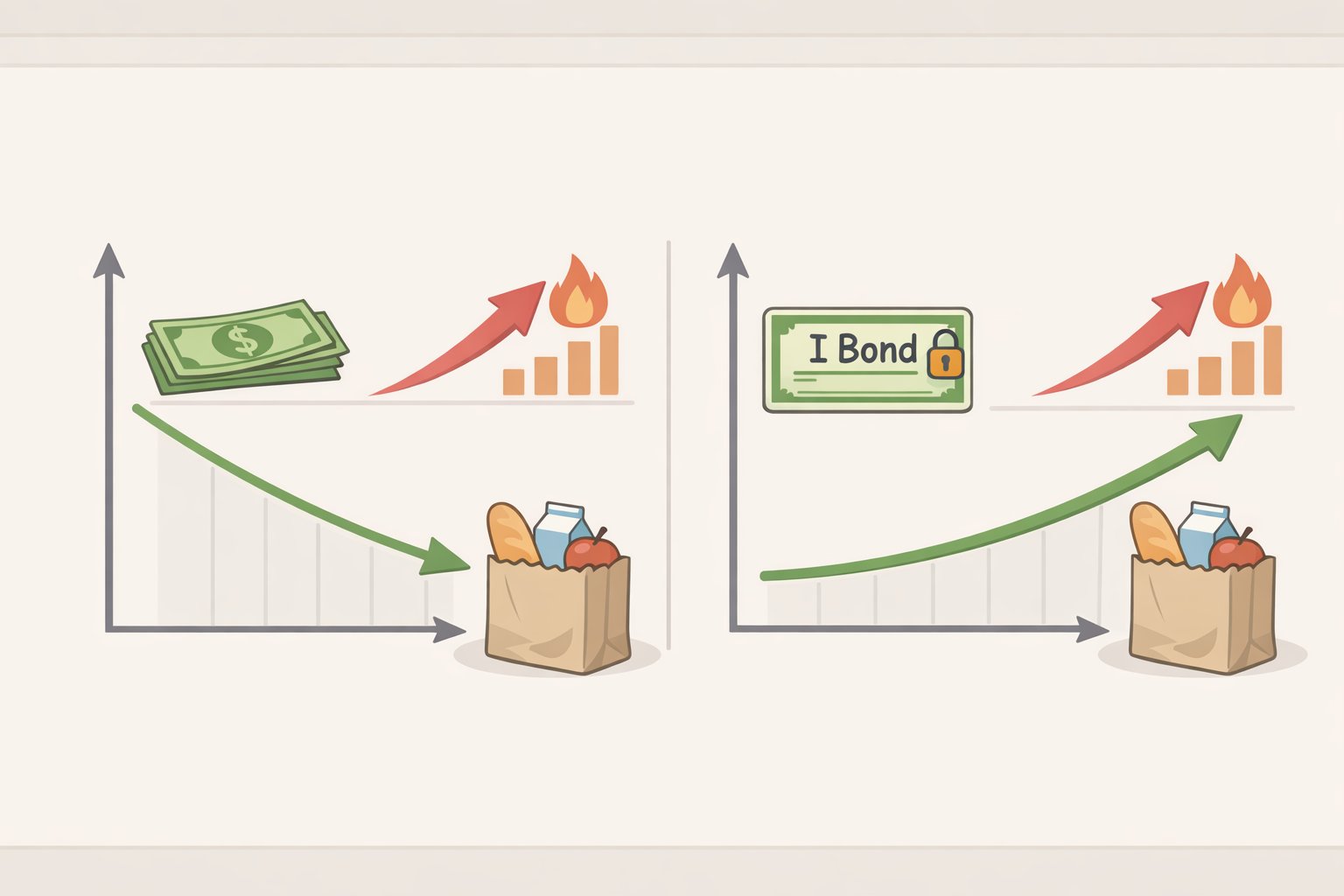

Series I savings bonds are one of the few places where cash can keep pace with inflation without giving up principal protection. They are not a magic shield, and they are not a home for money you might need next month. They are for cash you can leave alone for at least a year, after your emergency fund and after any high-interest debt is gone.

That is the decision in front of the reader: whether some portion of idle savings belongs in I bonds, or whether it should stay liquid elsewhere. The answer depends on how long the money can sit, how much you can buy, and whether the tax treatment helps or hinders your return.

Where to keep money during inflation

Inflation was still the most common financial worry for U.S. adults at the end of 2024, with 37% of households naming inflation and prices as a concern, ahead of basic living expenses at 22% and housing at 13%, according to the Federal Reserve's 2025 household well-being report. The report also found that people with income under $100,000 were more likely to specifically mention the cost of food and groceries as a concern.

The backdrop matters because the savings cushion many households built during the pandemic is gone. The Fed said U.S. excess savings were depleted in 2023Q1, while households in other advanced economies still held buffers of about 3% to 5% of GDP (Federal Reserve FEDS Notes, June 2023). Cash that sits in a plain account and earns less than inflation does what math says it will do, which is quietly lose purchasing power.

That is where I bonds come in. They do one job reasonably well: they help protect savings against inflation for money you do not need to touch right away.

Step 1: Check whether I bonds fit your money

Start with liquidity. I bonds cannot be redeemed for the first 12 months after purchase, so they are not a substitute for an emergency fund. If the money may be needed within a year, keep it out of I bonds.

Then think about debt. If you are carrying high-interest credit card debt or something similar, paying that down is usually the cleaner move. It offers a guaranteed return that no savings product is likely to beat.

The other limit is size. TreasuryDirect says there are annual purchase limits on electronic I bonds, so only a slice of cash savings can go into them in any one year (TreasuryDirect.gov). That makes I bonds a partial fix, not a full one.

A useful rule of thumb: I bonds fit readers who already have a funded emergency reserve, no high-interest debt, and cash they can leave untouched for at least 12 months. If the money may need to last five years, all the better. If it might be needed sooner, look somewhere else.

Step 2: Understand how I bond returns work

The mechanics are simple once the jargon is stripped out. TreasuryDirect says the earnings rate, or composite rate, is made up of two parts, a fixed rate and an inflation rate, and the inflation rate can change every six months from the bond’s issue date (TreasuryDirect).

The fixed rate stays the same for the life of the bond. The inflation rate moves with changes in the Consumer Price Index for urban consumers, or CPI-U. When inflation rises, the bond’s earnings rate rises too. When inflation falls, the rate falls, but the redemption value does not go down (TreasuryDirect).

That floor is the point. TreasuryDirect says a Series I bond’s redemption value will not decline during periods of deflation (TreasuryDirect). So while a savings account can preserve the dollar balance in front of you, an I bond tries to preserve that balance in real terms as well.

Interest starts in the first month you own the bond (TreasuryDirect). It is not paid out monthly. It accumulates until you cash out, which is a small annoyance and a useful discipline at the same time.

One thing Treasury is blunt about: you cannot determine the future value of a Series I bond in future years (TreasuryDirect). That uncertainty is built into the structure. You know the principal will not be cut. You do not know the exact payoff.

Step 3: Work out the tax tradeoff before you buy

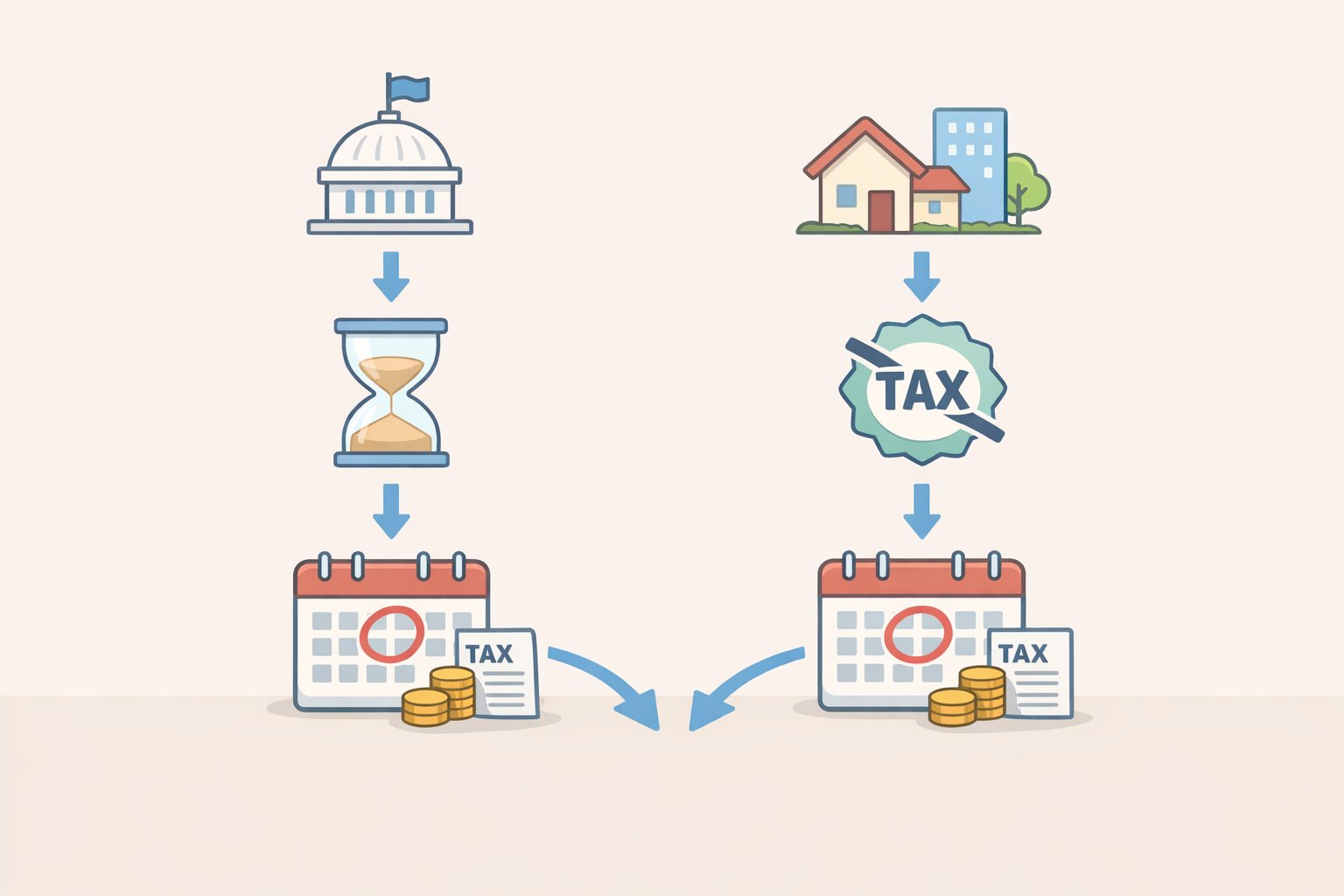

The tax treatment is part of the return, not an afterthought. TreasuryDirect says I bond interest is subject to federal income tax but not state or local income tax (TreasuryDirect). For savers in high-tax states, that exemption can make a noticeable difference.

Federal tax is usually deferred until the bond is cashed in or matures. TreasuryDirect says most people postpone reporting the interest until they actually receive it (TreasuryDirect). That means the interest compounds without an annual federal tax bill chipping away at the balance.

When the bond is redeemed, the 1099-INT covers the interest the bond earned over its life (TreasuryDirect). That can make the tax bill lumpy if the bond has been sitting there for years. It is worth planning for the year you redeem, especially if you expect a bigger income year to land in the same tax return.

There is also an education wrinkle. TreasuryDirect says using the money for higher education may keep you from paying federal income tax on the bond interest, subject to the rules that apply (TreasuryDirect). If the bond is part of a college fund, the exemption is worth checking before assuming the plain-vanilla tax treatment applies.

Step 4: Size the allocation without pretending I bonds solve everything

This is the part people often skip, then regret later. Because annual purchase limits cap how much can go into I bonds, they should be treated as one piece of a cash plan, not the whole thing.

Start with the money you truly do not need for at least 12 months. From there, decide how much of that pool belongs in I bonds and how much should remain liquid. If the amount exceeds the annual purchase limit, the remainder needs its own home.

That remaining cash does not have to sit idle. Readers should compare current yields and terms on high-yield savings accounts, short-term CDs, Treasury bills, and TIPS at TreasuryDirect.gov and through their bank or brokerage. The useful comparison is not just the headline yield. It is liquidity, tax treatment, inflation linkage, and what happens when you need the money sooner than planned.

The Fed’s savings data are a national average, which means they do not tell the whole story for every household (Federal Reserve FEDS Notes, June 2023). A family with a fat cash balance has a different problem from a renter living month to month. Size the I bond allocation to the money you can genuinely park, not to the amount that looks tidy on paper.

Step 5: Buy only after you confirm the terms

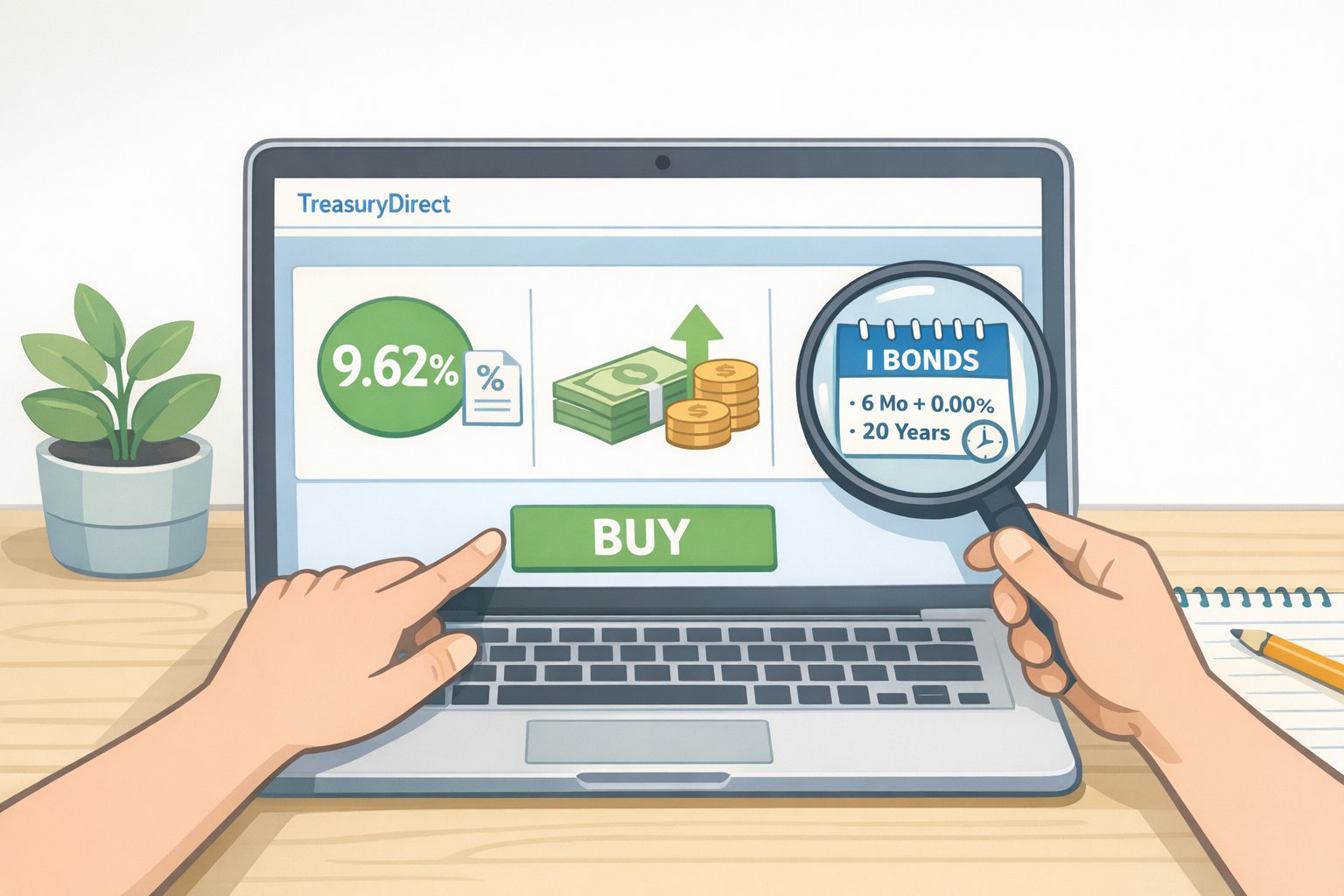

TreasuryDirect says a free TreasuryDirect account is used to buy savings bonds, and the site is where the current rules live (TreasuryDirect.gov). That matters because I bond terms can change, and old source materials will not tell you what applies today.

Before buying, check the current composite rate, the purchase limits, and any other current TreasuryDirect rules. Then decide whether the bond still fits the job. A product that once looked perfect can become just another modest option once the rate changes or the lockup feels longer than it did on paper.

That is not a flaw. It is the nature of cash management. The right place for savings during inflation is not the same for everyone, and it is rarely one place only.

Conclusion

If the goal is to protect savings against inflation, I bonds do a narrow but useful job. They give you a principal floor, an inflation-linked rate that resets every six months, and tax treatment that may help depending on where you live and when you redeem (TreasuryDirect; TreasuryDirect). They also come with a 12-month lockup and purchase limits, which keeps them from becoming a universal answer.

The next move is simple. Confirm the money is truly long-term, compare I bonds with the other places cash can sit, and buy only the amount that fits inside those constraints. The rest of your savings deserves a separate decision, because inflation does not pause just because the paperwork is annoying.