- Merrick Bank review: CD terms explained for 2026

- Who Merrick Bank deposit accounts are for

- Merrick Bank CD rates and account structure

- Early withdrawal penalties and the grace period

- Fees and consumer protections in the fine print

- What this Merrick Bank review can and cannot say

- Is Merrick Bank worth a look?

Merrick Bank review: CD terms explained for 2026

Merrick Bank review searches usually start with rate shopping, but the first thing this one needs to do is narrow the field. Merrick’s certificates of deposit are built for a very specific saver: someone with $25,000 ready to leave on deposit, comfortable managing the account online, and willing to let the money sit until maturity.

That matters because the contract is not casual about the setup. Every account owner must enroll in Merrick Bank’s online banking system for deposit accounts, Banno, and losing access to Banno does not release the customer from the account terms, according to the Merrick Bank Time Deposit Account Contract (May 2025). Funding is ACH-only, and Merrick does not accept cash, checks, or wire transfers to open the account, so anyone applying needs a separate U.S. bank account already in place.

Who Merrick Bank deposit accounts are for

This is not a broad-appeal CD. The contract requires applicants to apply from within the U.S. using a U.S.-based IP address, be at least 18, be a permanent U.S. resident, have a Social Security Number, have a U.S. street address, and be enrolled in Banno, per the Merrick Bank Time Deposit Account Contract (May 2025). If any of those boxes are missing, the door stays shut.

Think of Banno less like a helpful feature and more like the lobby. It is the only entrance. Customer service is available by phone Monday through Friday, except holidays, from 8:00 a.m. to 6:00 p.m. CST, but day-to-day account access lives online.

There is one more wrinkle worth noticing. In verifying identity and eligibility, Merrick may review a consumer report, credit history, or other information, and the application authorizes that review, according to the same contract. The terms do not say whether that review is a hard inquiry or a soft one, so applicants who care about their credit file may want to ask before submitting anything.

Merrick Bank CD rates and account structure

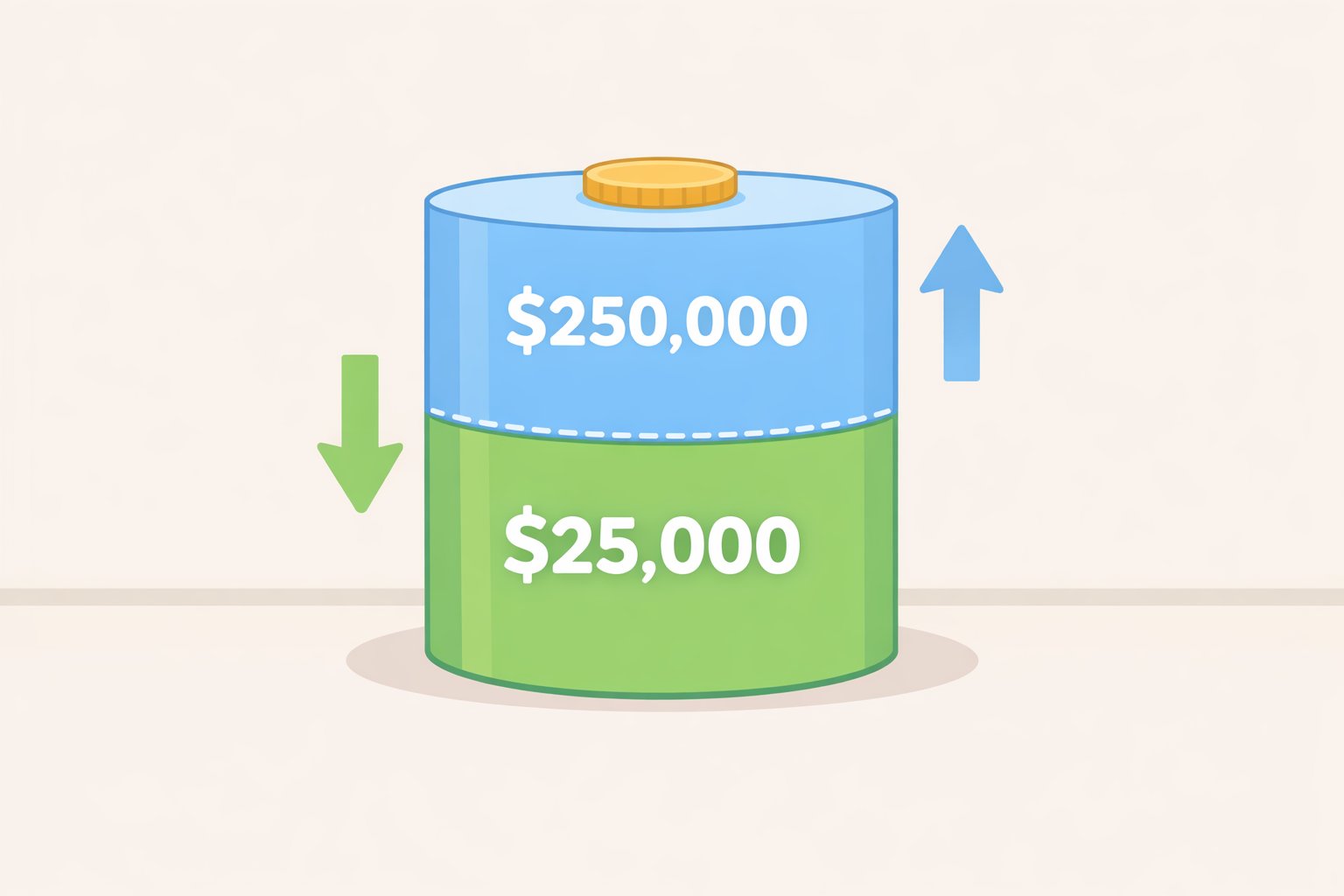

The biggest number in the contract is not an APY. It is the $25,000 minimum deposit. That is the amount required to open the account, and the account must keep a minimum principal balance of $25,000 each day to obtain the disclosed APY, while also compounding interest, according to the Merrick Bank Time Deposit Account Contract (May 2025).

That structure does two things at once. First, it makes the account unavailable to smaller CD shoppers, full stop. Second, it means the headline APY is tied to behavior, not just opening balance. A saver who wants interest paid out instead of compounded would not qualify for the disclosed APY under the contract.

There is also a ceiling. The maximum account balance is $250,000, and interest that accrues and is paid to the account does not count toward that limit, according to the contract. So the product is designed to hold a meaningful chunk of cash, but not to become a parking lot for unlimited funds.

This is why any discussion of Merrick Bank CD rates has to start with the structure, not the yield. Current APYs and term options were not provided in the research for this review, so they are not being guessed at here. Readers should check Merrick’s current posting directly if the live rate is the deciding factor. The terms do the real sorting first.

Early withdrawal penalties and the grace period

CDs are supposed to be boring. That is the whole appeal. Merrick’s contract makes the bargain plain: keep the money on deposit until maturity, or pay for the exit.

The early withdrawal penalty is tiered by term length. For terms of 364 days or less, the penalty is 90 days’ interest. For terms between 365 and 1,459 days, it is 180 days’ interest. For terms of 1,460 days or longer, it is 270 days’ interest, according to the Merrick Bank Time Deposit Account Contract (May 2025).

That is not unusual for a CD. It is just easier to ignore the penalty when the balance is small. On a $25,000 deposit, giving up half a year or more of interest can turn a decent yield into an expensive lesson. If there is even a fair chance the cash will be needed early, this is the wrong parking spot.

Merrick also uses automatic renewal. Unless the bank receives instructions not to renew, the account rolls into a new term at maturity, per the contract. The grace period is ten calendar days after the maturity date. Miss that window, and the money is locked into another term at whatever rate is current when the rollover happens.

That ten-day window is the part people forget. A CD can look tidy on day one and still become annoying on day 366 if the owner is traveling, busy, or simply not paying attention. The contract does not wait for a convenient week.

Fees and consumer protections in the fine print

The fee schedule is not especially dramatic, but it is worth reading because fees have a way of appearing exactly when nobody wants them. Merrick’s contract lists $25.00 per wire, $5.00 per statement, $5.00 per notice, $25.00 per stop payment, $25.00 per return, $25.00 per check, and $50.00 per filing, according to the Merrick Bank Time Deposit Account Contract (May 2025).

For a disciplined CD holder who uses online delivery and leaves the money alone, most of those charges should stay theoretical. Still, they are part of the account’s price tag, and hidden costs have a way of becoming very visible once a customer needs something outside the normal routine.

The contract also limits liability. Merrick says it is not liable for performing or failing to perform services under the account terms unless it has acted in bad faith or is otherwise required by law, according to the same contract. That is standard legal insulation for a deposit agreement, but standard does not mean trivial.

Disputes go to binding arbitration rather than court. If the customer starts arbitration, the customer pays one half of the filing fee or $125, whichever is less. If Merrick starts it, the bank pays all arbitration costs. The contract also says that the customer will not be responsible for arbitration fees beyond that cap or for fees that would have been incurred in court.

That arrangement is not a consumer fairy tale, but it is more restrained than some arbitration clauses that leave customers holding the entire bill. The fine print is still the fine print. It just is not written with a heavy fist.

What this Merrick Bank review can and cannot say

What can be said, based on the contract, is straightforward. Merrick Bank’s CD is built for a narrow group of depositors, and the rules are exacting. The account is online-only through Banno, requires a $25,000 minimum deposit, demands daily balance maintenance to earn the disclosed APY, and allows no cash, check, or wire funding at opening.

What cannot be said from the available research is just as important. This review does not have verified live APYs, term lengths, FDIC insurance confirmation, app-quality reporting, or customer-service performance data. It would be easy to paper over those gaps with cheerful language and call it a day. That would be lazy, and the contract deserves better.

So the cleanest reading is this: Merrick Bank may be a fit for a saver with a large cash balance, a stable timeline, and no need for branch access or flexible funding. It is not built for someone testing the waters with a smaller deposit. The minimum alone takes care of that.

Is Merrick Bank worth a look?

For the right person, yes. A saver with $25,000 or more, comfortable with online account management, and prepared to leave the money untouched until maturity can get a product that is plain about its rules and unsentimental about enforcement. There is something almost refreshing about that.

For everyone else, the answer is simpler. If the balance is below $25,000, if online access feels fragile, if there is any real chance the money will be needed early, or if a broader banking relationship matters more than a single CD, Merrick’s structure rules it out before rates even enter the conversation.

That is not a flaw so much as a filter. Merrick Bank’s CD is not trying to be all things to all savers. It is asking for a very specific deal, and it spells out the terms with almost stubborn clarity.