How to File an IRS Pandemic Penalty Refund Claim

If you’re trying to figure out how to file an IRS pandemic penalty refund claim, the short version is this: some taxpayers who paid penalties or interest tied to the COVID-19 disaster period may need to file a claim now to preserve their rights. The Taxpayer Advocate Service warned about the issue in May 2026, and the filing deadline most affected taxpayers need to watch is July 10, 2026.

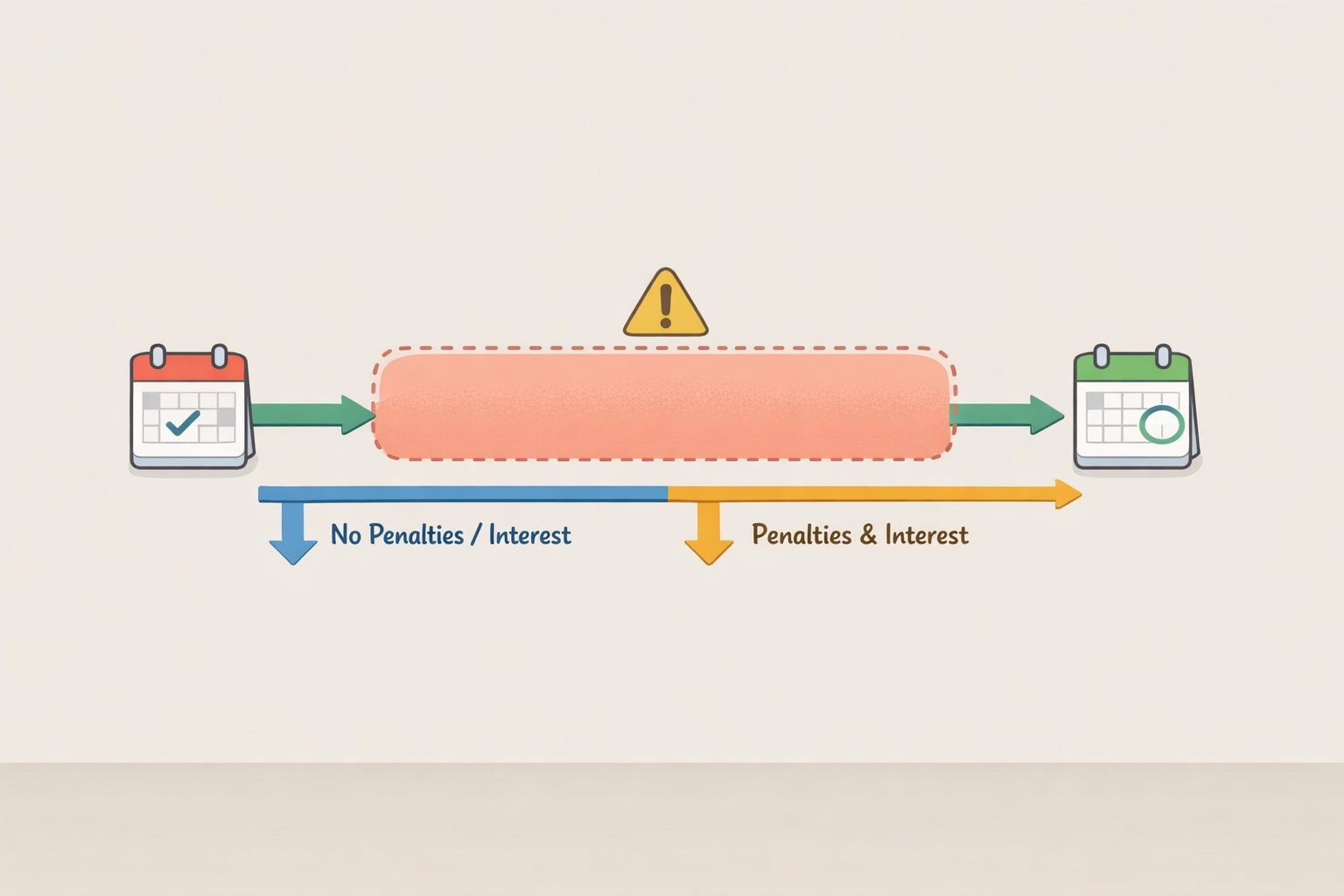

The legal theory behind the claims is Kwong v. United States. Under that reasoning, certain filing and payment deadlines may have been postponed during the COVID-19 federal disaster period, which ran from January 20, 2020 through May 11, 2023, plus 60 days, and that pushes the effective due date to July 10, 2023 for many returns and payments. That matters because the standard refund rule generally requires a claim to be filed by the later of three years from filing or two years from payment (Taxpayer Advocate Service NTA Blog, May 2026).

This is not settled law. The IRS has not formally accepted or rejected Kwong, so the point of filing is not to promise yourself a refund. It’s to preserve the claim while the courts sort out whether the penalties and interest were valid in the first place.

What the IRS pandemic penalty refund theory covers

Start with the scope, because that’s where people get tripped up. The Taxpayer Advocate Service says recent legal developments suggest some penalties and interest assessed during the nearly 3.5-year COVID-19 federal disaster period may have been improper, and tens of millions of taxpayers may be entitled to refunds or abatements if the theory prevails.

This is broader than the IRS’s automatic relief in 2022. That program covered certain failure-to-file penalties for 2019 and 2020 returns and was automatic, with no request required, but it did not extend to 2021 returns and did not cover every penalty or interest charge (IRS newsroom, September 2022; IRS Internal Revenue Bulletin 2022-36, September 2022). The Kwong theory is different. It depends on individual action.

How to tell whether this applies to you

Use this as a screening test, not a promise.

- Did you pay IRS penalties or interest, or have them assessed, on returns for 2019, 2020, 2021, or 2022?

- Did the return or payment fall somewhere in the COVID-19 federal disaster period?

- Do you think the amounts were assessed before July 10, 2023 under the Kwong theory?

If the answer to all three is yes, you may have a claim worth filing by July 10, 2026 (Taxpayer Advocate Service NTA Blog, May 2026). That said, the guidance does not say every penalty type is automatically covered. If your issue involves payroll taxes, trust filings, business returns, or estimated tax penalties, treat that as a caution flag, not a green light.

If you’re unsure what the IRS actually assessed, pull your IRS account transcript or check old notices such as CP2000 or CP14. That’s the paper trail you’ll need anyway.

There are also two other relief paths worth knowing if Kwong turns out not to fit your situation. First-Time Penalty Abatement may be available if you have a clean compliance history, and reasonable-cause relief can apply when facts beyond your control kept you from complying (Taxpayer Advocate Service, April 2022; TAS Tax Tips, May 2025). Those routes do not depend on Kwong.

File a protective claim on Form 843

Before you start, gather your IRS account transcripts, penalty notices, and payment records. You need enough detail to identify each tax year and each amount at issue. Otherwise the form becomes a very expensive piece of stationery.

Step 1: Decide whether you need a refund claim or an abatement request

A refund claim asks the IRS to return money you already paid (Taxpayer Advocate Service NTA Blog, May 2026). An abatement request asks the IRS to remove or reduce an assessed amount you have not yet paid.

That distinction matters because it changes the language you use on the form. If the amount is already paid, you’re asking for a refund. If it’s still sitting on the IRS books, you’re asking for abatement.

Step 2: Use Form 843

If you’re claiming Kwong-related refunds for interest and penalties and you are not revising the underlying tax liability, Form 843 is the form to use (Taxpayer Advocate Service NTA Blog, May 2026). You can find it here: Form 843, Claim for Refund and Request for Abatement.

Do not use Form 1040-X unless you are changing the tax itself. That is a different animal.

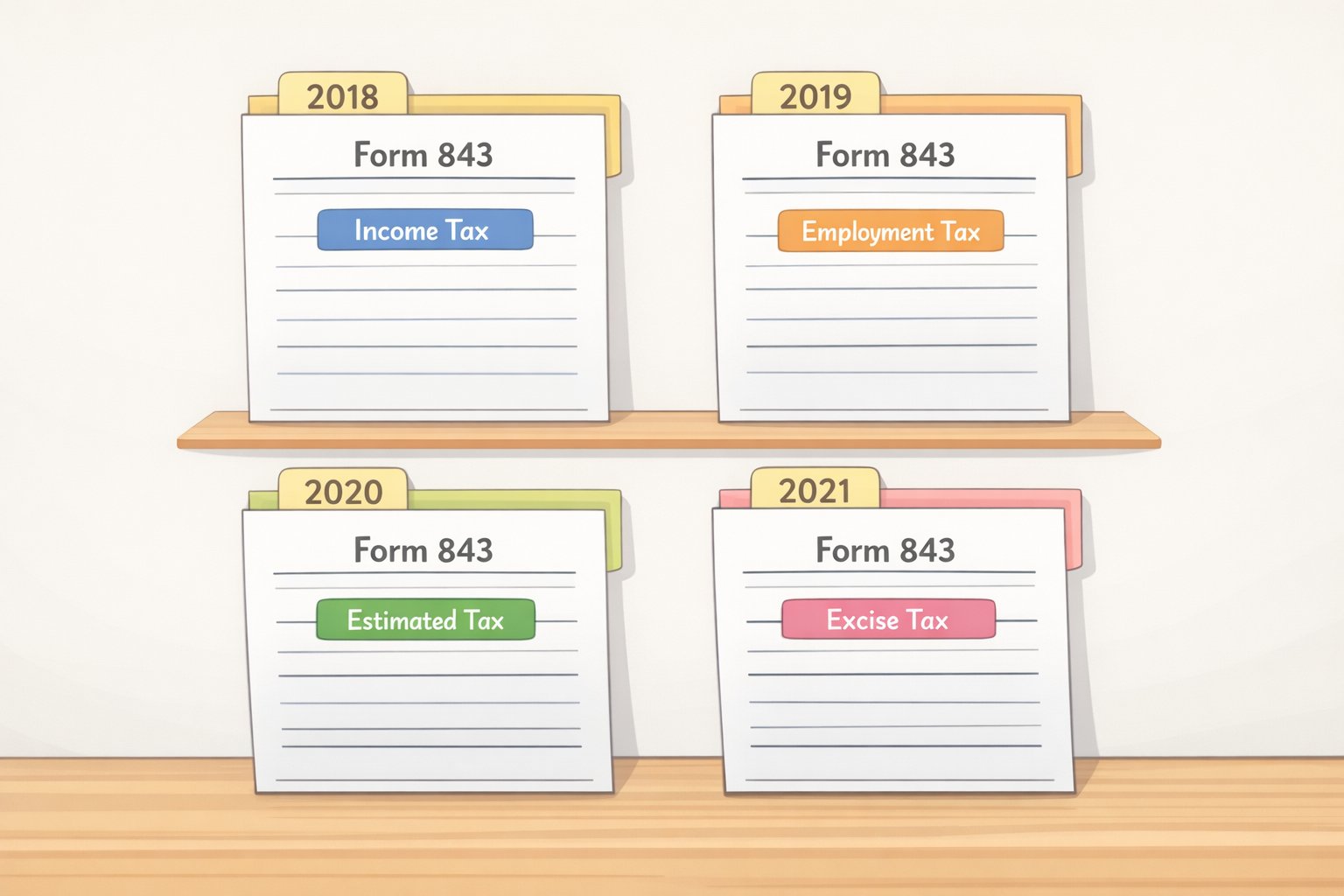

Step 3: Prepare a separate form for each tax period and tax type

In most cases, taxpayers must file a separate Form 843 for each tax period and each type of tax (Taxpayer Advocate Service NTA Blog, May 2026). If you have claims for 2019, 2020, 2021, and 2022, that can mean four separate forms.

Combining years or tax types on one form is one of the easiest ways to slow everything down.

Step 4: Fill in the form and make the claim specific

Complete your name, address, taxpayer identification number, tax year, and type of tax. Then write a clear explanation of the legal issue. A sentence like “I reserve my right to ask for a refund later” is not enough (Taxpayer Advocate Service NTA Blog, May 2026).

A usable explanation is plain and direct: this is a protective claim for penalties and interest tied to the COVID-19 disaster period, filed under the reasoning in Kwong v. United States, and the exact amount will be supplemented later once the legal issue is resolved. Keep it factual. Don’t write a novella.

The IRS’s internal procedures require a valid protective claim to be in writing, signed, and to identify the taxpayer, the specific years involved, the legal issue, and the basis for the claim (Taxpayer Advocate Service NTA Blog, May 2026).

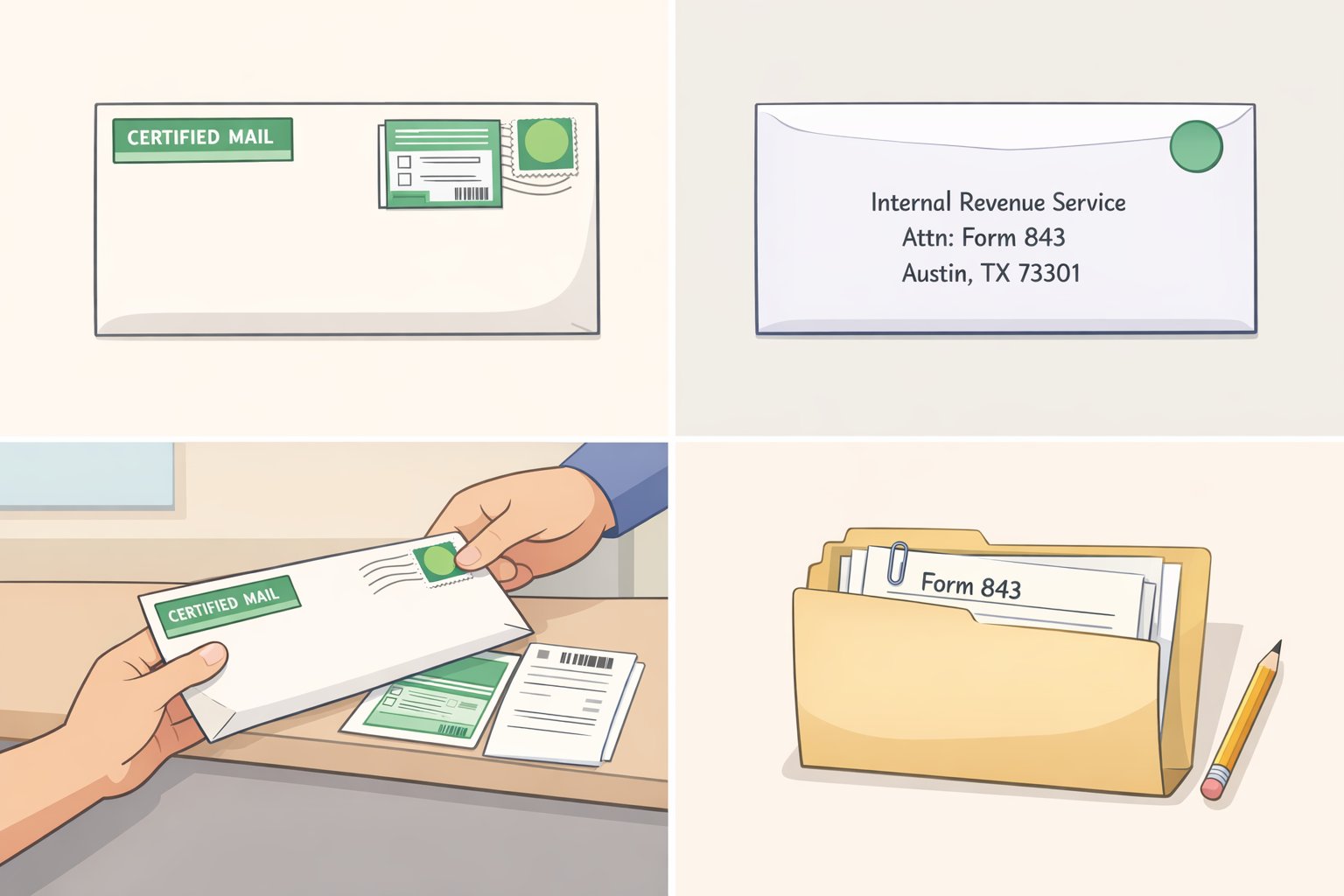

Step 5: Mail it to the right IRS service center

Send each Form 843 to the IRS service center where you would file a current-year return for that tax type (Taxpayer Advocate Service NTA Blog, May 2026). The address depends on your state and the kind of tax involved, so use the IRS.gov Where to File instructions.

Form 843 cannot be e-filed. It has to go by mail. Send it certified mail with return receipt, and keep a complete copy of everything you submit. The postmark is what proves you filed on time.

Mistakes that sink claims

The most common filing errors are easy enough to avoid, which is annoying because they are also the ones people make first. Missing the deadline, filing a vague claim, mailing without proof, sending it to the wrong address, or stuffing multiple years into one form can all derail the process (Taxpayer Advocate Service NTA Blog, May 2026).

The deadline deserves one last warning because the IRS and TAS both treat it seriously. A late filing risks losing the refund right altogether, even if the underlying legal theory eventually wins out. That is the unglamorous part of tax law: paper beats sympathy.

Watch the marketing, too. The Taxpayer Advocate Service warned in May 2026 that Kwong-related claims have already drawn aggressive refund schemes promising quick money and guaranteed eligibility. They can expose taxpayers to audits, repayment demands, penalties, and interest.

No legitimate tax professional can promise a sure thing here. The law is still unsettled. Anyone claiming otherwise is selling confidence, not advice.

What happens after you file

If the IRS does not allow or disallow the claim within six months, taxpayers generally have the right to file a lawsuit in federal court, including the U.S. Court of Federal Claims (Taxpayer Advocate Service NTA Blog, May 2026). If the claim is denied, you generally have 30 days from the rejection letter to request a hearing with the IRS Independent Office of Appeals (TAS Tax Tips, May 2025).

You can also supplement a protective claim later with more detail, but only if you filed it by the deadline. That is the whole logic of a protective claim. It buys time on the facts, not on the calendar.

Why filing now is the safer move

Filing a protective claim takes some paperwork and a stamp. Not filing can mean losing the refund right permanently, even if courts later side with taxpayers (Taxpayer Advocate Service NTA Blog, May 2026). For taxpayers with assessed but unpaid penalties, abatement requests follow different rules, but TAS still says not to sit on your hands.

If your case involves large amounts, multiple tax years, or business filings, a tax attorney or enrolled agent is worth considering. Free help is also available through the Taxpayer Advocate Service at taxpayeradvocate.irs.gov or 1-877-777-4778 for qualifying taxpayers.

File now if the claim might apply. The alternative is waiting for the law to catch up while the deadline walks out the door.