- What to do with a work bonus: Taxes, debt, and investing

- What to do first with a work bonus

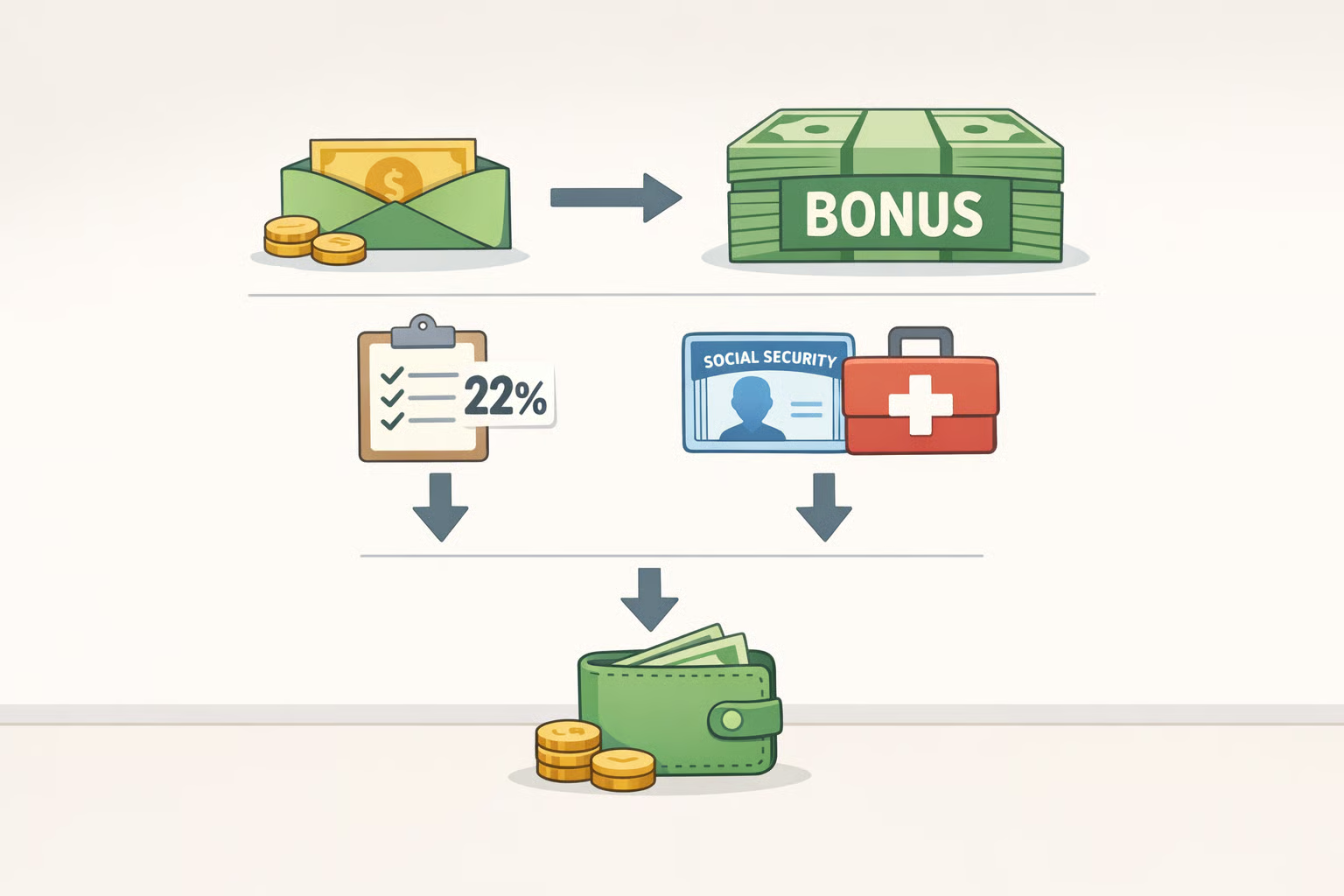

- Step 1: Calculate your real after-tax bonus

- Step 2: Pay off high-interest debt first

- Step 3: Build savings before you chase returns

- Step 4: Put the rest into long-term accounts

- How to use a work bonus wisely without turning it into a sermon

- A simple order of operations

- Conclusion: Give the bonus a job before it gives you ideas

What to do with a work bonus: Taxes, debt, and investing

What to do first with a work bonus

The gross number on your bonus notification is a fiction. Before you plan a single purchase or transfer, figure out what actually lands in your account, because that gap can be big enough to change the whole plan.

A work bonus is taxed as supplemental income. Most employers withhold federal income tax at a flat 22% under the percentage method for bonuses under $1 million, then Social Security and Medicare come off on top, with state tax potentially taking another bite. NerdWallet notes the IRS treats it like ordinary income when you file, so the withholding is only the opening move, not the final bill.

That matters because a year-end bonus is often the biggest windfall a worker sees all year, which is exactly why it disappears into impulse spending if nobody gives it a job. This guide walks through what to do with a work bonus in the right order: calculate the after-tax amount, pay down expensive debt, strengthen savings, invest what’s left, and leave a little room for a reward.

Step 1: Calculate your real after-tax bonus

Start with the number on the bonus notice, not the number in your head.

You need your gross bonus amount and, ideally, your pay stub so you can see whether payroll used the percentage method or the aggregate method. Under the percentage method, employers withhold 22% federally on most bonuses under $1 million. Under the aggregate method, the bonus is bundled with regular pay and taxed as one larger paycheck, which can push withholding higher than 22% depending on your situation. NerdWallet explains both approaches.

Then subtract payroll taxes. For 2026, the employee Social Security tax rate is 6.2% up to the IRS wage base of $184,500, and Medicare is 1.45% with no wage cap. That means federal withholding and payroll tax together can take a substantial chunk before state tax even enters the picture.

A simple estimate helps. If you got a $10,000 bonus and your employer used the 22% federal method, $2,200 is withheld for federal income tax before Social Security, Medicare, and any state tax are applied. The final tax owed may still be lower or higher when you file, because the bonus is added to your other earned income on your return. NerdWallet says that can produce a refund or a bill depending on your overall tax picture.

One small gotcha: if the withholding looks wildly off, do not assume payroll “messed up” in a way that can be fixed after the fact. It may simply mean your regular withholding is too light or too heavy for the year. NerdWallet notes that adjusting your W-4 before or after the bonus pays out is a straightforward way to bring withholding closer to reality. NerdWallet

Step 2: Pay off high-interest debt first

Once you know the net bonus, aim it at the most expensive debt sitting on your balance sheet.

Credit card debt is the obvious place to start. CNBC reported in late 2023 that the average credit card rate had climbed to 20.74%, and a balance of a little over $6,000 making only minimum payments would take 214 months to disappear and cost just over $9,000 in interest. CNBC cited Bankrate for those figures. That is a lot of money to pay for the privilege of being broke with style.

The case for debt repayment is simple. Paying down a 20%-plus balance is roughly the same as earning a guaranteed 20%-plus return, without the market risk and without waiting around for good news. If a bonus can erase that kind of interest bill, it has done real work.

NerdWallet’s November 2025 survey of 2,094 U.S. adults found that 30% would put the majority of a financial windfall toward debt repayment. NerdWallet The survey was conducted online by The Harris Poll from Nov. 3-5, 2025, and the result is not glamorous. It is still the sensible answer.

If several balances are competing for attention, pay the highest-rate debt first. If motivation matters more than strict math, knock out the smallest balance first and build momentum. Either way, do not let a “low monthly payment” fool you into thinking a debt is cheap.

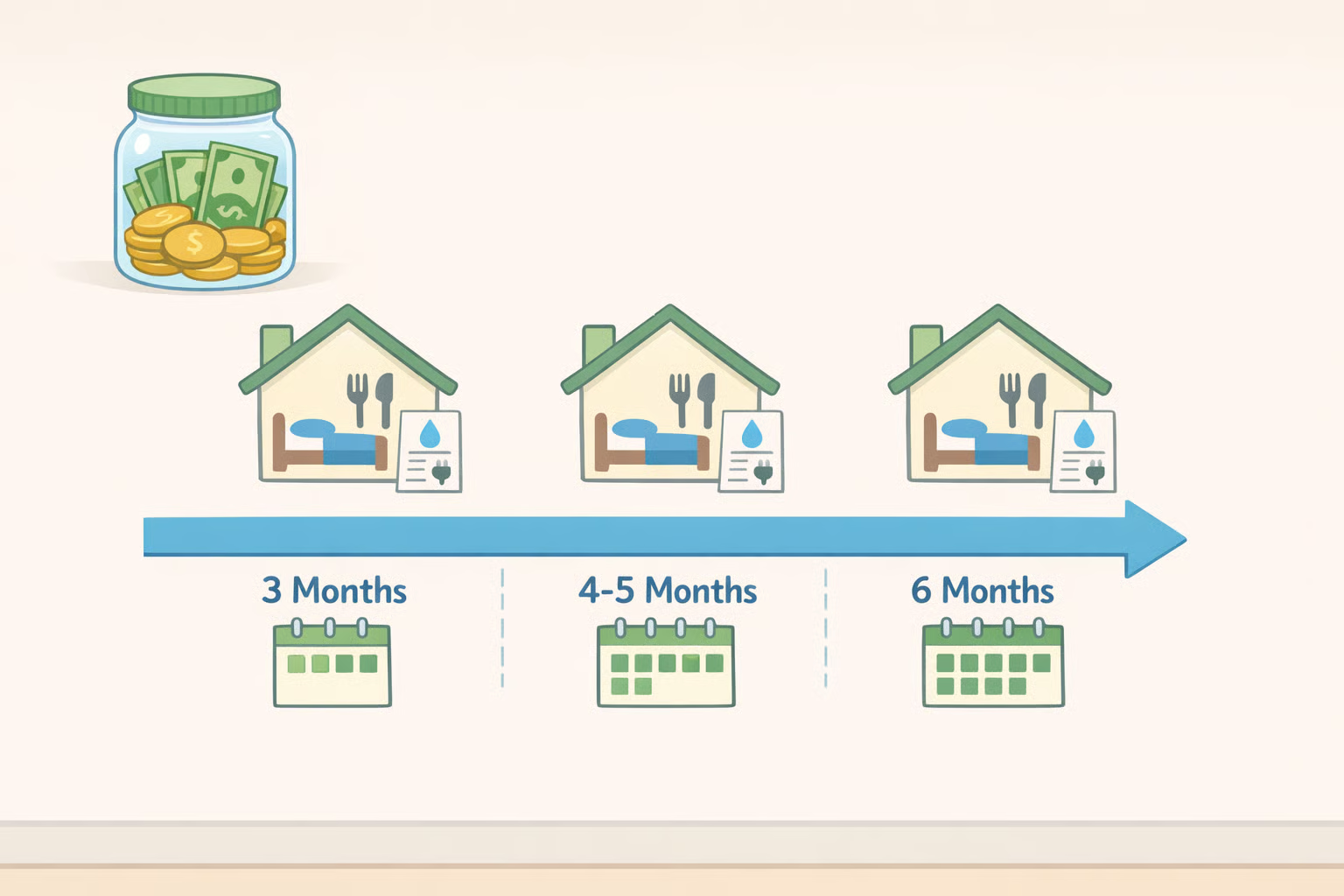

Step 3: Build savings before you chase returns

After expensive debt is under control, the next stop is cash reserves.

Financial planners usually point to three to six months of living expenses held in an account you can actually reach without a scavenger hunt. CNBC reported that range in 2023, and NerdWallet repeated the same rule of thumb in its 2025 windfall coverage. NerdWallet That cash is there for the annoying, ordinary disasters of life, the kind that do not make dramatic headlines but still cost money.

If your emergency fund is short, use the bonus to close the gap. A reserve that covers a few months of rent, groceries, utilities, transportation, and insurance buys something better than yield: breathing room. Markets cannot give that to you, no matter how charming the pitch deck.

NerdWallet’s survey found that 28% of Americans would put the majority of a windfall into savings. NerdWallet That is not a flashy answer, but savings has a useful habit of becoming extremely important the moment life gets inconvenient.

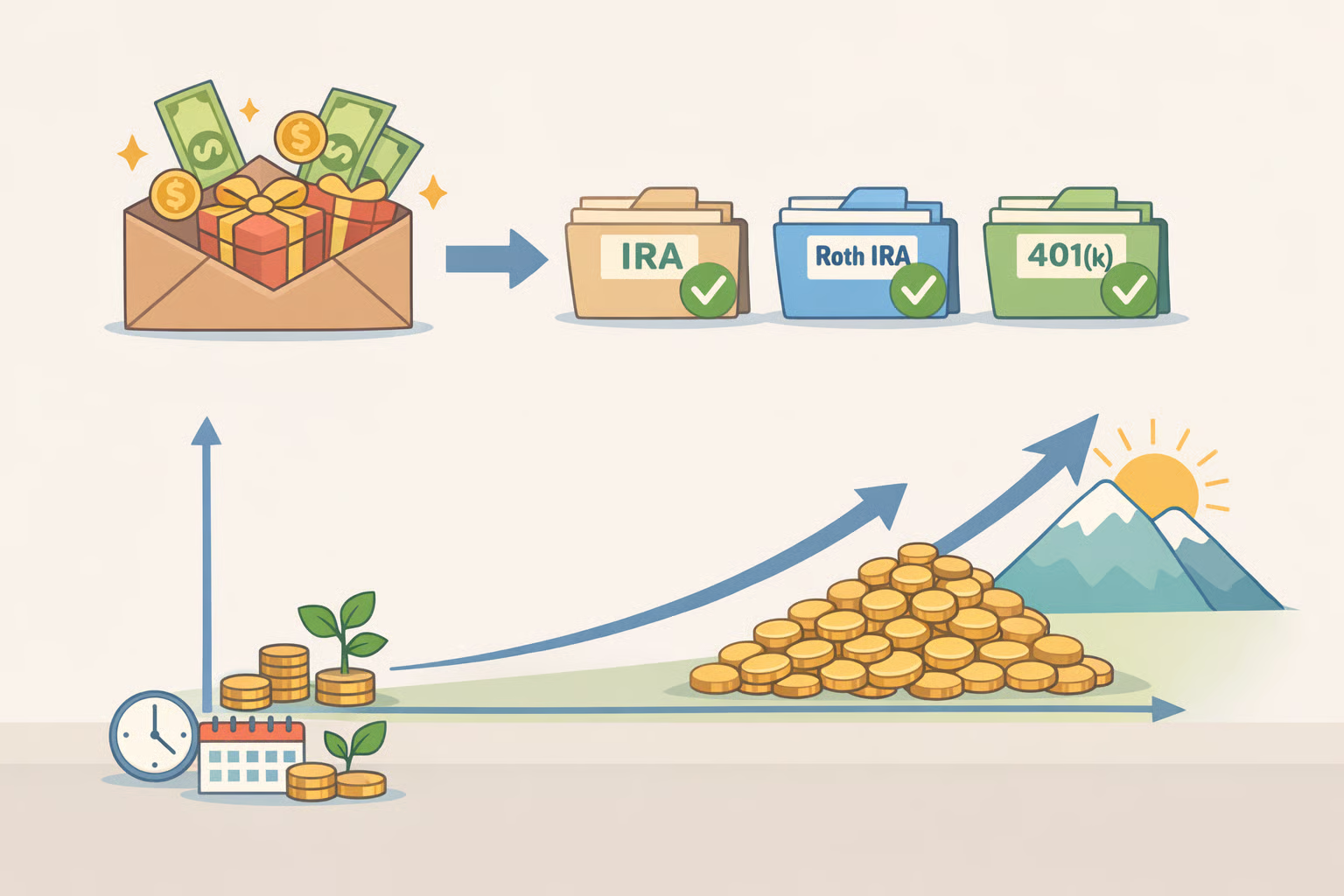

Step 4: Put the rest into long-term accounts

Once you have a buffer, look at tax-advantaged accounts first.

If you have not hit the annual contribution limits on a 401(k), HSA, or traditional IRA, bonus money can do double duty. It can reduce taxable income now and still keep working for you over the long haul. NerdWallet That is the part of personal finance that does not need a slogan.

If your employer allows bonus deferrals into retirement contributions, that can be worth checking too. If not, increasing future paycheck contributions can free up the same amount of cash and send it into the account over time. The mechanics vary, but the idea is the same: move money into a place where it has a job.

The compounding example is the clearest argument for patience. CNBC said a $3,000 bonus invested in an index fund averaging 7% annual returns would grow to $24,349 over 30 years. CNBC That is not a promise, just a reminder that time does most of the heavy lifting when you let it.

If retirement accounts are already maxed out, the remaining options are still respectable: a taxable brokerage account in a low-cost index fund, career development through courses or certifications, or a college savings account if that fits your life better. CNBC specifically pointed to courses, workshops, and certifications as a smart use of bonus money, and that is hard to argue with if a skill upgrade changes your earning power. CNBC

How to use a work bonus wisely without turning it into a sermon

People do strange things with windfalls. That is not a moral judgment, just a fact of human wiring.

The classic NBER paper on reduced tax withholding found that 43% of consumers said they spent the extra take-home pay they received when withholding changed in 1992. NBER Working Paper 4344 The study was about withholding changes, not bonuses specifically, but the lesson still travels: money that feels unexpected tends to get treated differently from regular pay.

That is why a modest, pre-decided splurge makes sense. Once debt is under control, emergency savings are funded, and retirement contributions are on track, NerdWallet says allocating around 10% of a windfall to personal enjoyment is a reasonable rule of thumb. NerdWallet CNBC made the same broad point in plainer language, noting that travel, shopping, or entertainment are fair game when the higher priorities have already been handled. CNBC

The trick is to make the spending deliberate. Pick the amount in advance, ring-fence it, and use it for something you will actually enjoy instead of letting the bonus leak away on the usual assortment of forgettable purchases.

A simple order of operations

If the bonus is still sitting in your head as “extra money,” turn it into a sequence:

- Calculate the net amount after federal withholding, payroll taxes, and state tax.

- Pay off high-interest debt.

- Fill or strengthen your emergency fund.

- Put the rest into retirement or other long-term accounts.

- Set aside a small, fixed amount for yourself.

That order is boring in exactly the right way. It gives the bonus a purpose before the money starts behaving like confetti.

Conclusion: Give the bonus a job before it gives you ideas

The smartest answer to what to do with a work bonus is not to treat it like a lottery ticket. It is ordinary income with extra steps, and IRS rules mean the take-home amount will be smaller than the headline number anyway. Once that is clear, the rest gets easier: attack costly debt, build cash reserves, invest for the long term, and allow a small reward once the serious stuff is handled.

The best bonus is the one that quietly improves next month, next year, and the decade after that. Fine to buy a little joy with it too. Just do that last.