- Saving Habits to Build Wealth: 7 Practical Steps

- Know your numbers first

- Set one specific savings goal

- Build an emergency fund before you chase anything fancier

- Simple saving habits that automate your savings

- Increase retirement contributions gradually

- Track your progress without obsessing over it

- Use account separation to keep money in its lane

- Make the habits work together

- What to do after the habits are in place

Saving Habits to Build Wealth: 7 Practical Steps

By the end of this guide, you’ll have seven saving habits you can put to work right away, plus a simple system that takes some of the guesswork out of money management. That matters because the numbers are still stubborn: in 2024, 55 percent of adults said they had enough saved to cover three months of expenses, down from 59 percent in 2021, and only 35 percent of non-retirees felt their retirement savings were on track, according to the Federal Reserve. The problem is not a lack of tools. It is that habits collapse when they depend on memory and good intentions.

That is where simple saving habits to build wealth do their best work. Fidelity and the Consumer Financial Protection Bureau both point toward the same basic fix, automate what you can, set clear goals, and make the money harder to accidentally spend.

Know your numbers first

Before any saving habit sticks, you need a baseline. Start with what comes in, what goes out, and where the gaps are. Fidelity says knowing your income and expenses is the first step in saving money.

Pull up three months of bank and credit card statements and sort spending into a few buckets. Fidelity’s framework is a useful check: 60 percent or less of take-home pay for essentials, 30 percent for nice-to-have spending, 10 percent for near-term goals and emergency savings, and 15 percent of pre-tax income for retirement, including employer contributions, Fidelity says. If the math feels ugly, good. That means the numbers are doing their job.

The point is not to produce a perfect budget. It is to find the amount you can realistically redirect without pretending your life is made of spreadsheets and self-denial. If your discretionary spending is too high, that gap becomes the first place to find savings.

Set one specific savings goal

Vague goals tend to evaporate. “Save more money” sounds noble and gets you nowhere. A concrete target with a deadline gives your savings something to hit.

Fidelity’s example is plain enough: a $5,000 goal for a year works out to about $417 a month, or $14 a day, Fidelity said in March. That kind of breakdown is useful because it replaces a huge number with a smaller one that feels less theatrical. At a 4.5 percent annual yield compounded monthly, Fidelity says saving $417 a month from zero could leave you with $5,127.67 after one year, Fidelity showed.

Pick one goal first. Write down the amount, the deadline, and the monthly transfer required to get there. The CFPB says sustainable saving works best when a goal is paired with a system for consistent contributions and regular progress checks.

Do not make the target heroic. A goal that requires perfect behavior is just a guilt machine with a calendar attached. Leave some room for months that run hot.

Build an emergency fund before you chase anything fancier

Emergency savings are not the boring cousin of investing. They are the thing that keeps a temporary setback from turning into a long, expensive mess.

The CFPB defines an emergency fund as cash set aside for unplanned expenses or financial emergencies, such as car repairs, home repairs, medical bills, or a loss of income. It also notes that people who struggle to recover from a financial shock often have too little savings and may lean on credit cards or loans, or even pull from retirement funds, which can make the original bill much larger because of interest and fees.

The Federal Reserve’s 2024 survey shows why that buffer still matters. Thirteen percent of adults said they would be unable to cover a hypothetical $400 expense by any means, up from 11 percent in 2021, and 55 percent said they had savings to cover three months of expenses, down from 59 percent in 2021, the Federal Reserve reported.

Open a separate savings account for this fund. Keep it distinct from checking so the money is not just floating around looking useful. The CFPB says a bank or credit union account is generally one of the safest places to keep it, while cash can be stolen, lost, or destroyed.

Simple saving habits that automate your savings

This is where the process gets easier. The goal is to reduce the number of decisions between your paycheck and your savings account. Fidelity says automation can help you save money, invest more consistently, and stay on top of bills without adding to your daily to-do list.

Automate transfers to savings

Set up recurring transfers from checking to savings. The CFPB says this is one of the easiest ways to save automatically, and Fidelity recommends the same approach. If your employer offers direct deposit, ask whether your paycheck can be split between two accounts, one for spending and one for saving, the CFPB says.

Start with an amount you can actually sustain. Twenty-five dollars per transfer is not glamorous, but neither is an empty savings account. The habit matters more than the headline figure.

Put bills on autopay

Recurring bills are a bad place to rely on memory. When bills are set to autopay, you are less likely to miss payments or rack up late fees, Fidelity says.

That does not mean autopay is magic. It means the bill gets paid on time without you having to remember it every month, which is how grown-up systems usually work. Set it, then check it once in a while so the balance does not surprise you.

Set investments to recur

Recurring investments remove the awkward ritual of deciding when to invest. The money moves on schedule, and you do not have to time the market perfectly or stare at the news waiting for a sign from the heavens, Fidelity says.

Brookings said in January 2024 that the SECURE 2.0 legislation, passed in December 2022, is the most extensive set of changes to retirement law in 15 years, and that it expanded automatic enrollment and made saving easier for more workers, Brookings reported. That is the broader policy version of the same idea: make saving the default, not the heroic exception.

Increase retirement contributions gradually

A lot of people set a retirement contribution rate and leave it there for years. It is a comfortable habit, which is another way of saying it can become a lazy one.

Fidelity recommends contributing 15 percent of annual pay to a retirement plan, including any employer match, but also says if 15 percent is not doable, that is okay, Fidelity says. One practical way to get there is to raise contributions automatically by 1 percent each year. Fidelity says that kind of increase could potentially leave you with $1.2 million more than if you had left contributions unchanged.

This works because it avoids the big, painful adjustment. You do not need to remodel your life. You just need to make the deduction a little larger over time, while life is busy pretending not to notice.

Track your progress without obsessing over it

Saving works better when you can see it. The CFPB recommends regular progress checks, whether that is an automatic account notification or a running tally you update yourself. The point is not surveillance. It is encouragement.

Pick one way to monitor the balances that matter. For an emergency fund, a monthly check is usually enough. For retirement contributions, an annual review may do the trick, especially if you use automatic escalation.

There is a small psychological benefit here that finance advice often misses. Progress is easier to repeat than intention. Once the number starts moving in the right direction, the habit becomes less abstract.

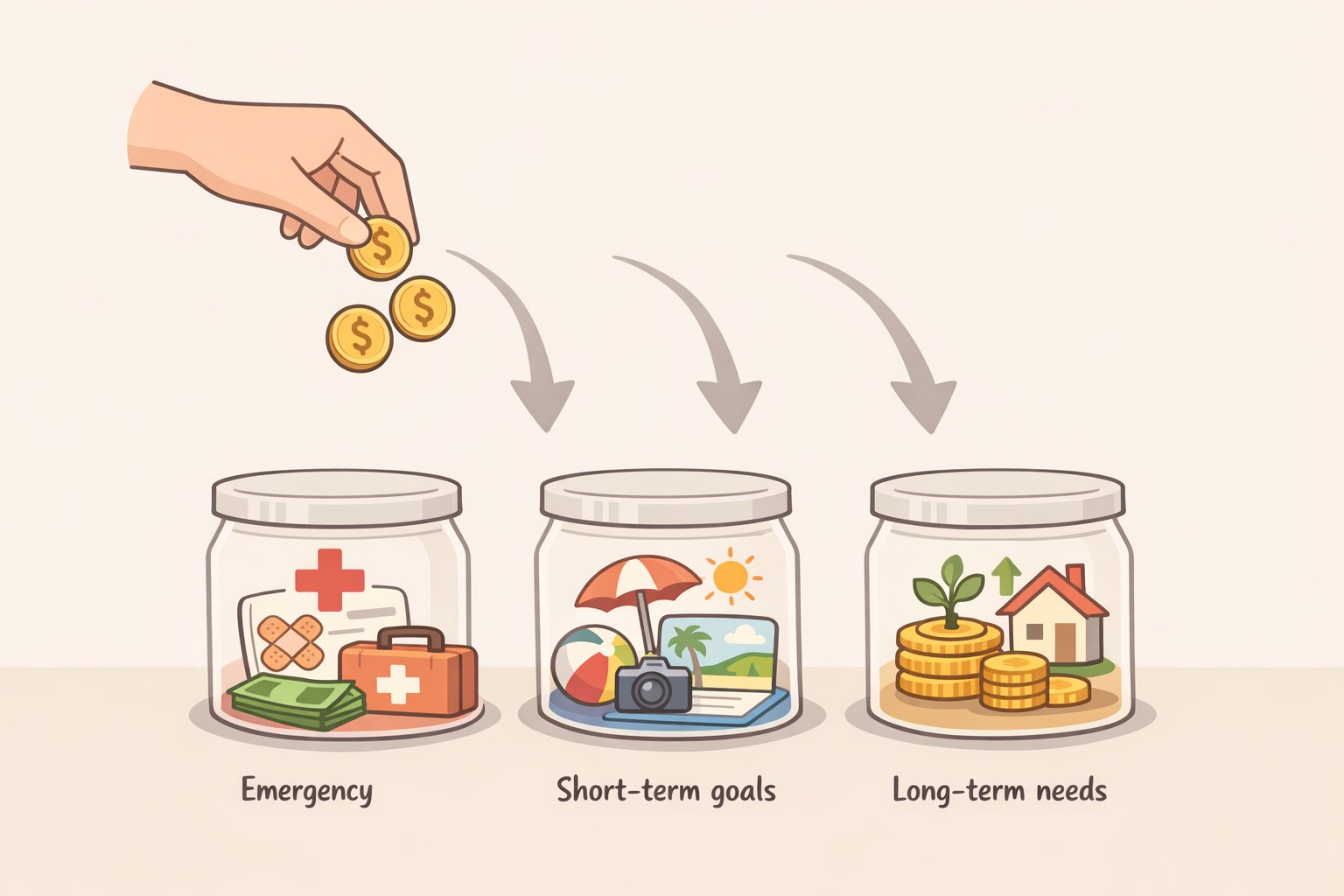

Use account separation to keep money in its lane

Not all savings should sit in the same place. The CFPB says a dedicated savings or emergency fund is one essential way to protect yourself, and Fidelity says short-term goals may be better kept in checking, regular savings, high-yield savings accounts, or cash-like investments such as CDs or money market funds, depending on your situation, Fidelity says.

That separation keeps you from raiding the wrong bucket for the wrong reason. Emergency money should be easy to reach, but not so easy that a mood swing can drain it. Short-term goal money should not be taking a vacation in your checking account just because it was lonely.

This is one of those rare moments when account structure matters almost as much as the amount saved. Money with a job should not be wandering around unassigned.

Make the habits work together

These habits are stronger as a system than as isolated tricks. Knowing your numbers gives you a starting point. Specific goals give the money a destination. Automation makes the whole thing easier to maintain.

That combination is the real lesson in the research. Fidelity says automation helps you save, invest, and keep up with bills without more daily effort, while the CFPB says consistent contributions are one of the fastest ways to build savings. The Federal Reserve’s 2024 data shows why this still matters: 61 percent of adults had a tax-preferred retirement account, but only 35 percent of non-retirees thought their retirement saving was on track, the Federal Reserve reported.

That gap is where habits matter most. Having an account is not the same thing as funding it properly. A system that moves money before you can argue with yourself tends to beat raw willpower, which has an inconsistent track record and a strong taste for excuses.

What to do after the habits are in place

Once the habits are running, the next question is where to park the money. Fidelity says short-term goals may fit in checking, savings, or high-yield savings accounts, while retirement money belongs in tax-advantaged accounts like a 401(k), IRA, or Roth IRA, depending on your situation, Fidelity says. That choice is a separate decision from the habit itself.

Start with the system, not the perfect destination. If the money is arriving regularly, the rest gets easier. That is the point of saving habits to build wealth, they make the right move the default one, and they keep working long after the initial burst of motivation has packed up and gone home.