- Social Security full retirement age 67 explained: rules

- What is Social Security full retirement age?

- Why a higher full retirement age is, in practice, a benefit cut

- Who is hurt most by Social Security full retirement age 67

- The solvency problem and who gets asked to solve it

- What to take away and where this is headed

Social Security full retirement age 67 explained: rules

For anyone born in 1960 or later, the Social Security full retirement age 67 is not a proposal waiting in the wings. It is current law, and the phase-in finished in 2022, according to SSA.tools and the SSA FAQ. No further increase is scheduled unless Congress changes the rules.

That matters because Social Security is not a side dish in retirement. The SSA says it covers about 96% of U.S. workers and replaces about 40% of annual pre-retirement earnings on average, with more than half of seniors relying on it for all or most of their income (SSA fact sheet, April 2025). The retirement age is one of the main levers that determines how much of that income people actually receive.

This article explains what the full retirement age means, why a higher retirement age functions as a benefit cut, and who bears the heaviest losses if Congress pushes it higher.

What is Social Security full retirement age?

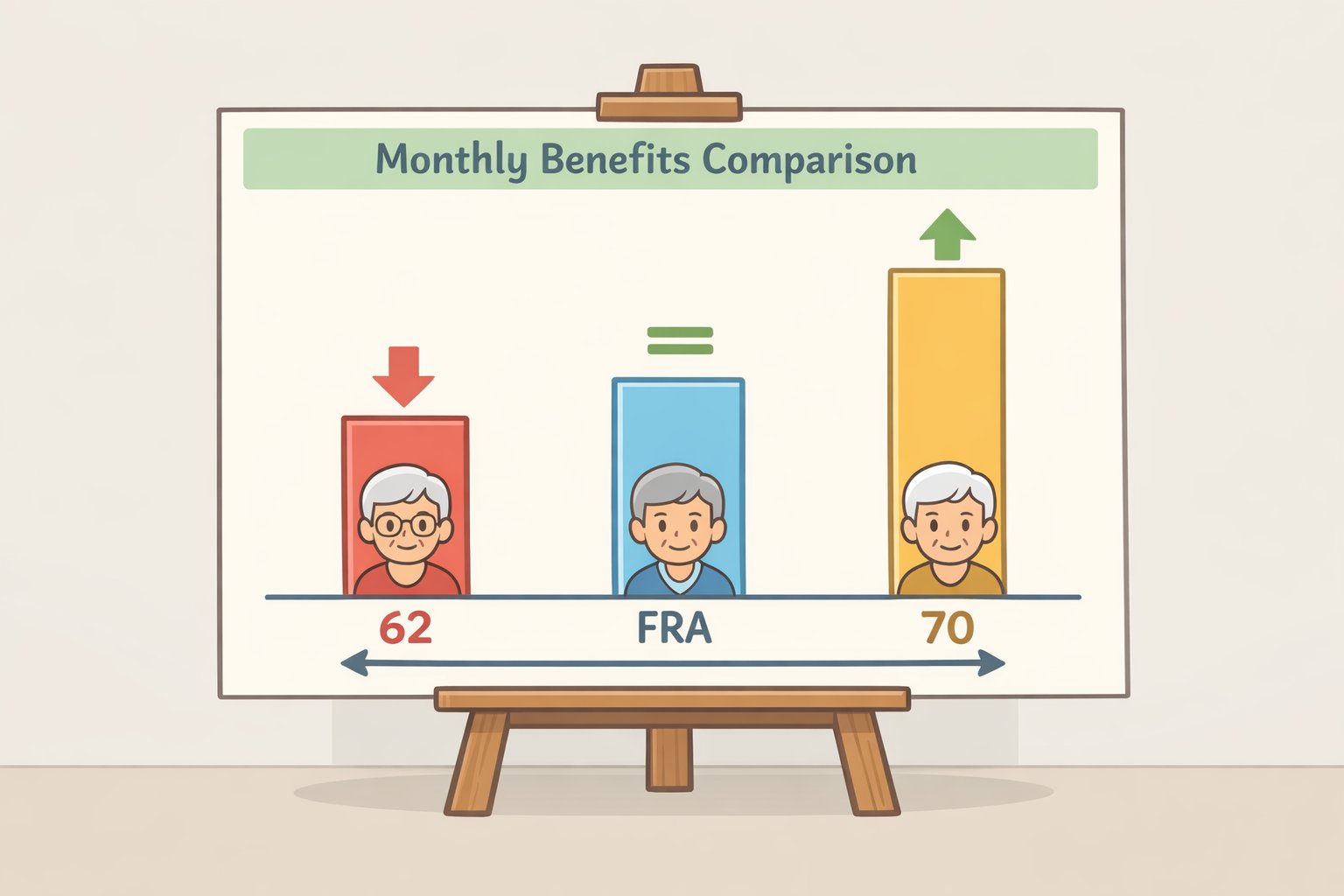

The normal retirement age, or full retirement age, is the point at which a worker gets 100% of their calculated Social Security retirement benefit, with no reduction for claiming early and no increase for waiting, SSA.tools says. It is the neutral reference point in the system.

That neutrality is easy to misunderstand. Workers can start benefits as early as 62, but the monthly payment is permanently reduced. They can also wait until 70, and delayed retirement credits raise the monthly benefit. As SSA.tools notes, the word “full” can be misleading, because waiting past full retirement age can produce a benefit 24% to 32% higher than the full amount, depending on birth year.

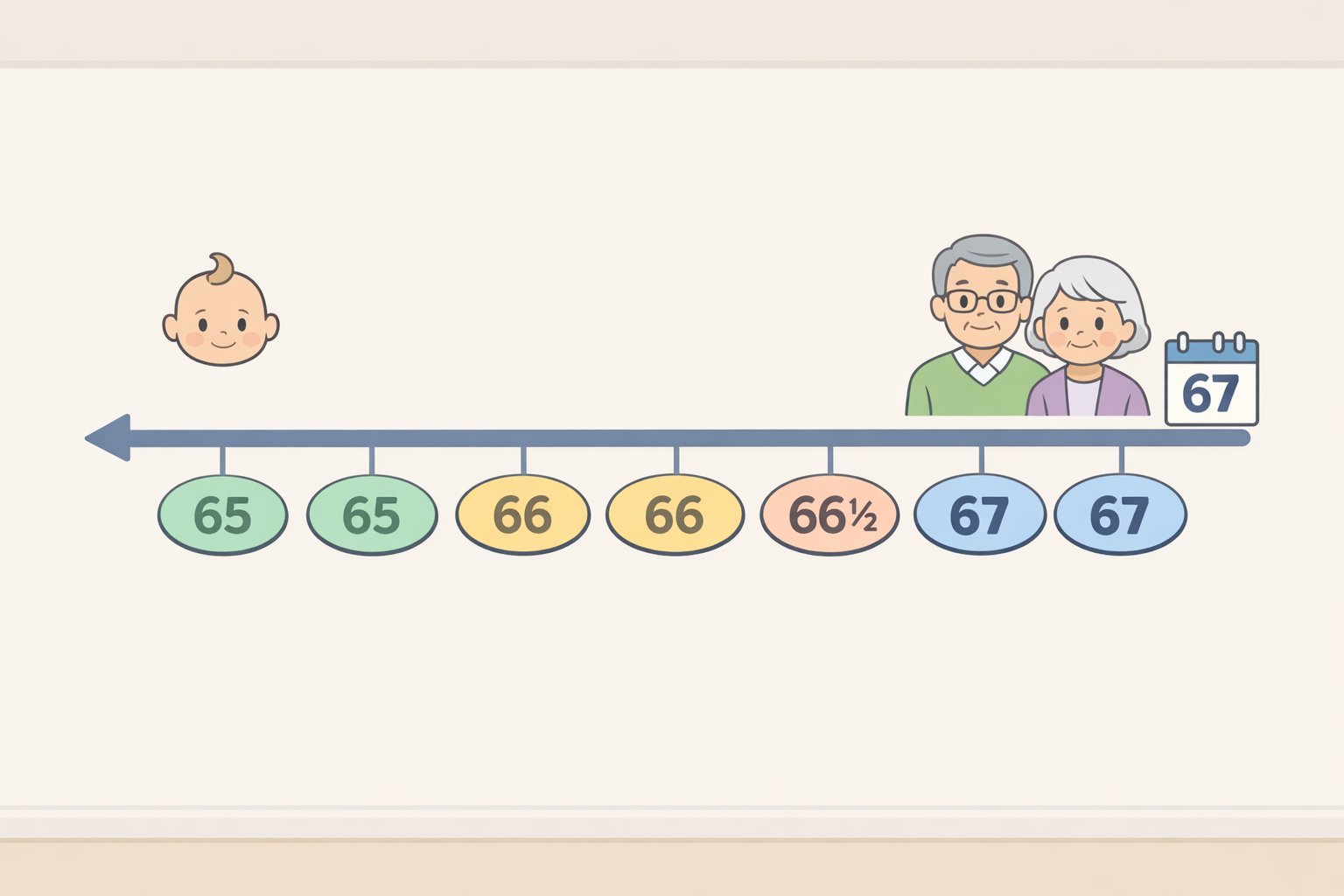

The age has not always been 67. Brookings says the full retirement age was 65 when Social Security was established in 1935, and Congress set a gradual increase in the 1983 amendments to deal with financing problems (Brookings, September 2024). The first step raised it to 66 for workers born in 1943, and the second step eventually brought it to 67 for people born in 1960 or later.

That finish line matters now because it closed a long-running phase-in and exposed the next fight. The law is no longer inching upward by itself. Any move beyond 67 would be a fresh political choice, not the last installment of an old one. That is where the debate gets sharper, and far less polite.

A quick birth-year guide makes the pattern clearer, based on SSA materials:

- Born 1943 to 1954: full retirement age is 66

- Born 1955: 66 and 2 months

- Born 1956: 66 and 4 months

- Born 1957: 66 and 6 months

- Born 1958: 66 and 8 months

- Born 1959: 66 and 10 months

- Born 1960 or later: 67

One useful distinction: Medicare eligibility still begins at 65, even though Social Security’s full retirement age is 67 for younger workers, the SSA says.

Why a higher full retirement age is, in practice, a benefit cut

The key point is simple: raising the full retirement age lowers benefits at every claiming age below it.

Claiming at 62 already means a permanent reduction. Under current law, a worker with a full retirement age of 67 gets 70% of the full benefit if they claim at 62, according to CBPP and SSA.tools. If the full benefit were $2,000 a month, that person would receive $1,400 a month for life.

The reduction is permanent. Cost-of-living adjustments still apply, but they apply to the reduced base amount, not to the benefit the worker would have received at full retirement age, SSA.tools says.

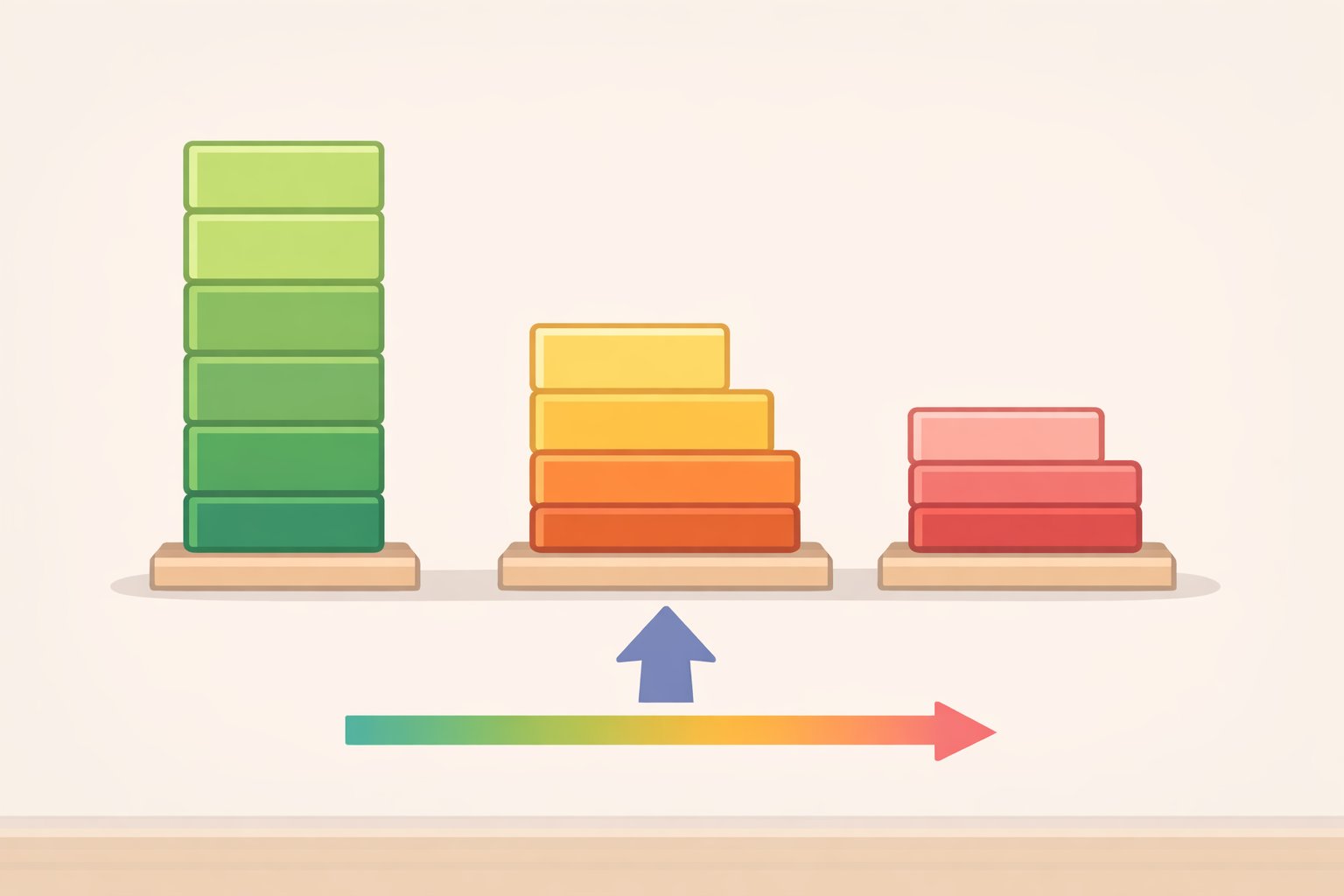

That is why an increase in the retirement age works like a broad benefit cut. CBPP says each additional year added to the full retirement age is roughly equivalent to a 7% cut in monthly benefits for affected retirees. The 1983 shift from 65 to 67 already lowered benefits by about 13% across the board, and pushing the age to 70 would cut scheduled benefits by nearly 20%.

The numbers get starker when laid out plainly. Under current law, a worker claiming at 62 gets 70% of a full benefit if the full retirement age is 67. If that age were 70, the same worker would get 57% of a full benefit, or $1,140 instead of $2,000 in the CBPP example. That is not a technical adjustment. It is a smaller check, every month, for the rest of the person’s life.

And the people affected are not a small minority. In 2023, nearly 840,000 people claimed Social Security at 62, the first month they could, making it the most popular claiming age, according to CAP (February 2025). More than 1.7 million new retirees claimed between 62 and 65, while only about 1.4 million claimed at or after full retirement age. The retirement age debate is not about a fringe group of planners with spreadsheets and patience. It is about the majority behavior of actual retirees.

Who is hurt most by Social Security full retirement age 67

The full retirement age applies to everyone, but its costs do not land evenly. Workers with fewer choices take the biggest hit.

Lower-income workers claim early out of necessity, not ignorance

Low-income older workers are more than three times as likely as high-income workers to claim Social Security before full retirement age, Reuters reported in August 2023, citing research by economist Teresa Ghilarducci. That undercuts the familiar idea that early claimers are simply uninformed.

Many are claiming early because they need the money to supplement wages that are too low to cover living expenses, Ghilarducci told Reuters. In other words, “work longer” is easy advice to give when a person can keep working. It is much less persuasive when the option is shaky or nonexistent.

That is not a rare edge case. CBPP found that among people who claimed at 62, 28% of women and 20% of men had already stopped working before that birthday. It also found that four in 10 recent retirees had been pushed out of their jobs, and about 40% of people in their early 60s reported a potentially disabling condition, while fewer than half of that group ever qualify for disability benefits.

Savings tell the same story. CAP reported in July 2024 that only 8% of Americans in the bottom fifth of the income distribution between ages 32 and 61 have any retirement savings at all, compared with 88% in the top fifth. For those households, Social Security is not one income stream among several. It is the income stream.

The life expectancy gap amplifies every dollar lost

Social Security’s design assumes that early claimers collect smaller monthly benefits for longer, while later claimers collect larger checks for shorter periods, so lifetime benefits are roughly balanced across claiming ages. That logic works in theory. In practice, it breaks down across income levels.

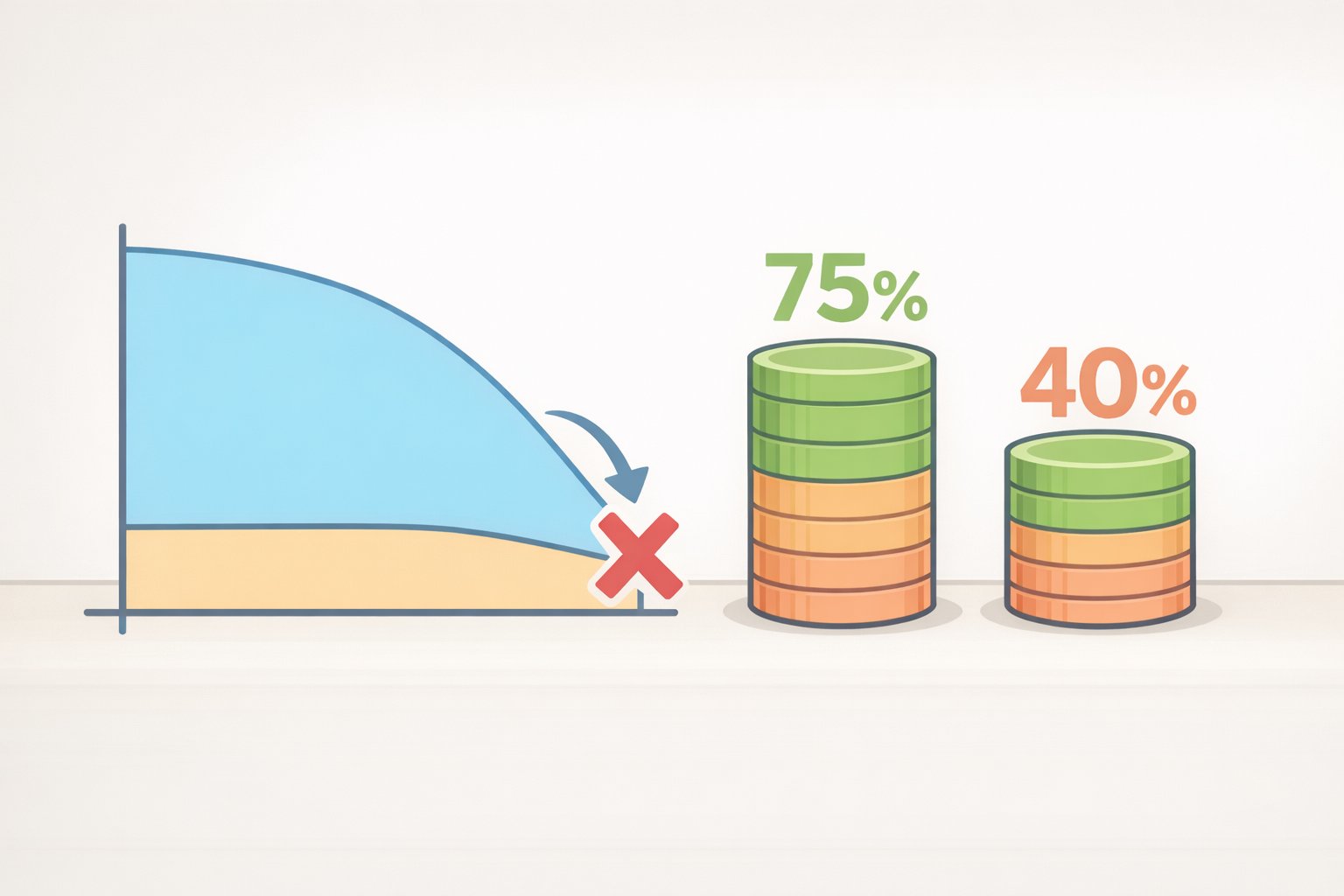

CAP noted in July 2024, citing GAO research, that a male worker at the 10th percentile of lifetime earnings can expect fewer than 10 years of benefits after reaching full retirement age, while a male worker at the 90th percentile can expect more than 18 years. A policy that trims three years of benefit time is therefore a much bigger share of expected retirement for the lower-earning worker.

Vox modeled in September 2025 what a three-year increase in the retirement age, from 67 to 70, would mean across income groups. Men in the highest income bracket would lose about 11% of expected benefit-collection years. Men in the lowest bracket would lose nearly 20%. Same rule, different consequences.

Physically demanding jobs make the problem worse. Lower-income workers are more likely to work in construction, manufacturing, agriculture, and other jobs that wear people down earlier, CAP said, and the American Academy of Actuaries has made the same basic point. Telling a person with a battered back to “just wait until 70” is a tidy slogan, but it is not much of a policy.

Racial inequities compound the picture, carefully

Black and Hispanic beneficiaries already receive lower lifetime Social Security benefits than white beneficiaries, according to the Urban Institute (December 2023). The Urban Institute projects that adults born between 2001 and 2010 will receive lifetime benefits 19% lower for Black beneficiaries and 14% lower for Hispanic beneficiaries than for white beneficiaries.

Life expectancy at 65 also varies by group, though not in one neat direction. CBPP reported in April 2023 that white life expectancy at 65 was 19.5 years in 2019, while Black and American Indian or Alaska Native life expectancy at 65 was 18.2 years. Asian and Hispanic life expectancies were higher, at 23.4 and 21.6 years.

The broader point is that a higher retirement age compounds existing disadvantages for groups with shorter expected benefit windows, but not identically for every community. That is why careful policy analysis matters. Broad averages can hide more than they reveal.

University of Michigan research adds another layer. It found that Social Security reduces retirement wealth disparities relative to other income sources, but absent policy changes, racial and ethnic gaps in retirement security are expected to widen over time. Raising the retirement age would not close that gap.

The solvency problem and who gets asked to solve it

The retirement age debate exists because Social Security has a financing problem. It is not a theoretical one.

Vox reported in September 2025 that the trust fund is projected to be depleted in about eight years, which points to 2033. At that point, current payroll tax revenue would cover about 77% of promised benefits, meaning an immediate across-the-board cut of roughly 23% under current law. The numbers are blunt, and they are not optional.

Raising the full retirement age would reduce the size of that shortfall, but it would not erase it. Brookings estimated in September 2024 that raising the age from 67 to 68 would close about 12% of the 75-year actuarial imbalance. A two-year increase, followed by longevity indexing that adds about one month every two years, could address close to 40% of the long-run gap.

That still leaves most of the problem unresolved, and it shifts the burden onto workers least able to absorb it. That is why some analysts and policymakers have proposed different combinations of tax and benefit changes.

One Brookings blueprint would raise the retirement age only for the top 20% of earners, eventually taking that group to 70 while leaving it unchanged for workers below the 60th percentile, with smaller increases in between (Brookings blueprint, February 2025). Another approach would raise more revenue by lifting the payroll tax cap so that it once again covers 90% of total wage earnings, roughly the ratio in 1983. CBPP says that would mean a cap of about $300,000, up from roughly $160,200 today.

Those are different choices about who pays. One asks more of higher earners through taxes. The other trims benefits more sharply for people most able to wait.

What to take away and where this is headed

The Social Security full retirement age 67 is already the rule for anyone born in 1960 or later. The real question is whether Congress moves it higher, and if so, whether it does so in a way that makes an already uneven system even more tilted against workers with the least flexibility.

The distributional pattern is not hard to see. A worker with a desk job, good health, savings, and some control over timing can often wait. A worker with poor health, no cushion, and a physically punishing job often cannot. The first worker has options. The second has deadlines.

The financing clock is also running. With trust fund depletion projected around 2033, reform decisions in the next few years will shape outcomes for tens of millions of Americans, and Vox notes that any bipartisan deal will require major concessions. The retirement age will probably be part of that bargain. The distributional evidence should be part of it too.

For readers deciding when to claim, the SSA’s Retirement Ready fact sheet shows how large the differences can be. A $1,000 monthly benefit at full retirement age can fall to $750 at 62 or rise to $1,320 at 70. Health, savings, income needs, and spousal factors all matter. There is no universal answer, only the mechanics, which are plain enough once the fog clears.